Rezidor Hotel Group AB FY 2010

210 likes | 759 Vues

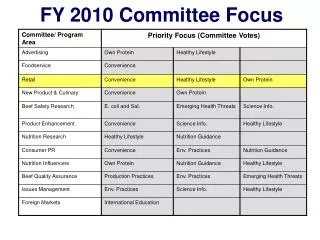

Rezidor Hotel Group AB FY 2010. Mars 2011. Top 10 Hotels Players in Europe Rezidor ranks 5 th in number of rooms, first on the upscale segment (with its brand Radisson Blu ). As of Dec. 2010. (1) . Only Midscale. (1) . (1) . Resort. (1) . Resort. (1) . Only UK.

Rezidor Hotel Group AB FY 2010

E N D

Presentation Transcript

RezidorHotel Group ABFY 2010 Mars 2011

Top 10 Hotels Players in EuropeRezidor ranks 5th in number of rooms, first on the upscale segment (with its brand Radisson Blu) As of Dec. 2010 (1) OnlyMidscale (1) (1) Resort (1) Resort (1) Only UK Sources: MKG Hospitality – Feb. 2011, Companies annual reports 2010 and corporate website (1)Nb of rooms based on internal estimates 2

Rezidor Hotel Group AB.Summary 1. Company overview Slide 3 2. Company organization Slide 4 3. Brands positioning Slide 5 4. Geographical breakdown Slide 6 5. Operating mode Slide 7 6. Group strategy Slide 8 7. Pipeline and lodging development Slide 10 8. Key figures Slide 11 9. SWOT analysis Slide 13 10. Company history Slide 14 11. Brands description Slide 15 Rezidor – Company profile FY 2010

1. Company overview Nordic Europe (2) Nordic Europe(2) Western Europe Western Europe Eastern Europe Eastern Europe MEA MEA # rooms segment # hotels Revpar ADR OR Description Main Shareholders • Rezidor is a Hospitality Swedish company operating in the traditional lodging industry • Three main brands: Radisson Blu, Park Inn by Radisson and Hotel Missoni • Asset-light business model • 4,947 employees • Fifth hotel player in Europe (in nb of rooms) • Radisson: largest upscale hotel brand, according to MKG • Segmented portfolio: Luxury/Lifestyle (Hotel Missoni), Upscale (Radisson Blu), Midscale (Park Inn by Radisson), Limited service (Country Inn) • Presence in 48 countries through EMEA • Radisson Blu and Park Inn by Radisson developed in EMEA under Master Franchise Agreements with Carlson • Listed on the NASDAQ OMX Stockholm Exchange on November 2006 Main Figures Segmental Revenue and EBITDA Revenue EBITDA (1) Excluding Western Europe negative EBITDA (-€4.6m) Incl. Denmark, Finland, Iceland, Norway and Sweden Sources: Reuters as of 28 April 2011, Rezidor Annual Report 2010, Rezidor website Rezidor – Company profile FY 2010

Rezidor Hotel Group AB (Sweden) 100% shares and votes Rezidor Hotel Holding AB (Sweden) 100% shares and votes Rezidor Hospitality A/S (Denmark) 100% shares and votes 100% 100% 100% 100% 100% Rezidor Hotels ApS Danmark (Denmark) Rezidor Regent A/S (Denmark) Rezidor Sweden AB (Sweden) Rezidor Park ApS (Denmark) Rezidor Loyalty Management A/S (Denmark) 100% 100% 100% 100% 100% Rezidor Russia A/S (Denmark) Rezidor Comerstone A/S (Denmark) Rezidor Hospitality Norway AS (Norway) Rezidor Country A/S (Denmark) Rezidor Lifestyle A/S (Denmark) 2. Company organizationGroup companies and legal structures Sources: Company reports Rezidor – Company profile FY 2010

3. Brand positioning Hotels / rooms / countries Luxury (% of room network) 1 h. / 136 r. / 1 c. Upscale (% of room network) 200 h. / 46,122 r. / 48 c. (2) Midscale (% of room network) 103 h. / 19,232 r. / 26 c. (1) Economy (% of room network) 2 h. / 133 r. / 2 c. Source: RezidorAnnual Report 2010 NB: 6 Regenthotelsincluded in Otherhotels in Annual Report 2 Country Inn hotels in EMEA (Germany and Austria) Full Service Limited Service Rezidor – Company profile FY 2010

4. Geographical breakdown Hotel and room network As of December 31st, 2010 312 h, 66,375 r 20% 56h 12,945r Nordic Europe 23% 60 h 15,071r Eastern Europe 44% WesternEurope 160 h 29,406r 13% 36 h 8,953r Middle-East, Africa & Others Share ofglobalnetwork (in nb of r) X% Rezidor – Company profile FY 2010 Source: Rezidor Annual Report 2010

