Download

1 / 49

490 likes | 590 Vues

Explore the world of money, banks, and the Federal Reserve in this informative chapter. Learn about the functions of money, how banks create money, the role of the Federal Reserve System, and more.

E N D

26 MONEY, BANKS, AND THE FEDERAL RESERVE CHAPTER

Objectives • After studying this chapter, you will able to • Define money and describe its functions • Explain the economic functions of banks and other depository institutions and describe how they are regulated • Explain how banks create money • Describe the structure of the Federal Reserve System (the Fed), and the tools used by the Fed to conduct monetary policy • Explain what an open market operation is, how it works, and how it changes the quantity of money

Money makes the World Go Around • Money has taken many forms; what is money now? • What do banks do, and can they create money? • What is the Fed and what does it do? • How does the Fed ensure that the economy has the right amount of money to function properly?

What is Money? • Money is any commodity or token that is generally acceptable as a means of payment. • A means of payment is a method of settling a debt. • Money has three other functions: • Medium of exchange • Unit of account • Store of value

What is Money? • Medium of Exchange • A medium of exchange is an object that is generally accepted in exchange for goods and services. • In the absence of money, people would need to exchange goods and services directly, which is called barter. • Barter requires a double coincidence of wants, which is rare, so barter is costly. • Unit of Account • A unit of account is an agreed measure for stating the prices of goods and services.

What is Money? • Store of Value • As a store of value, money can be held for a time and later exchanged for goods and services. • Money in the United States Today • Money in the United States consists of • Currency • Deposits at banks and other depository institutions • Currency is the general term for bills and coins.

What is Money? • The two main official measures of money in the United States are M1 and M2. • M1 consists of currency outside banks, traveler’s checks, and checking deposits owned by individuals and businesses. • M2 consists of M1 plus time deposits, savings deposits, and money market mutual funds and other deposits.

What is Money? • Figure 26.1 illustrates the composition of these two measures in 2001 and shows the relative magnitudes of the components of money.

What is Money? • The items in M1 clearly meet the definition of money; the items in M2 do not do so quite so clearly but still are quite liquid. • Liquidity is the property of being instantly convertible into a means of payment with little loss of value. • Checkable deposits are money, but checks are not– checks are instructions to banks to transfer money. • Credit cards are not money. Credit cards enable the holder to obtain a loan quickly, but the loan must be repaid with money.

Depository Institutions • A depository institution is a firm that accepts deposits from households and firms and uses the deposits to make loans to other households and firms. • The deposits of three types of depository institution make up the nation’s money: • Commercial banks • Thrift institutions • Money market mutual funds

Depository Institutions • Commercial Banks • A commercial bank is a private firm that is licensed to receive deposits and make loans. • A commercial bank’s balance sheet summarizes its business and lists the bank’s assets, liabilities, and net worth. • The objective of a commercial bank is to maximize the net worth of its stockholders.

Depository Institutions • To achieve its objective, a bank makes risky loans at an interest rate higher than that paid on deposits. • But the banks must balance profit and prudence; loans generate profit, but depositors must be able to obtain their funds when they want them. • So banks divide their funds into two parts: reserves and loans. • Reserves are the cash in a bank’s vault and deposits at Federal Reserve Banks. • Bank lending takes the form of liquid assets, investment securities, and loans.

Depository Institutions • Thrift Institutions • The thrift institutions are • Savings and loan associations • Savings banks • Credit unions.

Depository Institutions • A savings and loan association (S&L) is a depository institution that accepts checking and savings deposits and that make personal, commercial, and home-purchase loans. • A savings bank is a depository institution owned by its depositors that accepts savings deposits and makes mainly mortgage loans. • A credit union is a depository institution owned by its depositors that accepts savings deposits and makes consumer loans.

Depository Institutions • Money Market Mutual Funds • A money market fund is a fund operated by a financial institution that sells shares in the fund and uses the proceeds to buy liquid assets such as U.S. Treasury bills.

