Competency 4.02 Understand the Banking System

580 likes | 743 Vues

4.0 Understand the Role of Finance in Business. Competency 4.02 Understand the Banking System. Objective 4.02-A Analyze the roles/responsibilities of the Federal Reserve. The Federal Reserve System. What is the Federal Reserve System? Why does it exist? Who participates?

Competency 4.02 Understand the Banking System

E N D

Presentation Transcript

4.0 Understand the Role of Finance in Business Competency 4.02Understand the Banking System Objective 4.02-A Analyze the roles/responsibilities of the Federal Reserve.

The Federal Reserve System • What is the Federal Reserve System? • Why does it exist? • Who participates? • How is it organized?

The Federal Reserve (The Fed)A Centralized Banking System • Federal Reserve Act signed into law by President Woodrow Wilson • Organized by the Federal Government in 1913 • Why have “ The Fed” ? Purpose: • To establish and maintain confidence in the US monetary system • To ensure a safe, healthy and stable economy • To supervise and regulate member banks and help serve the public efficiently. * Prior to the Federal Reserve Act anyone could issue currency or coin money

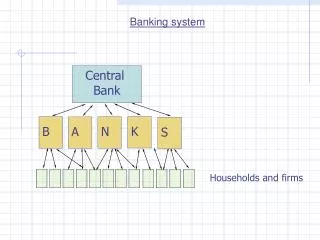

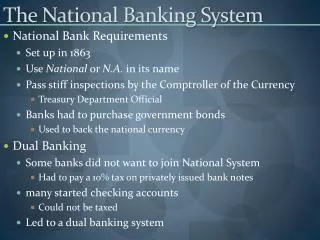

Who Participates in Federal Reserve? • All National Banks are required to be part of the Fed • Optional for state banks • Divisions are called DISTRICTS • There are 12 DISTRICTS in the United States • Every state comes under a district • Each Federal Reserve Bank is a corporation, owned by its member banks NC is in District 5, the Richmond District.

The Federal Reserve • What are the two arms of “The Fed”? • Board of Governors • Represents the government (public) sector • District Federal Reserve Banks • Represents the business (private) sector

Board of Governors • Usually meet about twice a week, ordinarily on Mondays and Wednesdays • Public is invited to look into the meetings of the Board of Governors • Usually discuss monetary policy such as lowering and raising interest rates The Board Room at the Federal Reserve in Washington, DC

Members of the Board of Governors • Ben S. Bernanke, Current Chairman • Alan Greenspan, Retired Chairman • Chairman is appointed by President and confirmed by Senate • Similar to procedure for Supreme Court Justices

Purpose of Federal Reserve • Established to supervise and regulate banks • Known as the “Bank’s bank” • The central bank of the United States • Assists banks with serving the public more efficiently • All national banksare required to join the Federal Reserve System • State banks have the option of joining the system

The Federal Reserve System Services • Supervision of banks • Agent for the federal government • Regulates monetary policy • Lends money to member banks • Acting as a clearinghouse • Participation in open market activities • Sets loan limits & standards • Supplies currency

1. Fed Supervision: Set Reserve Requirements • Member banks are required to keep a certain percentage (10% for many years) of all deposits in the bank’s vault or on deposit with the district federal reserve bank • Reserves: funds set aside for emergencies • Example: a rush of withdrawals by customers • Purpose: to reduce risk of bank panics and protect depositor’s money

1. Fed Supervision: Audits Member Banks Inspects banks by auditing financial records • Audit -an inspection of records to verify the: 1. accuracy of books (records) of the bank 2. bank is complying with banking laws Similar to Individuals/corporations who are audited by the IRS to review the accuracy of a tax return.