Franchised Owned Leased Managed 5. Operating mode 2002 133 h. / 28,900 r. 2010 312 h. / 66,375 r. +37,745 rooms +130% over 8 years Source: Rezidor Annual Report 2002 & 2010 Rezidor – Company profile FY 2010

6. Group strategyImportant developments of the year • Park Inn by Radisson • New name launched in Q2 2010 • Link with Radisson’s brand image to enhance further growth • Sale of Regent • Positive effect of M€ 5.7 • Management services still provided to Regent hotels after sale • Portfolio agreement in the Baltics • Agreement to re-brand 10 Reval hotels (ca 2,400 rooms) in the Baltics to Radisson Bluand Park Inn • Agreement to strengthen Rezidor’s position in the key markets Riga, Tallinn and Vilnius • Carlson’s shareholding • Carlson, Rezidor’s major shareholder, has increased its shareholding to 50.03% of the registered shares in May 2010 Brand strategy M&A Development strategy Ownership Source: Rezidor Annual Report 2010 Rezidor – Company profile FY 2010

6. Group strategyStrategic axes • Margin improvement: EBITDA target margin of 12% • Tight cost control (following the cost reduction program of 2009) • Substantial increase in cash flow in 2010 allows increase in maintenance Capex • Fixed-lease structure to be maintained in Western Europe • Asset light strategy • Increasing proportion of managed and franchised hotels (95% of the pipeline vs. 74% of the actual portfolio) • Hotels conversions privileged in some specific markets such as UK, Germany and Russia for Park Inn brand, while Radisson Blu expansion mainly through new builds • Focus on expansion of core brands: Radisson Blu, Park Inn by Radisson • Disposal of peripheral assets: sale of Regent luxury brand to Formosa in April 2010 • Key priority to boost brand awareness as a mean to increase RevPar penetration: new name for Park Inn followed by a major new marketing and sales campaign in 2011, mainly in UK • Expansion plans in emerging countries • Focus on Russia/CIS and Africa: strong economic growth, undersupply or old inventory combined with high room demand and low operating costs • Emerging markets represent over 70% of the pipeline (vs. 36% of rooms in operation) • Radisson Blu: key to entering new markets, Park Inn usually following the footsteps of Radisson Blu • Rezidor is considering to enter the economic segment in Middle East, Russia and Africa under a new brand*. Rezidor – Company profile FY 2010 Sources: Rezidor Annual Report 2010 *Press review as of March, 2011

7. Pipeline and lodging development Business Development in 2010 • Openings: +7,173 r. (32 h.) • Closings: -1,444 r. (6 h.) • Net evolution: +5,279 r. (+9,4%) Pipeline 2011-2015 : 21,493 additional rooms (32% of the current network), incl. 8100 new rooms signed in 2010 Per region Per brand Per contract type Nordic Europe Radisson Leased Western Europe Park Inn Managed Eastern Europe Missoni Franchised MEA Focus on Eastern Europe and MEA Two core brands: Radisson Blu and Park Inn by Radisson +95% current pipeline managed & franchised Source: Rezidor Annual Report 2010 Rezidor – Company profile FY 2010

8. Key figuresP&L evolution & forecasts Rezidor – Company profile FY 2010

9. SWOT analysis Strength Weaknesses • Strong support of the worldwide group Carlson, which owns 50.1% of the company • Large product range, from midscale to luxury • Large brand awareness in Scandinavia • Leadership in Scandinavia • Good business model (upscale with maximum pricing power, strong operating leverage, no debt, well positioned to win management contracts) • Geographical footprint limited to EMEA • Expensive lease commitments • Dependence on Carlson • Poor business control, especially as Rezidor pursues an aggressive growth plan • Bad ratings in customer satisfaction surveys • Difficulties in securing new hotel contracts or keeping/prolonging maturing contracts Opportunities Threats • Improving business mix (asset light management contracts) • Well positioned for recovery, thanks to costs measures implemented in 2009 • Growing share of the branded hotels trend for conversion from unbranded to branded hotels • Strong room rollout potential • Central and Eastern Europe as one of the world’s fastest emerging travel markets • Intense competition, with a large number of players, especially in Europe Source: Broker research, June 2010 Rezidor – Company profile FY 2010

10. Company history 2009 2006 2010 Sale of Regent Hotels to Formosa Radisson SAS becomes Radisson Blu Rezidor goes public on the Stockholm Stock Exchange 2005 Hotel Missoni is launched, in partnership with the Italian fashion brand of the same name Multi brand franchised master agreement, adding 3 other Carlson’s brands to Rezidor Portfolio: Regent, Park Inn and Country Inn 2002 2001 SAS International Hotel becomes Rezidor First master franchise agreement with CarlsonRadisson SAS is born 1994 First hotel outside Scandinavia: SAS Hotel Kuwait 1980 Scandinavian Airlines founds the company SAS International Hotels by opening its first hotel, the SAS Royal Hotel in Copenhagen 1960 Rezidor – Company profile FY 2010 Source: Rezidor Website

