Download

1 / 58

580 likes | 751 Vues

Tomorrow’s Electric Industry -- Challenges and Opportunities. David K. Owens Executive Vice President Edison Electric Institute 2009 NCEA CEO & Executive Workshop Green Bay, Wisconsin December 7, 2009. America’s Challenges. Resolve financial crisis

E N D

Tomorrow’s Electric Industry -- Challenges and Opportunities David K. Owens Executive Vice President Edison Electric Institute 2009 NCEA CEO & Executive Workshop Green Bay, Wisconsin December 7, 2009

America’s Challenges • Resolve financial crisis • Stimulate economy and get America back to work • Health Care • Address Climate Change • Transform our society to be greener and more efficient

Overview • Recession has dampened demand, but forecasted to rebound and grow • Commodity, equipment, and labor costs are down, making it an ideal time to build and prepare for future demand increases • Wall Street Restructuring affects access to capital markets and increasing cost of capital • As one of the most capital-intensive industries, reduced access to capital markets at higher costs, means that enhanced liquidity and financial flexibility is important • Utility industry at the beginning of a major investment cycle • Driven by new technology, demand growth, efficiency and environmental CAPEX • Addressing climate change and new priorities will be costly

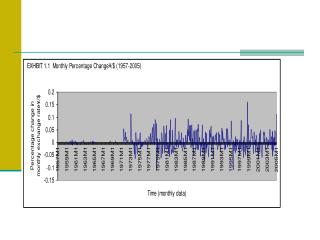

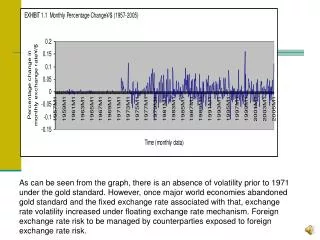

Long-term Decline in Credit Quality:1992 vs. Today 4/16/1992 9/30/2009

Industry Capital Expenditures are Growing • Industry committed to reliability - making needed investments in generation, transmission, smart grid/ distribution & the environment • Financial crisis initially brought sharp revisions for 2009 • Multi-year trend of soaring construction /materials costs reversed since mid-2008 • Increased spending expected to continue into the future • Total CAPEX for 2010-2030 ~ $1.5 trillion* • Excludes impact from climate legislation U.S. Shareholder-Owned Electric Utilities * The Brattle Group, preliminary findings from The Edison Foundation presentation titled Transforming America’s Power Industry. Represents the entire Power sector.

Industry Faces Difficult Decisions To Invest or Not to Invest? Defer or cancel infrastructure projects to enhance current liquidity position Electric reliability could be impacted when economy and demand rebound Opportunities with sharply declining commodity and input costs Higher financing costs Uncertainty ?

Climate Change QuestionsWe Must Answer! • How do you minimize the impact of compliance costs on low-income consumers? • What must U.S. climate change legislation and carbon management strategy include to • Ensure economic growth? • Ensure energy security? • Avoid unfairness?

President Obama’s Energy / Environmental Views Renewable Portfolio Standards Climate Change 25% by 2025 80% reduction by 2050 H.R. 2454 20% by 2020 S.1462 15% by 2021 H.R. 2454 & S.1733 83% reduction by 2050 Smart Grid EnergyEfficiency Overhaul of Federal Efficiency Codes Increased Government Support In H.R. 2454, S.1462 and stimulus package In H.R. 2454 & S.1462

Key Climate Provisions • Economy Wide? • Cap-and-Trade or Tax? • Mitigating Customer Impacts? • Allowances • Offsets • Strategic allowance reserve • Other approaches – Price Collar • Targets and Timetables?

Targets and TimetablesLeading Congressional Proposals H.R. 2454 S.1733 U.S. CAP proposal • 3 % below 2005 by 2012 • 17 % below 2005 by 2020 • 42 % below 2005 by 2030 • 83 % below 2005 by 2050 • 3% below 2005 by 2012 • 20% below 2005 by 2010 • 42% below 2005 by 2030 • 83% below 2005 by 2050 • 3 % below to 2 % above 2005 by 2012 • 14-20 % below 2005 by 2020 • 42 % below 2005 by 2030 • 80 % below 2005 by 2050

Targets and TimetablesQuestions / Concerns • To meet short-term targets • Power sector will rely on energy efficiency, renewables and natural gas • In the medium term (i.e., 2020-2025) • Targets should be harmonized with the development and commercial deployment of advanced climate technologies and measures • (e.g., nuclear energy, advanced coal technologies with carbon capture and storage, PHEVs, smart grid)

The American Clean Energy and Security Act of 2009 (H.R. 2454) Economic Impact Projections

