Download

1 / 13

130 likes | 382 Vues

11. Chapter. S Corporations. In General. For federal income tax purposes, S Corporations are tax-reporting entities but not tax-paying entities, often referred to as flow-through entities. S Corporations. Election of S Corporation Status. Eligibility for Subchapter S Status.

E N D

11 Chapter S Corporations

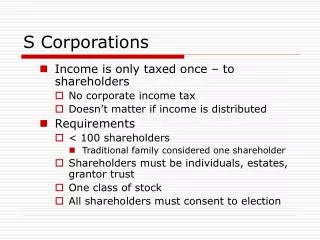

In General • For federal income tax purposes, S Corporations are tax-reporting entities but not tax-paying entities, often referred to as flow-through entities

S Corporations Election of S Corporation Status

Eligibility for Subchapter S Status • [IRC §1361(b)(1)] Eligibility requirements: • Domestic corporation • Not an “ineligible” corporation • Limited number of shareholders • Shareholders may only be individuals, estates and certain types of trusts • Shareholders may not be nonresident aliens • Can have only one class of stock

Eligibility for Subchapter S Status • [IRC §1361(b)(1) & (c)] Limit on number of shareholders: • Post-AJCA 2004 (effective 1/1/2005) • Limited to 100 shareholders • Families can elect to have all “family members” treated as one shareholder

Eligibility for Subchapter S Status • [IRC §1361(b)(1)(D] Only one class of stock outstanding: • Differences in voting rights only are disregarded [IRC §1361(c)(4)] • Must confer identical distribution and liquidation rights [Reg. §1.1361-1(l)]

Electing Subchapter S Status • [IRC §1362(a)] All shareholders must consent to an S corporation election • [IRC §1362(b)] The election must be made during the preceding tax year or by the 15th day of the 3rd month of the current tax year • [IRC §1362(c)] The election is effective for the taxable year for which it is made and all subsequent years until the election is terminated

LIFO Recapture Tax • [IRC §1363(d)] For C corporations using the LIFO inventory method, the entire LIFO recapture amount must be included in taxable income in the last taxable year before the S corporation election is effective • LIFO recapture equals the difference between the inventory basis using LIFO versus FIFO

S Corporations Termination of S Corporation Status

Termination of Subchapter S Status • [IRC §1362(d)(1)] Termination by revocation: • Shareholders owning more than 50% of the shares outstanding must consent to the revocation • Revocation must be made by the 15th day of the 3rd month of the taxable year to be effective for that year (otherwise effective for the next taxable year)

Termination of Subchapter S Status • Other termination • Automatically revoked if corporation fails to qualify for S corporation status [IRC §1362(d)(2)] • Automatically revoked if passive investment income > 25% of gross receipts for three consecutive years and the corporation has accumulated earnings and profits (E&P) [IRC §1362(d)(3)(A)]

Termination of Subchapter S Status • [IRC §1362(e)(1)] If an election is terminated other than by revocation, the corporation has two short tax years (one as an S corporation and one as a C corporation) • Tax for the C corporation short tax year must be annualized [IRC §1362 (e)(5)]

Termination of Subchapter S Status • [IRC §1362 (f)] IRS may allow shareholders to “fix” terminations that were inadvertent • [IRC §1362(g)] Otherwise, a corporation cannot elect S corporation status again for at least five years after an S election is terminated