Depository Institutions • The Economic Functions of Depository Institutions • Depository institutions make a profit from the spread between the interest rate they pay on their deposits and the interest rate they charge on their loans. • This spread exists because depository institutions • Create liquidity • Minimize the cost of obtaining funds • Minimize the cost of monitoring borrowers • Pool risk

Financial Regulation, Deregulation, and Innovation • Financial Regulation • Depository institutions face two types of regulations • Deposit insurance • Balance sheet rules

Financial Regulation, Deregulation, and Innovation • Deposits at banks, S&Ls, savings banks, and credit unions are insured by the Federal Deposit Insurance Corporation (FDIC). • This insurance guarantees deposits in amounts of up to $100,000 per depositor. • This guarantee gives depository institutions the incentive to make risky loans because the depositors believe their funds to be perfectly safe; because of this incentive balance sheet regulations have been established.

Financial Regulation, Deregulation, and Innovation • There are four main balance sheet rules • Capital requirements • Reserve requirements • Deposit rules • Lending rules

Financial Regulation, Deregulation, and Innovation • Deregulation in the 1980s and 1990s • During the 1980s many restrictions on depository institutions were lifted and distinctions between banks and others depository institutions ended. • In 1994 the Riegle-Neal Interstate Banking and Branching Efficiency Act was passed, which permits U.S. banks to establish branches in any state. • This change in the law led to a wave of bank mergers.

Financial Regulation, Deregulation, and Innovation • Financial Innovation • The 1980s and 1990s have been marked by financial innovation—the development of new financial products aimed at lowering the cost of making loans or at raising the return on lending. • Financial innovation occurred for three reasons • The economic environment--high inflation • Massive technological change • Avoid regulation

Financial Regulation, Deregulation, and Innovation • Deregulation, Innovation, and Money • The combination of deregulation and innovation has produced large changes in the composition of money, both M1 and M2.

How Banks Create Money • Reserves: Actual and Required • The fraction of a bank’s total deposits held as reserves is the reserve ratio. • The required reserve ratio is the fraction that banks are required, by regulation, to keep as reserves. Required reserves are the total amount of reserves that banks are required to keep. • Excess reserves equal actual reserves minus required reserves.

How Banks Create Money • Creating Deposits by Making Loans • To see how banks create deposits by making loans, suppose the required reserve ratio is 25 percent. • A new deposit of $100,000 is made. • The bank keeps $25,000 in reserve and lends $75,000. • This loan is credited to someone’s bank deposit. • The person spends the deposit and another bank now has $75,000 of extra deposits. • This bank keeps $18,750 on reserve and lends $56,250.

How Banks Create Money • The process continues and keeps repeating with smaller and smaller loans at each “round.” • Figure 26.2 illustrates the money creation process.

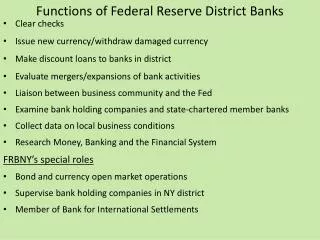

The Federal Reserve System • The Federal Reserve System, or the Fed, is the central bank of the United States. • A central bank is the public authority that regulates a nation’s depository institutions and controls the quantity of money.

The Federal Reserve System • The Fed’s Goals and Targets • The Fed conducts the nation’s monetary policy, which means that it adjusts the quantity of money in circulation. • The Fed’s goals are to keep inflation in check, maintain full employment, moderate the business cycle, and contribute toward achieving long-term growth. • In pursuit of its goals, the Fed pays close attention to interest rates and sets a target that is consistent with its goals for the federal funds rate, which is the interest rate that the banks charge each other on overnight loans of reserves.

The Federal Reserve System • The Structure of the Fed • The key elements in the structure of the Fed are • The Board of Governors • The regional Federal Reserve banks • The Federal Open Market Committee.

The Federal Reserve System • The Board of Governors has seven members appointed by the president of the United States and confirmed by the Senate. • Board terms are for 14 years and overlap so that one position becomes vacant every 2 years. • The president appoints one member to a (renewable) four-year term as chairman. • Each of the 12 Federal Reserve Regional Banks has a nine-person board of directors and a president.

The Federal Reserve System • Figure 26.3 shows the regions of the Federal Reserve System.

The Federal Reserve System • The Federal Open Market Committee (FOMC) is the main policy-making group in the Federal Reserve System. • It consists of the members of the Board of Governors, the president of the Federal Reserve Bank of New York, and the 11 presidents of other regional Federal Reserve banks of whom, on a rotating basis, 4 are voting members. • The FOMC meets every six weeks to formulate monetary policy.