Discount Rate Future Growth of Nuclear Power Timing of Commercially Available CCS Availability of Renewable Energy Sources Reduced Electricity Use Due to Price Response and Energy Efficiency Use of Offsets Principal Drivers of Cost Results

How Will Emissions Reductions be Achieved?Assumptions on Nuclear, Renewables, Energy Efficiency Vary

Cost Containment Measures Allocation of Allowances Price Collar Offsets

Allocation of AllowancesPrimary Goals • Help mitigate the impact of increased energy prices on consumers • Assist in transition to clean energy economy • Advance development and deployment of clean energy technologies, including energy efficiency

Allowances Under Kerry-Boxer Bill (S.1733) Clean Energy Jobs and American Power Act S.1733: • 15.75% of allowances are used for deficit reduction (10% through 2029) and other uses • Number of allowances to electricity sector reduced • Contains the same allocation distribution as H.R. 2454 • Total number of allowances for 2012-2016 are the same under H.R. 2454 less for 2017-2030 • Auctions 25% of the allowances (15% in H.R. 2454). Source of these additional allowances is unclear • Establishes a minimum auction price of $10 in 2012, escalating at 5% per year plus inflation • Contains a so-called “soft” price collar

How a Price Collar Could Work Allowance Price

How a Price Collar Could Work • Price ceiling – EPA sells allowances to regulated firms, for compliance only, at price cap. Rules needed to prevent gaming • Possible Sources of these allowances: • Strategic Reserve • Borrowing from the Future • Borrowing from Offsets

How is the Reserve Replenished? • When allowance prices fall below the price floor (green area), EPA stops selling allowances and the Unsold allowances are added to the Reserve • The revenues from sales of “additional” (whether from reserve or borrowed, etc. ) allowances at the capped price (red area), are used when prices decline (yellow area) to purchase offsets. Each purchased offset enables an allowance to be restored to the Reserve/ future, etc.

Mitigating Customer ImpactsOffsets • Allows use of up to 2 billion tons annually of offsets • Up to 1 billion from domestic sources • With waiver (insufficient domestic offsets at market price of allowances) , up to 1.5 billion from international sources • Recognizes three types of offsets • Domestic (exchanged at 1:1 basis) • International • Term offsets (only valid for five years) • Concerns • Questions about supply and ability to fully utilize cap • Domestic offsets mainly from ag. forestry projects (<1/2 billion tons)? • International offsets largely dependent on successor to Kyoto Protocol • EPA has discretion whether to issue any international offset credits

What Will It Take to Address Climate Change? • Renewables • Energy efficiency • Clean coal technologies • Carbon capture and storage • Nuclear • Plug-in hybrid electric vehicles (Smart grid) There is no silver bullet! We need it all … but it will be costly!

Renewable / Energy Efficiency QuestionsWe Must Answer! • Renewable Technology • How much can increased renewable capacity contribute going forward? • How do we get transmission constructed for renewables? • Energy Efficiency • How significant of a role can energy efficiency play in the future? • How can customers benefit and actively participate in energy efficiency programs from the residential and commercial perspectives?

State Renewable Energy Portfolio Standards • 31 states with quota obligations – RPS • Each state has different natural resource endowment, different industrial and socio-economic characteristics… • …So each state RPS has: • Different targets • Different timelines • Different eligible resources • Different compliance entities • Different compliance mechanisms • Different enforcement and penalties

Federal PoliciesA Federal ERES? • H.R. 2454 – 20% by 2020 The American Clean Energy and Security Act of 2009 • S.1462 – 15% by 2021 The American Clean Energy Leadership Act of 2009 • Contingent on climate (HR 2454 / S.1733)

Planned Capacity Additions Reflect State RPS Requirements Non-Hydro Renewable Nuclear Nuclear 4% 10% Hydro 13% 9% Non-Hydro Renewable 34% Coal Coal 14% 30% Gas Oil 41% 0% Hydro Gas Oil 16% 6% 23% US Generation Capacity in 2008 (1,061 GW in Service) Planned Capacity Additions to 2020 (352 GW) Non-hydro renewables make up 4% of US capacity today but 34% of planned capacity additions through 2020. Source; Ventyx Global Energy and Bernstein Analysis

Biggest Challenge for Renewables … Transmission • Planning • Siting • Cost Allocation Renewables are Variable Resources!

