Download

1 / 14

210 likes | 630 Vues

Next Page Click Here. Types of Cost Behavior Patterns. Total Long Distance Telephone Bill. Minutes Talked. Next Page Click Here. Total Variable Cost Example. Your total long distance telephone bill is based on how many minutes you talk (the more you talk, the higher the bill).

E N D

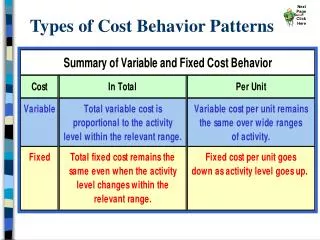

Next Page Click Here Types of Cost Behavior Patterns

Total Long DistanceTelephone Bill Minutes Talked Next Page Click Here Total Variable Cost Example Your total long distance telephone bill is based on how many minutes you talk (the more you talk, the higher the bill).

Per MinuteTelephone Charge Minutes Talked Next Page Click Here Variable Cost Per Unit Example The cost per minute talked is constant(for example, 10 cents per minute).

Monthly Basic Telephone Bill Number of Local Calls Next Page Click Here Total Fixed Cost Example Your monthly basic telephone bill is probablyfixedand does not change when you make more local calls.

Monthly Basic Telephone Bill per Local Call Number of Local Calls Next Page Click Here Fixed Cost Per Unit Example The fixedcost per local call decreasesas more local calls are made.

Next Page Click Here Fixed Costs and Relevant Range The company’s normal operating range 90 Total cost doesn’t change for a wide range of activity.It then jumps to a new higher cost for the next higher range of activity. Relevant Range 60 Rent Cost in Thousands of Dollars 30 0 0 1,000 2,000 3,000 Rented Area (Square Feet)

How does this type of fixed cost differ from a step-variable (or step-wise) cost? • Step-variable (or step-wise) costs can be adjusted more quickly and . . . • The width of the activity steps is much wider for the fixed cost. Next Page Click Here Fixed Costs and Step-Variable (or Step-Wise) Costs

Total cost increasesto a new higher cost for the next higher range of activity. Total costremains constant within a narrow range of activity. Next Page Click Here Step-Variable (or Step-Wise) Costs Cost Activity

Next Page Click Here Mixed Costs A mixed cost has both fixed and variable components. Consider thefollowing electric utility example.

Next Page Click Here Y Variable Utility Charge Fixed MonthlyUtility Charge X Mixed Costs Total mixed cost Total Utility Cost Activity (Kilowatt Hours)

Next Page Click Here The High-Low Method WiseCo recorded the following production activity and maintenance costs for two months: • To break down the mixed cost,these two levels of activity are used to: • compute the variable cost per unit; • compute the fixed cost; and then • express the costs in equation form Y = a + bX.

Next Page Click Here The High-Low Method Unit variable cost = Changein costChange in units Unit variable cost = $3,600 ÷ 4,000 units = $0.90/unit

Next Page Click Here The High-Low Method Unit variable cost = $3,600 ÷ 4,000 units = $0.90/unit Fixed cost = Total cost – Total variable cost Fixed cost = $9,700 – ($0.90 per unit × 9,000 units) Fixed cost = $9,700 – $8,100 = $1,600

Next Page Click Here The High-Low Method Unit variable cost = $3,600 ÷ 4,000 units = $0.90/unit Fixed cost = $9,700 – ($0.90 per unit × 9,000 units) Fixed cost = $9,700 – $8,100 = $1,600 Total cost = Fixed Cost + Total variable costY = a + bX Y = $1,600 + $0.90X