The Federal Reserve System • Figure 26.4 summarizes the Fed’s structure and policy tools.

The Federal Reserve System • The Fed’s Power Center • In practice, the chairman of the Board of Governors (since 1987 Alan Greenspan) is the center of power in the Fed. • He controls the agenda of the Board, has better contact with the Fed’s staff, and is the Fed’s spokesperson and point of contact with the federal government and with foreign central banks and governments.

The Federal Reserve System • The Fed’s Policy Tools • The Fed uses three monetary policy tools • Required reserve ratios • The discount rate • Open market operations

The Federal Reserve System • The Fed sets required reserve ratios, which are the minimum percentages of deposits that depository institutions must hold as reserves. • The Fed does not change these ratios very often. • The discount rate is the interest rate at which the Fed stands ready to lend reserves to depository institutions. • An open market operation is the purchase or sale of government securities—U.S. Treasury bills and bonds—by the Federal Reserve System in the open market.

The Federal Reserve System • The Fed’s Balance Sheet • On the Fed’s balance sheet, the largest and most important asset is U.S. government securities. • The most important liabilities are Federal Reserve notes in circulation and banks’ deposits. • The sum of Federal Reserve notes, coins, and banks’ deposits at the Fed is the monetary base.

Controlling the Quantity of Money • How Required Reserve Ratios Work • An increase in the required reserve ratio boosts the reserves that banks must hold, decreases their lending, and decreases the quantity of money. • How the Discount Rate Works • An increase in the discount rate raises the cost of borrowing reserves from the Fed, decreases banks’ reserves, which decreases their lending and decreases the quantity of money.

Controlling the Quantity of Money • How an Open Market Operation Works • When the Fed conducts an open market operation by buying a government security, it increases banks’ reserves. • Banks loan the excess reserves. • By making loans, they create money. • The reverse occurs when the Fed sells a government security.

Controlling the Quantity of Money • Although the details differ, the ultimate process of how an open market operation changes the money supply is the same regardless of whether the Fed conducts its transactions with a commercial bank or a member of the public. • An open market operation that increases banks’ reserves also increases the monetary base.

Controlling theQuantity of Money • Figure 26.5 illustrates both types of open market operation.

Controlling the Quantity of Money • Bank Reserves, the Monetary Base, and the Money Multiplier • The money multiplier is the amount by which a change in the monetary base is multiplied to calculate the final change in the money supply. • An increase in currency held outside the banks is called a currency drain. • Such a drain reduces the amount of banks’ reserves, thereby decreasing the amount that banks can loan and reducing the money multiplier.

Controlling the Quantity of Money • The money multiplier differs from the deposit multiplier. • The deposit multiplier shows how much a change in reserves affects deposits. • The money multiplier shows how much a change in the monetary base affects the money supply.

Controlling the Quantity of Money • The Multiplier Effect of an Open Market Operation • When the Fed conducts an open market operation, the ultimate change in the money supply is larger than the initiating open market operation. • Banks use excess reserves from the open market operation to make loans so that the banks where the loans are deposited acquire excess reserves which they, in turn, then loan.

Controlling the Quantity of Money • Figure 26.6 illustrates a round in the multiplier process following an open market operation.

Controlling the Quantity of Money • Figure 26.7 illustrates the multiplier effect of an open market operation.

Controlling the Quantity of Money • The Size of the Multiplier • To calculate the size of the money multiplier, first define: • R = reserves • C = currency in circulation • D = deposits • M = quantity of money • B = monetary base • c = ratio of currency to deposits • r = required reserve ratio

Controlling the Quantity of Money • The quantity of money, M, is: • M = C + D = (1+ c) D • The monetary base, B, is: • B = R + C = (r + c) D • Divide the first equation above by the second one to get: • M/B = (1+ c)/(r + c) • or • M = [(1+ c)/(c + r)] B

Controlling the Quantity of Money • The money multiplier is [(1+ c)/(c + r)]—the amount by which a change in B is multiplied to determine the resulting change in M. • With c = 0.5 and r = 0.1, the money multiplier is • 1.5/0.6 = 2.5.