Inflation and Monetary Policy

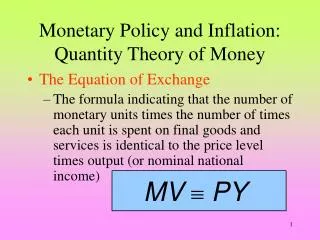

Inflation and Monetary Policy General Lecture Topic Relax first Fisher Assumption “no inflation” This means we now allow money to exist, not just real goods as in basic model. We must now distinguish between nominal (money) and real interest rates Monetary policy becomes possible

Inflation and Monetary Policy

E N D

Presentation Transcript

General Lecture Topic • Relax first Fisher Assumption “no inflation” • This means we now allow money to exist, not just real goods as in basic model. • We must now distinguish between nominal (money) and real interest rates • Monetary policy becomes possible

Specific Topics • Nominal and real interest rates • Data sources • Implications for financial innovation • Monetary policy • How the Fed controls the money supply • How the money supply (monetary policy) enters the loanable funds model • Limits of monetary policy

Definitions • Nominal interest rate • Interest rate in money terms • As reported in financial press etc. • Real interest rate • Interest rate in terms of purchasing power • Calculated by reducing nominal return by the amount of inflation

Backward looking vs. Forward looking interpretation • This calculation can only be done after-the-fact. After inflation is known • The forward-looking approach – that relates nominal and real interest rates today is more interesting • Here expected inflation is used instead of realized inflation

Fisher Equation:relates real and nominal interest rates (1+i) = (1+r)(1+α) Or, approximately i = r + α Where i = nominal interest rate r = real interest rate α = expected inflation

Logic of the relation • A lender requires / a borrower will pay • Increased purchasing power in return for delaying consumption. This is the real interest rate, determined by the loanable funds model. • The nominal interest rate includes this and, since it is quoted in money terms, compensation for the expected loss in purchasing power of money (expected inflation)

Events that effect nominal rates • Any factor that affects real rates [productive opportunities, tastes, endowments] • Any news that affects expected inflation [e.g. past inflation, policy, etc.]

Monetary policy affects nominal interest rates in two ways If the money supply is increased • Nominal interest rates decrease because of the direct effect on real interest rates • Nominal interest rates increase • Because inflation and expected inflation increase • This is the inflationary expectations effect

What is the real rate now? real = nominal – expected inflation Nominal interest rates • Current data • Historical data: (e.g. FRED: Federal Reserve Economic Data) 10 year treasury

Inflation Data • FRED summary Inflation • Original source: Bureau of Labor Statistics www.bls.gov/cpi

For net result: history of real rate (See text p. 61)

Alternative market information TIPS: Treasury Inflation Protected Securities • At each coupon payment date, face value adjusts in proportion to realized inflation (lagged) • Thus the nominal amount of coupon and final principal payment offsets inflation (see text p. 72)

TIPS • Thus TIPS coupon can be thought of as being quoted in real terms (what’s left after removing effect of inflation from the nominal payment received.) • The YTM calculated from the coupon is a real yield.

Historical TIPS Data • 30 year bond ’98 to present • 10 year note 2000 to present

Current TIPS Data • Wall Street Journal • Markets • Market Data

Financial Instruments based on inflation • Government bonds • TIPs (or other index) • Foreign currency denominated • Private sector bonds • Indexed • Gold or commodity linked

Inflation instruments asfinancial innovation Recall: ordinary loans as financial innovation • Innovation profitable if GFT created • GFT result from differences • For ordinary loans differences in productive opportunities, tastes, endowments

Do TIPS allow new GFT? • What new choices do they offer investors? • Differential exposure to inflation • New GFT trade possible if investors differ in their desired exposure to inflation due to • differing opinions about amount of inflation • differing willingness to bear inflation risk

TIPS: Summary • Potential source of data about the real rate of interest (or market expectations about inflation) • Does illustrate GFT from innovation but: • A public, not private, innovation • Timing (in an interval of relatively low and stable inflation) not typical

Money and the banking system • Banks hold reserves as deposits at the Fed • In this sense the Fed is the bankers’ bank • Banks borrow and lend these Fed Funds • Banks must hold reserves in proportion to deposits • Bank deposits (checking accounts) are the most important form of money • The link between Fed Funds and bank deposits permits control of the money supply

Tools of monetary policy • Open market operations: Buying or selling bonds • Rediscount rate: The rate at which the fed loans to banks • Reserve requirement: The proportion of deposits that must be held as reserves (non-interest bearing) with the Fed.

Open market operations • The Fed buys (sells) bonds creating (extinguishing) reserves in payment • This is by far the most common tool of monetary policy • Note that creating reserves to pay for goods and services is fiscal, not monetary policy • We limit attention to pure monetary policy

How the money supply (monetary policy) enters the Fisher Model

Basic idea Changing money supply affects supply of loans (of loanable funds)

Preliminary observations • Note: The Fisher Model works with real interest rates and real quantities • Nominal interest rates found by adding on expected inflation • It is also convenient to consider only demand and supply of loans to private borrowers (corporation)

Interpretation of curves • Demand is demand for loans by firms (real borrowing as a function of real interest rate) • Supply is household supply of loans net of government borrowing. • Resulting quantity is private borrowing • It directly reflects demand for investment • Resulting interest rate applies to all

If Fed wants lower interest ratesit increases money supply • Buys bonds, putting money in the accounts of households • Households relend these funds to firms • Supply (to private sector) shifts out • Interest rate falls • Private borrowing and investment increase

This is the direct effect or liquidity effect • Monetary policy increases the (real) amount households have to lend to private sector • Thus supply curve of loans shifts out

Benefit of expansive policy • Increased investment stimulates the economy • The direct effect dominates as long as Fed policies do not also produce inflation that modifies nominal interest rates and balances

Limitations of expansive policy • New borrowing may stimulate a desire to invest beyond the capacity of the economy. • Increased demand for goods, with no room to increase output, leads to price increases. • Inflation, and the expectation of further inflation, results.

Expansive Monetary Policy • Increases output and lowers real interest rates if the economy is operating below capacity • Creates inflation if the economy is at capacity

Restrictive Monetary policy • Increases the real rate without inflation • Reduced money supply (bond sales) shifts supply to private sector to the left • Real interest rate increases • Desired borrowing decreases • Can move the economy more quickly out of the danger zone for inflation • Can choke the economy if applied when the economy is operating below capacity