1. FED Supervision: Approves Bank Mergers Q: Why do banks merge? To be more competitive -to offer customers more locations (local, regional, national, international) -to offer a variety of services more efficiently -to compete with a growing array of other financial service companies such as: *money market and other mutual funds *mortgage companies *credit unions and *credit arms of industrial firms (General Electric and Ford Motor) Here are some recent bank mergers approved by “The Fed” in 2007-2008 • Bank of New York bought Mellon Financial Corporation for $18.3 Billion • JPMorgan Chase bought Bear Stearns for $1.1 Billion • Bank of America bought Merrill LynchBank of America for $50 Billion • Wells Fargo bought Wachovia for $15.1 Billion

2. Fed Acts as Agent for Federal Government • The Fed holds a checking account for the US Treasury • Disburses social security benefits and other transfer payments using the direct deposit system • Accepts some types of federal tax money Example: Federal tax depositories Payroll taxes - federal income tax, FUTA, and social security taxes are deposited using federal deposit coupon into a national bank

3. FED Regulates Monetary Policy • What is Monetary Policy?When the Federal Reserve influences money and credit conditions in the economy to achieve economic goals • How? The Fed determines amount of money in circulation and available for loans, then either increases or decreases to stabilize/stimulate the economy • Tight money- policy when less money is available at higher interest rates, slows (stabilizes) economy • Loose money- policy when more money is available at lower interest rates, increases (stimulates) economy

4. FED Lends Money to Member Banks Monitors the discount rate of interest - rate used by the Fed to loan money to member banks • Compare banks to intermediaries (go-betweens) trading in money at “wholesale” prices The Fed changing interest rates affect borrowers (member banks) who pass rates to consumers • Raising rate - discourages borrowing • Reducing rate - encourages borrowing • Note: the Federal Reserve does not loan money to individuals or businesses (only member banks) HOWEVER, rates the Fed charges member banks “trickle down” and affect the interest rates for consumers

5. FED Acts as Clearing House Clears/Processes/Settles checks for member banks • Federal Reserve uses the Automated Clearing House (ACH) to electronically complete fund transfers (check settlements) between banks • Interdistrict Settlement Fund in Washington, DC used for between district transfers • Checks/deposit slips have MICR coding • Magnetic Ink Character Recognition • Scanners read MICR on checks to electronically process data accurately and rapidly through the ACH and Interdistrict Settlement Fund

6. FED Participates in Open Market Participates in open market operations by buying and selling government securities Q: What are government securities? A: Treasury bills and bonds – loans to government in various denominations (amounts) and for various time periods • Advantages and Disadvantages + offer a fixed rate of interest over a fixed period of time + attractive because not subject to income taxes - cannot be easily transferred and are non-negotiable

Open Market Operations Government securities are sold at a discount (from face value), but are redeemed (cashed in) for face value on the maturity (due) date Examples: • Purchase treasury note for $7500 (discount price), redeem at maturity date for $10,000 (face value) • Purchase Series EE savings bond for $25, redeem in 7 years at maturity for $50

Government Securities • Savings bonds - Example Series EE- • Denomination minimum $25 • Payable after 6 months • Earns interest up to 30 years • Short-term obligation of the U.S. TreasuryTreasury bill – maturity in one year or less • Issued to mature in 13 weeks, 26 weeks, 52 weeks • Long-term obligation of the U.S. Treasury • Treasury note – maturity at 1 to 10 years, minimum $1000 • Treasury bond - maturity at 10 + years

Open Market Operations Bank discount rates encourages borrowing by member banks, and therefore encourages borrowing by consumers • Purpose of open market operations • Regulate money supply Most frequent method of controlling the economy • Who controls open market operations? • Federal Open Market Committee (FOMC)- A committee within the Federal Reserve

7. The FED Sets Lending Standards Sets standards for consumer legislation dealing with lending and credit • Sets limits for loans and investments by member banks News: Federal Reserve revised bank lending rules since banking crisis • Ex: Lower % of total loans for land/acreage

8. The Fed Supplies Currency • Money defined: • a medium of exchange for value • US money = currency and coins Federal Reserve supplies paper currency • Legal Tender for all debts, public and private • Paper currency supplied is “Federal Reserve Notes” Printing currency (paper money, bills) • Bureau of Printing and Engraving • Counterfeiting - federal crime Coinage • Minting supplied and regulated by the Department of Treasury, US Mint

