Download

1 / 1

10 likes | 187 Vues

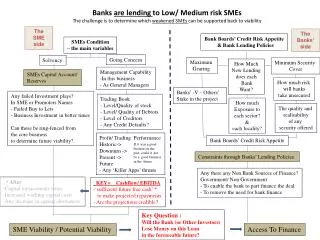

Banks are lending to Low/ Medium risk SMEs The challenge is to determine which weakened SMEs can be supported back to viability . The SME side. The Banks’ side. Bank Boards’ Credit Risk Appetite & Bank Lending Policies. SMEs Condition – the main variables. Going Concern. Solvency.

E N D

Banks are lending to Low/ Medium risk SMEs The challenge is to determine which weakened SMEs can be supported back to viability The SME side The Banks’ side Bank Boards’ Credit Risk Appetite & Bank Lending Policies SMEs Condition – the main variables Going Concern Solvency Maximum Gearing Minimum Security Cover How Much New Lending does each Bank Want? • Management Capability • In this business • As General Managers SMEs Capital Account/Reserves How much risk will bankstake unsecured Banks’ -V – Others’ Stake in the project • Any failed Investment plays? • In SME or Promoters Names • Failed Buy to Lets • Business Investment in better timesCan these be ring-fenced from the core business to determine future viability? Trading Book - Level/Quality of stock- Level/ Quality of Debtors- Level of Creditors- Any Credit Defaults? How much Exposure to each sector? & each locality? The quality and realisability of any security offered Profit/ Trading PerformanceHistoric-> Downturn ->Present -> Future- Any ‘Killer Apps’ threats Bank Boards’ Credit Risk Appetite If it was a good business in the past, could it not be a good business in the future Constraints through Banks’ Lending Policies Any there any Non Bank Sources of Finance?Government/ Non Government - To enable the bank to part finance the deal- To remove the need for bank finance • * After • Capital replacements costs • Increased working capital costs • Any decrease in capital allowances • KEY= Cashflow/ EBITDA • ‘sufficient future free cash’ * to make projected repayments • Are the projections credible? Key Question : Will the Bank (or Other Investors) Lose Money on this Loan in the foreseeable future? SME Viability / Potential Viability Access To Finance