Oligopoly

Oligopoly. Powerpoint produced by Rachel Farrell (PDST) & Aoife Healion (SHS, Tullamore ) Sources of information: SEC Marking Scheme. Syllabus. Exam Questions (HL). Short. Long. 2011 Q 2 2006 Q 2 2003 Q 1 1999 Q 2. 2010 Q 4 2004 Q 4 2002 Q 5. Oligopoly.

Oligopoly

E N D

Presentation Transcript

Oligopoly Powerpoint produced by Rachel Farrell (PDST) & AoifeHealion (SHS, Tullamore) Sources of information: SEC Marking Scheme

Exam Questions (HL) Short Long 2011 Q 2 2006 Q 2 2003 Q 1 1999 Q 2 • 2010 Q 4 • 2004 Q 4 • 2002 Q 5

Oligopoly • Is a market form in which a market or industry is dominated by a small number of sellers who likely to be aware of the actions of the others and can influenceprice or quantity sold. • Proctor & Gamble, Unilever, Tesco…..

Examples • Petrol/Oil: Topaz, Esso.. • Motor: Ford, Toyota, Nissan • Retail Banks: AIB, BOI • Supermarkets: Tesco, Dunnes • Detergent Manuf: P & G. Unilever

Assumptions of oligopolies 1. Few large firms • There are a few large firms that dominate the industry. • They can influence the price or quantity produced.

2. Firms interact with each other • Firms in oligopoy do not act independently of each other. • They take into account the likely reactions of their competitors.

3. Product differention • Firms sell similar products. • They engage in competitive advertising. • They engage in brand marketing. • They try to convince consumes that their product is better.

Is an agreement among firms to divide the market, set prices, or limit production. Eg. OPEC 4. Collusion

5. Firms may pursue objectives other than profit maximisation a) Maximise sales: • Once a certain level of profit has been earned the firm may concentrate on increasing their share of the market. b) Prevent government intervention: • Firms may fear that SNP would attract a government investigation and restrict their activities.

6. There may be barriers to entry into the industry • Firms may not be able to enter the industry because of: • Economies of scale • Limit pricing • Control over the channels of distribution • Brand proliferation

Barriers to Entry 1. Economies of Scale • Large firms produce on a large scale and benefit form decreased cost per unit . • If a new firm tries to enter the market the existing firm that is well established can afford to lower price to deter them. • New firms will be unable to compete due to the huge set up costs involved.

Limit Pricing • Is an agreement between firms to set a relatively low price to make it unprofitable for new firms to enter the industry.

Control over the channels of distribution • Ologopolies may refuse to supply retailers who stock the products of competitors.

Brand Proliferation • The same firm produces several brands of the same type of product. • This will leave very little room for new firms to competitor.

Research!!!! • Look at the household products in your own home to see what company produces them.

Non price competition2010 SQ 4 • Is when competing firms try to increase sales/market share by methods other than changing prices.

Examples • Branding: To create loyalty and recognition. • Packaging: Distinctive to competitors. • Competitive advertising: Creates difference in the minds of consumers.

Opening hours: Extended, 24/7. • Quality of service: Layout, staff, services. • Sponsorship: Of local or national events. • Special offers: Gifts, coupons, loyalty cards.

Benefits of non-price comp to consumers2002 SQ 5/2011 Q 2 1. Consumer loyalty rewarded • Consumers can receive loyalty points which can be used as they wish. 2. Stability in prices • Consumers will be better able to budget as prices will not always be changing. 3. Better quality commodities / services • Firms may offer better service and/ or after sales service to consumers. 4. More informed consumers • Through advertising consumers may get more information about products and services and so can make more informed choices.

Price competition • Is when competing firms try to increase sales/market share by changing price.

Benefits of price competition to consumers 1. Lower prices • Consumers will be able to get better value from their limited income. 2. More choice • Consumers will have a greater disposable income and can decide what to spend it on. 3. Preferable to NPC because; • Special offers of NPC may be unwanted • Vouchers may be unused.

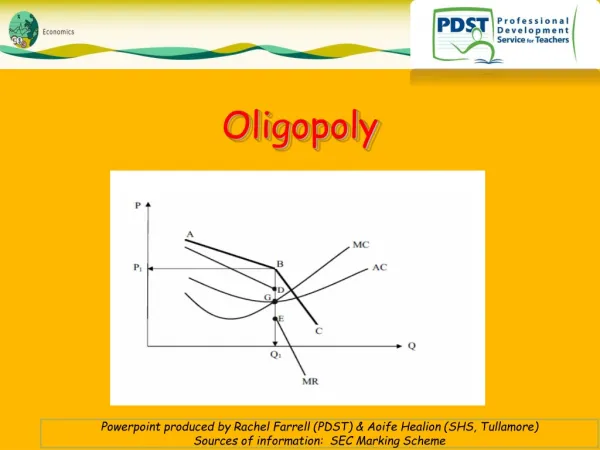

Shape of the demand curve of a firm in oligopoly • If the price leader sets the price at B then all firms face a kinked demand curve ABC.

Kinked Demand Curve (2011/2006/2003) Elastic demand curve increase in price, lose many customers D = AR A Price P1 B Inelastic demand curve decrease in price, gain few customers C Q1 Quantity

1. Along the elastic demandcurve above point B, if a firm increases price it will lose many customers and revenue. 2. Along the inelastic demand curve below pon B, if a firm decreases price so will competitors, so it will gain few customers but will lose revenue.

Relationship between the demand curve and the marginal revenue curve. • Because the D/C is kinked the firms MR curve consists of two distinct parts. • It is constant between D and E. • Between these points if MC changes, price will not change.

Relationship between the demand curve and the marginal revenue curve. D A D = AR Price P1 B MR E C Q1 Quantity

Price rigidity/Sticky prices • Prices tend not to change when costs change in oligoploy. • Firms fear the reaction of their competitors. • If a firm increase price their competitor will not, so they will lose customers & revenue. • If a firms decrease price so will competitors, so they will not gain customers and lose revenue.

Constant prices • Firms in oligopoly may not increase prices when costs increase as it may cost more to change catalogues and price lists than change the price. • In this case the oligopolist will absorb the price increase themselves.

Long run equilibrium of a firm in oligopoly • Eq is where MC=MR & MC is rising. • This occurs at point G on the diagram. • The firm will produce at Q 1 • The firm will charge price P 1 • Due to barriers to entry firms may earn SNP if AR > AC. • Even if costs rise between D & E prices remain rigid at P 1.

Sweezy’s kinked demand curve explained price rigidity in the 1930’s. • However in the 1970’s oligopolies did increase prices due to oil prices. • In the 1980’s oligopolists increased prices due to increased demand.

Question • Do you believe that the Irish retail market for banking services operates under oligopolistic conditions?

Yes • Few sellers………. • Interdependence between firms……… • Close substitutes……………… • Remember headings, bullet points & examples.