St. Louis Federal Reserve • http://www.stlouisfed.org/education_resources/

Topics Classification of financial institutions Depository Non-depository Common payment services Electronic Funds Transfers Online Bill Pay Checking Accounts Specialty checks Money Orders

Classification of Financial Institutions Depository Earns money to finance their business by accepting deposits from customers Types include: Commercial banks- full service - offer many different services, including savings, loans, and checking accounts. Savings and Loan associations (S&Ls) -traditionally specialize in savings and home loans, but now are very similar to commercial banks. Mutual savings banks- owned by the depositors and specialize in savings and home loans. Credit unions- not-for profit, serve their members only, and are owned by their depositors.

Classification of Financial Institutions Non-depository Earns money to finance their business by selling specific services such as policies, investments, and loans Types include: Life insurance companies -term, whole, universal Investment companies - stocks, bonds, mutual funds Consumer finance companies – higher rates if bad credit Mortgage companies – loan $ for land, buildings, homes Check-cashing outlets –fee based if do not have bank acct Pawnshops –loan $ based on value of item pawned

How To Compare Financial Institutions Which characteristics of financial institutions are of interest? Services offered Safety Convenience Fees and charges Restrictions What kinds of questions may be asked about each characteristic?

Comparative Questions • Services – Does the institution offer needed services? • Savings • Depository for payroll taxes • Checking • Various options to meet customer needs • Loans • Short term - working capital • Long term - mortgage • Credit cards • Debit cards • Safe deposit boxes • Trust management

Comparative Questions • Safety– Is the institution insured against losses? • Federal Deposit Insurance Corporation (FDIC) Created by Congress to maintain stability and public confidence in the nation’s financial system: insures deposits, supervises financial institutions • National Credit Union Administration (NCUA) Charters and supervises credit unions

Comparative Questions • Convenience – Does the institution offer the access desired? • Physical locations available • Online services • Easy to access & use • ATM machines

Comparative Questions • Restrictions – Are there minimum balances that must be kept, or other restrictions? • Minimum balance- $ amount required to stay in account at all times • If account keeps minimum balance, fees are often waived (eliminated)

Comparative Questions • Fees and Charges– What are the short and long-term costs of the services? • Flat monthly fees • Fees per transaction • NSF (Non-sufficient funds) fees • Checks written • Debit transactions • # of transactions allowed before fees begin • Minimum balance required to eliminate fees

Common Payment Services • Electronic Funds Transfers • Online Bill Pay • Checking Accounts • Personal, business • Specialty checks • Certified, Cashier’s, Traveler’s • Money Orders • Postal, Express, Telegraphic

Online Bill Pay • Use the web to make payments • Often fee based • Privacy can be issue • Change PIN frequently • Use only “safe” sites • Write Online Bill Pay questions 1-3 from next slide on notebook paper. Use the website to answer the questions. • http://banking.about.com/od/bankonline/f/setupbillpay.htm

Online Bill Pay Questions • What are the two types of online bill pay? • What is automatic bill pay? • Choose link Banking 101 Choose link 3 reasons to avoid online banking. List 3 reasons given.

Common Payment Services - EFT Electronic Funds Transfer (EFT) Banking method in which computers and electronic technology is used as a substitute for checks and other paper forms of banking Electronic Funds Transfer Options: Automated Teller Machines (ATM’S) Pay-By-Phone Systems Direct Deposit or Withdrawals Paychecks, automated bill payment Point-of-Sale Transfers Debit Cards Automatic Deposits and Payments 36

Checking Accounts • Used by business and individuals to manage cash transactions • Check- • A preprinted form issued by the financial institution • Account holder directs withdrawals by writing checks • Parties to a Check • Payee, Drawee, Drawer

