Download

1 / 7

70 likes | 256 Vues

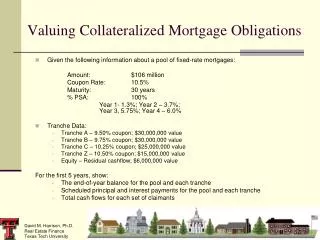

Valuing Collateralized Mortgage Obligations. Given the following information about a pool of fixed-rate mortgages: Amount: $106 million Coupon Rate: 10.5% Maturity: 30 years % PSA: 100% Year 1- 1.3%; Year 2 – 3.7%; Year 3, 5.75%; Year 4 – 6.0% Tranche Data:

E N D

Valuing Collateralized Mortgage Obligations • Given the following information about a pool of fixed-rate mortgages: Amount: $106 million Coupon Rate: 10.5% Maturity: 30 years % PSA: 100% Year 1- 1.3%; Year 2 – 3.7%; Year 3, 5.75%; Year 4 – 6.0% • Tranche Data: • Tranche A – 9.50% coupon; $30,000,000 value • Tranche B – 9.75% coupon; $30,000,000 value • Tranche C – 10.25% coupon; $25,000,000 value • Tranche Z – 10.50% coupon; $15,000,000 value • Equity – Residual cashflow; $6,000,000 value For the first 5 years, show: • The end-of-year balance for the pool and each tranche • Scheduled principal and interest payments for the pool and each tranche • Total cash flows for each set of claimants