Integrating RenewablesOperational Challenges • Higher RPS levels can create significant surplus energy • Has created excess energy at night • Requires more system backup to maintain reliability • Quick start and fast ramping technologies (peaking / storage) to manage generation variability and maintain reliability when wind falls off or clouds appear • Smart grid can help mitigate some of these problems • Energy storage / off-peak electric vehicle charging can mitigate problem • Smart grid will help enable these new technologies

Demand Projected To Increase 40% 21% by 2030 Recession Impact? Billon kiloWatthours Sources: U.S. Department of Energy, Energy Information Administration

The Energy Efficiency Challenge • Average US household owns 24 consumer electronic products • 2 DVRs use as much energy in 1 year as a refrigerator • Play Station and X-Box use more electricity than a PC • PCs and TVs now account for 10% of a home’s electricity usage • 99% of these products must be plugged in or recharged • 42” Plasma TV uses more than twice as much as a standard 27” TV • More efficient use of energy could significantly reduce energy bills • Need to educate all consumers about how to save energy and use it more efficiently

Aggressive campaign for technologies Smart buildings Smart appliances Smart electric meters and grid Smart rates Use of “smart technologies” and new rate designs can: Allow consumers to control their energy usage to save money Avoid wasting energy Control how and when appliances do their jobs Help utilities efficiently operate their systems and maintain reliability Help keep supply and demand in balance Support more efficient use of generating resources Commercializing plug-in hybrid electric vehicles Intensified National Commitment To Energy Efficiency Is Needed

Energy Efficiency - Our 1st fuelAve. Cost ~$0.035 / kWh Saved Total Utility EE Costs per kWh Saved $0.050 $0.045 $0.040 $0.035 $0.030 $/kWh $0.025 $0.020 $0.015 $0.010 $0.005 $0.000 2000 2001 2002 2003 2004 2005 2006 2007 Source: The Edison Foundation – Institute of Electric Efficiency; EIA Form 861

Energy Efficiency Business Model Components Program Cost Recovery Lost Margin Recovery Performance Incentives

Carbon Capture and Storage Challenges • Capture • Develop cost-effective means of capturing CO2 from combustion • Transport • Ability to access current gas and CO2 pipeline structure • Regulatory framework • Liability concerns • Storage • Permitting and siting • Liability concerns • Full-scale demonstration projects • Public education and acceptance

New Coal GenerationCarbon Capture and Storage (CCS) in (H.R. 2454) • “National strategy” for a CCS regulatory framework • Federal agencies to develop a (sec. 111) • Geologic storage and propose regulations • EPA to finalize regulations for under the Clean Air Act (sec. 112) • Study of legal framework for geologic storage sites • Establish task force (sec. 113) • New Carbon Storage Research Corporation • Funded by charge on deliveries of fossil fuel electricity • Fund commercial-scale (>250MW), integrated demo projects (sec. 114) • $10 billion over 10 years; 50% of funds reserved for utility projects • Corporation is an affiliate of EPRI and not an agent of the U.S. government

U.S. Electricity Sources Which Do Not Emit Greenhouse Gases During Operation 2008 Source: Energy Information Administration Updated: 4/09

Expectations for the Future 2014 2012 2018 2020 2016 2010 Initial wave has 4 - 8 plants on line by 2015-2016 Suppliers ramp up component manufacturing capability Second wave begins construction when it is clear that first wave can be licensed and built on time and within budget Second wave begins COL preparation Source: NEI

U.S. Shale – A Game Changer?Gas Production Potential Forecast Historical BCFD Source: Tristone Capital, Devon Energy

SMART GRID A Game Changing Technology

What is the Smart Grid? An advanced, telecommunication / electric grid with sensors and smart devices linking all aspects of the grid, from generator to consumer, and delivering enhanced operational capabilities that : • Provide CONSUMERS with the information and tools necessary to be responsive to electricity grid conditions (including price and reliability) through the use of electric devices and new services (from smart thermostats to PHEV) • Ensure EFFICENTuse of the electric grid (optimizing current assets while integrating emerging technologies such as renewables and storage devices) • Enhance RELIABILITY (protecting the grid from cyber and natural attacks, increasing power quality and promoting early detection and self correcting grid “self-healing”)

EEI Members’ Stimulus Awards • EEI Members have won approximately $2.8 billion in funding under the Recovery Act, including: • $2.4 billion in Smart Grid Investment Grants • $287 million in Smart Grid Demonstration and Storage funding • $14 million for solar energy deployment and integration • $4 million to expand the use of alternative fueled vehicles • $3.6 million in synchrophasor research

Smart Grid Technologies • The Smart Grid is all about technologies that will transform the industry by enabling: • New businesses • New market participants • New customer relationships • Customer control • Enhanced reliability • Electric Utilities will lead the transformation.

Smart Grid Benefits • Installed smart devices can do multiple tasks • Aggregate demand response to reduce wholesale market peaks and prices • Provide consumers with information and tools to optimize energy usage • Relieve congestion at transmission and distribution level • Avoid or defer G, T & D infrastructure investments • Optimize use of existing resources • Coordinate integration of new renewables and storage devices • Improve customer, distribution and grid reliability Utilities are uniquely positioned to optimize the new smart grid and maximize the benefits from smart grid investments