Download

1 / 7

70 likes | 120 Vues

Explore interdependent demands of Poiuyts & Qwerts with price functions and optimal outputs, alongside a discussion on the concept of demand, product market analysis, and industry dynamics. Discover how price elasticity affects firms in competitive markets.

E N D

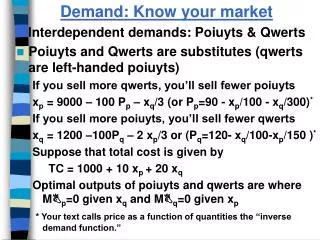

Demand: Know your market Interdependent demands: Poiuyts & Qwerts • Poiuyts and Qwerts are substitutes (qwerts are left-handed poiuyts) If you sell more qwerts, you’ll sell fewer poiuyts xp = 9000 – 100 Pp – xq/3 (or Pp=90 - xp/100 - xq/300)* If you sell more poiuyts, you’ll sell fewer qwerts xq = 1200 –100Pq – 2 xp/3 or (Pq=120- xq/100-xp/150 )* Suppose that total cost is given by TC = 1000 + 10 xp + 20 xq Optimal outputs of poiuyts and qwerts are where Mp=0 given xq and Mq=0 given xp * Your text calls price as a function of quantities the “inverse demand function.”

Poiuyts and Qwerts When we optimize using Solver, xp = 2000 Pp = 56.67 xq = 4000 Pq = 66.67 Notice, if we increase xp by +1 at this point, Pp declines by 1/100 and Pq declines by 1/150. Thus, MRp= 56.67(+1) - .01(2000) -.0067(4000) = 56.67 – 20.00 – 26.67 =56.67– 46.67 = 10.00 Since MCp= 10.00, Mp = 0 at the optimal solution.

Demand • When we speak of “demand” for a product, we think of a uniform product, a commodity. • When we dealt with demand for GM light trucks, we didn’t distinguish between Buick vans and Chevy pick-ups; we certainly didn’t distinguish between blue pick-ups and red pick-ups. We thought of a generic product, “light trucks.” • Even products we normally think of as “commodities” are subtly differentiated: Saudi oil has less(?) sulfur content than North Sea oil and accordingly sells for a different price. • We can get important insights into how the light truck market responds to rebates and how the oil market responds to business cycles without concerning ourselves with detailed product differentiation.

Demand Analysis: The Product and its Market • How you define the product and its market depends on the questions you want to ask. • If all you care about is sales of red Chevy pick-ups to women in Las Vegas in October … red Chevy pick-ups is your product … women in Las Vegas in October is your market • Even then, you’re abstracting from red Chevy pick-ups with different accessories and Las Vegas women of different marital status. • When you’re the analyst, • you get to define the product. • you get to define the geography, the demographics, and the time period of your analysis.

Demand: The Industry, The Firm Competitive Industry Firm With Industry FirmMarket Power Firm is Price TakerFirm is Price Maker Decides Quantity Decides Price-Quantity To Produce Combination P P P

Price Elasticity of Demand: Once More Price elasticity of demand = • Percent change in quantity dx/x • = = • Percent change in price dp/p • Linear DemandConstant x small high; x large low x = k P-a or xPa = k P P

Price Elasticity of Demand:Industry and FirmShort – Run and Long – Run Price elasticity of demand increases the more substitutes there are for a product • The products of the all the other firms in an industry are good substitutes for a particular firm’s product • Demand for the firm’s product is more elastic than demand for the industry’s product as a whole • Demand for a competitive firm’s product is infinite Price elasticity of demand increases the more time buyers have to adjust to price changes • Elasticity is greater in the long-run than in the short-run