11. Brands description • Full Service Rezidor – Company profile FY 2010 Source: Rezidor Annual Report 2010

11. Brands descriptionFull service – Hotel Missoni Overview Network Full service, upper upscale brand • Focusing on lifestyle and design aspects • License agreement with the italian fashion house of the same name • Woldwide licensing agreement • First Hotel opening in 2009 Main competitors • So by Sofitel, W, Morgans, Malmaison, Bulgari, Armani • Network • 2 hotels, 305 r. (incl. newly opened Missoni Kuwait City) • Pipeline = 3 hotels / 508 rooms Locations • Fashionable cities as well as in up-and-coming resort areas • Geographical breakdown • Worldwide, with a focus on Europe and the Middle East • Two hotels operated in Edinburgh and Kuwait • Future openings include Oman, South Africa, Brazil Rezidor – Company profile FY 2010 Source: Rezidor Website

11. Brands descriptionFull service – Radisson Blu Overview Network Full service, upscale brand • Largest Rezidor hotel brand • Largest upscale hotel brand in Europe • Ranging from small boutique hotels to major city landmarks • Managed / Leased contracts • Trademark of Carlson, master franchise agreement with Carlson until 2032, with the option to extend the agreement until 2052 New architecture and design policy • Rebranded as Radisson Blu in 2009 • Key figures FY 2010 • ADR: €110.3 • RevPar: €70.5 • Occupancy Rate: 63.9% Main competitors • Pullman, Hilton, Marriott H&R, Sheraton • Network • 200 hotels / 46,122 rooms in operation= 230 rooms per hotel on average • Pipeline: 52 hotels / 12,922 rooms Locations • Mainly located in city centers, leisure resorts and airports FY 2009 • ADR: €105.95 • RevPar: €65.9 • Occupancy Rate: 62.2% Rezidor – Company profile FY 2010 Source: Rezidor Annual Report 2010, Rezidor Website

11. Brands descriptionFull service – Park Inn (1/2) Overview Network Full service, midscale brand • New name to be used from January 2011: Park Inn by Radisson • Mainly operated under franchise agreements • Targeted markets: UK, Germany and Russia (growth mainly driven by conversion) • Trademark of Carlson, master franchise agreement with Carlson until 2032, with the option to extend the agreement until 2052 • Key figures FY 2010 • ADR: €64.5 • RevPar: €37.5 • Occupancy Rate: 58.0% Main competitors • Novotel, Scandic, Holiday Inn • Network • 87 hotels / 16,121 rooms in operation= 185 rooms per hotel on average • Pipeline = 51 hotels / 9,408 rooms Locations • City centers, suburban locations and transport terminals FY 2009 • ADR: €63.8 • RevPar: €33.6 • Occupancy Rate: 52.6% Rezidor – Company profile FY 2010 Source: Rezidor Annual Report 2010, Rezidor Website

11. Brands descriptionPark Inn (2/2) : affiliation brand strategy case study 2000 2002 2010 2003 • Rebranding operation to Park Inn by Radisson to enhance further growth • Carlson signs a master franchise agreement with The Rezidor Hotel Group to develop Park Inn in EMEA • Rezidorrelaunches Park Inn. First hotel in Berlin • Carlson acquires the Park Inn brand from Olympus Hospitality Group • Park Inn by Radisson is a “fresh and energetic” midscale hotel brand (119 hotels / 85% in Europe) • Relaunched in 2003, stand-alone brand until 2010, when an affiliation to Radisson wasdecided (starting Jan 2011) • New name is in line with Rezidor decision to focus its dvlp on its two core brands, Radisson and Park Inn • Objectives : The link with Radisson and its great strength and reputation will allow Park Inn to grow faster and to increase the brand awareness. But no repositioning / upgrade seems to be planned. • Implementation Plan : • The rebranding process will start in Park Inn’s key home market, the United Kingdom, before extending the process across Europe, Middle East and Africa. • The transition of Park Inn hotels to Park Inn by Radisson will be completed by the end of 2011. • First Park Inn by Radisson in Brazil, developed by Atlantica Hotels International • Pipeline1 : 41 in EMEA, 3 in North America , 2 in APAC (India), 2 in Latin America 1LodgingEconometrics Q4 2010

11. Brands descriptionLimited service – Country Inn Overview Network Limited service, economy brand • Brand under development, currently under review by Rezidor • Trademark of Carlson, master franchise agreement with Carlson until 2032, with the option to extend the agreement until 2052 Main competitors • Ibis • Network • 2 hotels / 133 rooms in operation • Geographical Breakdown • Germany • Austria Rezidor – Company profile FY 2010 Source: Rezidor Annual Report 2010, Rezidor Website