Parties to a Check Check Number Drawer’s Name & Address Joint Account ABA # Payee Check Date Melanie Paige Charles Paige 319 619 Main Street Raleigh, NC 27601 2-131/1034 July 16, 2010 Pay To the Order of _____Donnie Tatum______________________$100.50 _One hundred and 50/100 ---------------------------------------------------DOLLARS State Credit Union For _______________ Charles Paige 2131/1034:78434 234320 100.50 07-18-2010 2251 Drawer’s Signature - Last item completed on check! 38 Bank Name - Drawee Memo MICR Banking #s

Record Keeping • IMPORTANT: Keep a current balance in check register or on check stub by: • Recording deposits • Recording withdrawals • Checks written • EFTs • Bank Fees

Common Payment Services http://usa.visa.com/download/merchants/visa_travelers_cheques_acceptance.pdf • Special Checks • Travelers check • Requires 1st signature when check issued • Requires 2nd signature when check used Go to link below and read about traveler’s checks and how they work.

Traveler’s Checks • Traveler’s Checks – Draft drawn by a well-known financial institution on itself or its agent, used when traveling • Go to website • http://www212.americanexpress.com/dsmlive/dsm/dom/us/en/personal/cardmember/additionalproductsandservices/giftcardsandtravelerscheques/travelerschequesandforeigncurrency.do?vgnextoid=6d17fc671492a110VgnVCM100000defaad94RCRD Write questions 1-3 on notebook paper. Use the website to answer the questions. Click on Learn More about Travelers Checks. • List the 4 steps in how to use travelers checks. • List 5 ways Travelers Checks mean Peace of Mind. • What is the benefit of Cheques for Two?

Certified Check A certified check is written by a bank for you from your bank account to give to someone. It's guaranteed funds that the bank reserves from your account. Go to website: http://www.superpages.com/supertips/what-is-a-certified-check.html Write Certified Check questions 1-5 from next slide on notebook paper. Use the website to answer the questions.

Certified Check Questions • Who issues a certified check? • Give two examples of when you might need a certified check? • Why can’t a certified check bounce? • Why does a creditor require a certified check? • Do banks charge a fee for a certified check?

Cashier’s Check SampleCashier’s Check – A check the bank draws on itself

Common Payment Services • Money Order • Draft issued by a post office, bank, express company, or telegraph company for use in paying or transferring funds for the purchaser • Orders issuing agency to pay amount printed on form to another party • Types of Money Orders: • Postal money order • Express money order • Telegraphic money order • Go to website http://en.wikipedia.org/wiki/Money_order Write questions 1-5 from next slide on notebook paper. Use the website to answer the questions.

Money Order Questions • For what amount of money is a money order issued? • When was the Postal Order system established? • What is a concern about using money orders? • Who usually sells money orders in the United States? • Name 5 security features of a postal money order.

Common payment services Opening a checking account Signing a signature card is the first step Writing a check for payment Endorsing a check for deposit An endorsement allows the payee to cash the check, deposit the check or transfer payment of the check to someone else. Different types of endorsements: Blank Full Restrictive

Check Endorsements Definition: Signature on the back of a check What does an endorsement do? Allows payee to cash, deposit or transfer payment of the check to someone else Provides proof that the payee cashed or transferred payment of the check to someone else How should a check be endorsed? Endorser (payee who is signing) should sign the check the way it is on the front of the check and if the name is misspelled, correct the signature directly up under the first endorsement 48

Blank Endorsements Signed with endorser’s name only (endorser is payee from front of check) Can be cashed by anyone who holds the check with a blank endorsement! Don’t use blank endorsement before you are ready to cash or deposit! Should match payee’s name 49

Special Endorsement Transfers payment of a check to someone else. Payee signs check , then writes “pay to the order of” another person Can be used to make payment on a debt Juan is payee on check Juan owes Maria money Juan transfers payment to Maria. Debt = money owed Might also endorse: Juan Delgado pay over to Maria Fernandez