Download

1 / 0

0 likes | 180 Vues

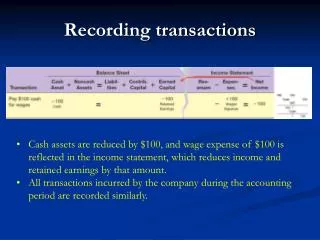

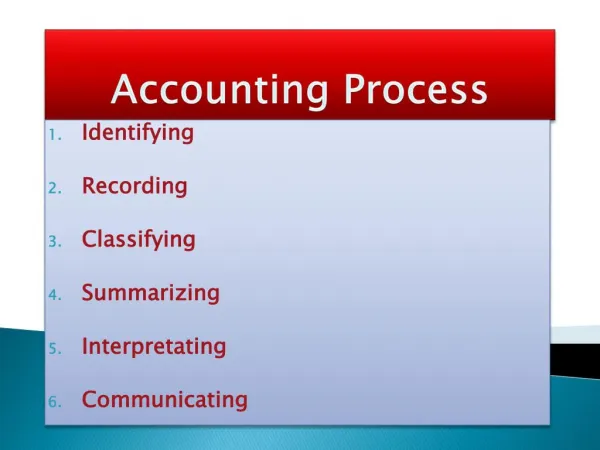

Recording Business Transactions. Chapter 2. The Accounting Process. Record transactions in the journal. Copy (post) to the ledger. Prepare the trial balance. The Account. Basic summary device

E N D