The Evolution of Wealth Management

250 likes | 486 Vues

The Evolution of Wealth Management. Garth Gibbes & Carl Brillinger April 29, 2014. What is your current market for your Products & Services?. Who is your client? Why do they do business with you? What needs they have that you serve? What do you provide them that is unique?

The Evolution of Wealth Management

E N D

Presentation Transcript

The Evolution of Wealth Management Garth Gibbes & Carl Brillinger April 29, 2014

What is your current market for your Products & Services? • Who is your client? • Why do they do business with you? • What needs they have that you serve? • What do you provide them that is unique? • How do you differentiate yourself?

What is Wealth Management? • Why does someone buy or own mutual funds and stocks? • What is the purpose of an investment? • Why does a client care about superior investment returns? • What role does ‘money’ play in a client’s life? • How important is “trust”?

Wealth Management: a working definition • An integrated approach to a client’s financial planning needs • Focuses on client before product sales • Combines advisory services with product placement • Geared to a client’s life stage needs

How did Wealth Management evolve • Pre-1980, Financial Planning focused on affluent clients • Effect of the baby boom • Crumbling of “four pillars” • Growth of product suppliers and products • Explosion in number of investment advisors • Changing client needs as they move through their life cycle

The key industry players in Wealth Management • Clients • Manufacturers • Regulators • Distributors (advisors) • Educators

The Evolution of Wealth Management 1. The industry prior to 1980 Investment Advisors Insurance Agents Chartered Banks Trust and Estate Family protection Young families Business protection Annuities, retirement plans Custodial services Transfer agents Trustee role Tax planning Estate structure Affluent clients Stocks and bonds “hot tips” Investment selection Personal banking Deposit services Guaranteed products

The arrival of Wealth Management • Within the last decade, services increased as stock market bubble burst and corporate scandals surfaced • Clients demanded trusted source of advice • Advisors are becoming better educated • Baby boomers and parents required help securing their retirements and transferring wealth to children • High net worth clients and families now have access to more skilled professionals • Wealth management firms now compete on trust and reputation and recognize the importance of fiduciary duties

The industry response to aging clients • More emphasis on lifestyle issues and the role money plays • The emergence of the “key” advisor or “Chief Financial Officer” • The explosion in products and approaches to meet client needs • Mass-marketing of products and services • Increased focus on client education

The evolution of the distribution industry • Pre-1980 investment advice was commission based • Insurance and mutual funds based on distribution model • Legal and regulatory restraints on advisor activity • Deregulation occurred in U.S. in 1975 and Canada in 1992 • Crumbling of the “four pillars” came as a result of deregulation • Distribution through financial advice became the norm • Canadian chartered banks play a major role in distribution and industry change • Wealth management approach became effective way for distributors to create cross-selling opportunities

Types of distribution companies • “Full-Service” investment advisors • “Mutual fund” financial planners • Insurance financial planners • “Fee-based” planners • Referral financial planners

Wealth Management and Advisors • Advisors are adjusting to their aging clientele • Advisors moved from specialists to generalists • Advisors are marketing themselves as comprehensive planners • Advisors hold multiple licenses (insurance, investment management, commodities, futures, etc.,) • Advisors are using the Wealth Management Approach as a way to differentiate themselves and provide more relevant information and advice.

Delivery of Wealth Management Advice • Commission: advisors take a percentage of value transaction • Fee-base: advisors charge a set fee for their advice based on asset size • Fee-for-service: advisors charge by the hour or the plan • Fees plus commissions: advisors receive commissions from manufacturers (trail commissions or service fees); may also charge fees for plans

Who is providing Wealth Management Advice • Full-service investment advisors • Licensed financial planners • Mutual fund sales people • Insurance agents • CA’s, CMA’s, CGA’s and accountants • Do-it-yourself (internet, media, on-line investing etc., • Commercial Banking people

What types of advisors practice wealth management • Established advisors: have a mature book of business and long-term relationships with clients • New advisors: desire to market a different approach to client relationships • Women advisors: taking a more holistic approach to wealth management • New immigrant advisors: Understanding the specific cultural needs

Clients who receive wealth management • High net worth clients: clients who seek a “key trusted advisor” who can advise on all areas of their financial life • Business owners: clients who are transitioning out of their business and into retirement • Investment buyers: clients who incorporate their investments into a bigger financial plan • Senior executives: clients who are looking at an integrated approach to their financial plan and an advisor who can save them time • Women clients: clients who take a more “family” view of financial planning and investing

The role of the wealth advisor • To understand the client’s views of money and to match financial solutions to client needs • To educate client on issues they may not be aware of • To “coach” client to set and attain financial goals • To act as a “personal Chief Financial Officer”

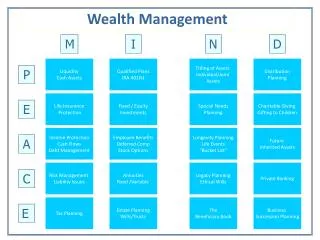

The Personal Chief Financial Officer WealthAdvisor Investment Management Insurance Needs Tax Issues Business/ Credit Issues Estate Planning

Wealth Planning (from An Advisor’s Point Of View ) Investment Management Tax Planning Estate Planning Income/Cash Management Charitable Giving

Four client financial life stages • Accumulation phase: Family and career building • Preservation phase: Planning for retirement and life after work • Converting wealth to income: Utilizing assets to finance lifestyle • Transfer of wealth: Passing on assets before and after death

How to become the best wealth advisor • Focus on your client’s overall financial needs • Become a trusted advisor by not being a “product pusher” • Improve your listening skills • Want to be in your business for the long-term • Understand the changing industry • Invest in your wealth management education • GOODLUCK!