Download

1 / 34

350 likes | 541 Vues

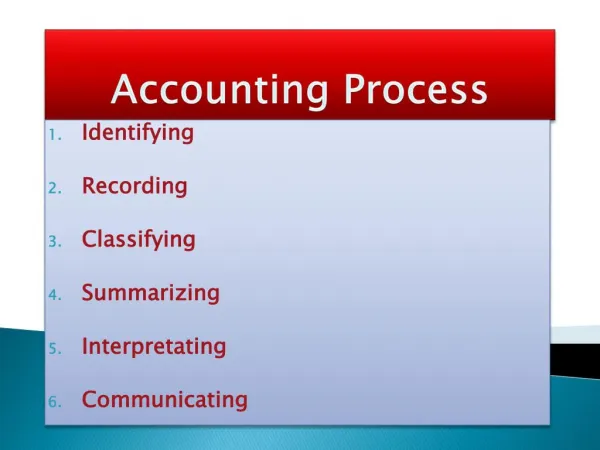

Recording Business Transactions. Appropriate business documents prepared or received (Source documents). Record transactions in journals. Input. Post transactions to ledgers. Invoices. Bank Statements. Financial reports (income statement and Balance sheet). The accounting process.

E N D

Appropriate business documents prepared or received (Source documents) Record transactions in journals Input Post transactions to ledgers Invoices Bank Statements Financial reports (income statement and Balance sheet) The accounting process Trial Balance

Components of an Accounting system • Source documents • Special journals • Subsidiary ledgers • General ledgers (Control account)

Bank Statements Employee Records Invoices Cheques Source Documents Source documents

Accounts • The account is the basic summary devise of accounting (file label). • Accounts are grouped into three broad categories. • Assets, Liabilities and Owners’ Equity.

Accounting Terms • Account: • a basic component of an accounting system • Ledger: • a group of accounts • Assets: • economic resources

Accounting Terms • Liabilities: • debts or other obligations to an outside party (not the owner) • Owners’ equity: • owners’ claims on the assets owned by the business

Accounting Terms • Double-entry bookkeeping: • all transactions have at least two effects on the entity • T-account: • an account format used to show the effect of transactions • It takes the form of a capital letter “T”.

Assets • Something a business owns that has future economic value.

Classification of Accounts Asset Accounts • Cash at Bank • Bills Receivable • Accounts Receivable • Inventories • Prepaid Expenses • Land • Building • Equipment, Furniture and Fixtures

Liabilities • Something that an entity owes - a debt.

Classification of Accounts • Liability Accounts • Bills Payable • Accounts Payable • Accrued Liabilities (for expenses incurred but not paid) • Non-Current Liabilities ( debentures or mortgage)

Classification of Accounts • The Owners’ equity (Capital) shows the owners’ claim to the assets of the business after total liabilities are subtracted from total assets.

Owners’ Equity Accounts • Capital: • owners’ interest in the business • Drawings: • owners’ withdrawals of cash or other assets from the business

Owners’ Equity Accounts • Revenues: • income earned from performing services or sales • increase owners’ equity • Expenses: • costs incurred in operating a business • decrease owners’ equity

Jane’s Service Station • Assume that the business sold $4,000 worth of petrol on a given day and performed $2,000 of repair services. • How much revenue did the business earn that day? • $6,000

Jane’s Service Station • Revenues increase Jane’s equity in the business. • The business had to pay mechanics and suppliers $3,750 for the work performed that day.

Jane’s Service Station • Expenses decrease Jane’s equity in the business. • How much was the net increase in Jane’s equity that day? • $2,250

Double-Entry Accounting • Double entry bookkeeping means to record the dual effects of each business transaction. • Assets = Liabilities + Owners’ Equity • Assets are on the left (debit side). • Liabilities and Equity are on the right (credit side).

The left side is the debit side. The right side is the credit side. Debits and Credits

The T-Account Account Title DEBIT CREDIT LEFT SIDE

The T-Account Account Title DEBIT CREDIT RIGHT SIDE

Rules of Debit and Credit • Increases in liabilities and owners’ equity are recorded on the right (credit side). • Increases in assets are recorded on the left (debit side).

Rules of Debit and Credit • Decreases in liabilities and owners’ equity are recorded on the left (debit side). • Decreases in assets are recorded on the right (credit side).

The Double Entry System • Each transaction is recorded with at least: • One debit • One credit • Total debits must equal total credits. • The whole system is always in balance.

The T-Account...Assets Account Title Credit Debit Assets IncreaseDecrease

The T- Account...Liabilities Account Title Debit Credit LiabilitiesDecreaseIncrease

– – + + Owner’s Capital Owner’s Withdrawals Revenues Expenses The Account and its Analysis = + Assets Liabilities Equity

A T-account represents a ledger account and is a tool used to understand the effects of one or more transactions. Debits and Credits

= + Assets Liabilities Equity EQUITIES ASSETS LIABILITIES Debit Credit Debit Credit Debit Credit +- - + - + Double-Entry Accounting

_ _ Owner’s Capital Owner’s Withdrawals + Revenues Expenses Capital Withdrawals Revenues Expenses Debit Credit Debit Credit Debit Credit Debit Credit - + +- - + +- Double-Entry Accounting Exh. 3.8 Equity