Download

1 / 22

220 likes | 322 Vues

Learn how to assess past and future profitability using financial statements and stock prices. Understand key metrics like profit margin, ROE, and earnings per share to make informed decisions. Gain insights into leveraging market data for financial analysis.

E N D

Measuring Profitability James Dow For GBUS 600 Spring 2004

Outline (1) Using financial statements to evaluate past profitability. (2) Using financial statements to think about future performance. (3) Using stock prices to think about future performance.

(1) Using financial statements to evaluate past profitability. • Useful when assessing management. • Perhaps useful for forecasting future. • Historical information is what you want.

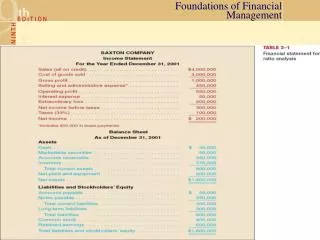

Quick Overview of Financial Statements • Annual Report • Income Statement • Balance Sheet

Income Statement • Revenue - Costs = Earnings • Net Earnings or Income = Profits

Is $300 Million a Lot? • Profit margin (earnings/sales)? • What about earnings per share? • Return on equity (earnings/equity)

Balance Sheet • Assets = Liabilities + Equity • Equity is like “net worth” • “Book” (historical) value of equity

Is 15% a Lot? • Opportunity cost of generating earnings. • Cost of capital • ROE – cost of equity

Problems with ROE • Only one period of earnings. • Need longer history for evaluating past. • Need future earnings for future. • Book value of equity vs. market value. • Can we get information from market value?

(2) Using financial statements to think about future performance. • This is a business question. • Historical financial information provides clues. • Market prices also provide information.

Income Statements in More Detail • Revenues • - Costs of goods sold • - Other costs (such as) Administrative Costs Research Costs Interest and Taxes Extraordinary Items = Net Earnings

Why report different costs? • Why split out administrative costs? • Why split out extraordinary items?

Thinking about the Future • What will change? • How will that affect the financial position? • A quick comment on financial ratios.

(3) Using stock prices to think about future performance. • Stock price represents the value of a company. • The value of a company depends on future prospects. • Stock price depends on future prospects. • But how? We need a theory!

An oversimplified theory of stock prices • ROE = (total earnings)/(book equity) • Earnings yield • = (total earnings)/(market capitalization) • = e/p (inverse of p/e ratio)

More Oversimplified Theory • e/p should equal opportunity cost of investing in stocks. • Changes in e produce changes in p. • Of course, it’s future e’s that really matter.

Things That Affect Stock Prices • Current and future earnings. • Risk of the particular stock. • Attitudes towards stock in general. • Attitudes towards saving in general.

Using Stock Prices • Use price information to judge earnings prospects. • How to separate firm specific factors from other forces? • Compare with the “average” behavior of stocks.

Figure 3. Relative Stock Performance: International Paper and S&P 500. S&P500 International Paper

Conclusion • Know your question! • Use financial data to guide your investigations. • Use financial data to support your analysis.