Download

1 / 19

190 likes | 502 Vues

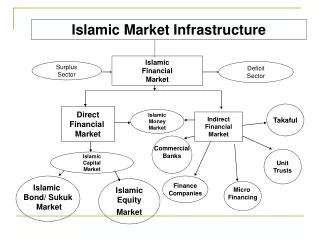

The Financial Market. The term ‘Financial Markets’ refers to all those organisations and institutions which lend funds to business enterprises and government/public authorities. FINANCIAL MARKETS. MONEY MARKET Short-term funds Organised and unorganised. CAPITAL MARKET

E N D

The Financial Market • The term ‘Financial Markets’ refers to all those organisations and institutions which lend funds to business enterprises and government/public authorities. FINANCIAL MARKETS MONEY MARKET Short-term funds Organised and unorganised CAPITAL MARKET Medium and long-term funds

Money Market • Money market refers to an mechanism whereby borrowers manage to obtain short-term funds on one hand. And on the others, lenders succeed in getting credit worthy borrowers for their money. • In any money market, the Central Bank occupies a strategic position being the residual source of supply of funds, followed by commercial banks as the most important lenders. • However, these banks are not only lenders of money, but they also create credit. The Central Bank’s role is therefore important as controller of credit.

Functions of Money Markets • By providing various kinds of attractive and suitable credit instruments, it increases the supply of funds. • Money Market avoids, gluts or shortages in funds arising out of seasonal variations in the flow and demand for funds. • It enhances the amount of liquidity in the economy. • It makes available funds at cheaper rates. • It reduces regional gluts and stringencies in funds through quick transfer of funds from one place to another. • By providing profitable investment opportunities for short-term surplus funds, it helps to enhance profitability of individuals and financial institutions.

The Organised Indian Money Market • The Indian money market comprises two sectors: organised and unorganised segments. • In the organised segment of the money market, the RBI occupies a pivotal position, followed by commercial banks, including public sector banks and joint stock banks, Indian and foreign. • The structure of money market has undergone huge changes, particularly since economic reforms. • The RBI has gradually developed money market through five-pronged approach.

Indian Money Market: Changing Structure • Ceilings on interest rate of various money market instruments were withdrawn since 1989. • Several new money market instruments introduced, viz auctions of Treasury Bills, Commercial Papers, RBI repos. • Permitting increasing number of players: starting with Discount and Finance House of India (DFHI)

Money Market Instruments • Call money market: These are money dealt for 1 to 14 days. Inter-bank lending/call money market is the major component of this market. • Treasury Bills Market: Treasury Bills are short-term liability of the government. The market for these include, 14-day Auction TBs, 182-days, (1999), 364-days (not re-discountable with RBI). • Repos: This is a money market instrument which enables collateralised short-term borrowing and lending through sale and purchase in debt instruments. Under a repo transactions, holder of a security can sell it to an investor with an agreement to purchase them at pre-determined rate and date.

Money Market Instruments providing liquidity to the commercial sector. • Commercial Bills: Bill issued between merchant firms, between seller and buyer of goods. The purpose is to reimburse the seller while the buyer delays payments. • Commercial Papers (CP): This is a short-term instrument of raising funds by corporates. It is essentially a sort of unsecured promissory note sold by the issuer to a banker. Following the recommendations of the Vaghul Committee, CP was introduced in 1990, can be issued by listed companies which have working capital of not less that 5 crores. These companies have to be rated by rating agencies approved by RBI, has to obtain P2 from CRISIL or A2 from ICRA. • MMFs: Introduced in 1992, for providing additional short-term avenue for individual investor.

The Unorganised Segment of Indian Money Market • Money lenders, indigenous bankers, • Unregulated loan companies, chit funds, nidhis.

The Capital Market • Capital Market can be divided into two constituents: • 1) The Securities market • 2) the Financial Institutions; IFCI, IDBI, LIC, UTI etc. The Securities market Corporate Securities Market Government Securities Market

Importance/Role of Capital Market • Pace of development, is conditioned, among other things, by the rate of long-term investment and capital formation. That in turn, is conditioned by mobilisation, channelisation and augmentation of funds. • With rise of joint stock companies, capital market becomes a necessary infrastructure for fast-paced industrialisation, hence promotes industrial growth. • Raising long-term capital • Ready and continuous market

The Government Securities market • Gilt-edged Market: Market in government securities or securities guaranteed by the government. Imp features are: • Risk free and returns are guaranteed • RBI the sole dealer of these securities • Investors in these securities are predominantly institutions which are required to hold government securities like comm. Bnks, LIC, UTI, etc.

Financial Institutions in the Indian Economy • Institutions that allow savers and borrowers to interact are called financial intermediaries. • Types of Financial Intermediaries: • Banks - Bond Market • Stock Market - Mutual Funds • Other

Financial Intermediaries: Banks • Banks take in deposits from people who want to save and make loans to people who want to borrow. • Banks pay depositors interest and charge borrowers higher interest on their loans. • Banks help create a medium of exchange, by allowing people to write cheques against their deposits.

Financial Intermediaries: The Bond Market • A bond is a certificate of indebtedness that specifies obligations of the borrower to the holder of the bond. • Characteristics of a bond: • Term: the length of time until maturity. • Credit Risk: the probability that the borrower will fail to pay some of the interest or principle.

Financial Intermediaries: The Stock Market • Stock represents ownership in a firm, thus the owner has claim to the profits that the firm makes. • Sale of stock infers “equity finance” but offers both higher risk and potentially higher return. • Primary Market: new issues market • Secondary Market: stock market • Markets in which stock is traded: • National Stock Exchange • Bombay Stock Exchange

Financial Intermediaries: Mutual Funds • AMutual Fundis an institution that sells shares to the public and uses the proceeds to buy a selection, or portfolio, of various types of stocks, bonds, or both. • Allows people with small amounts of money to diversify.

Financial Intermediaries: Other • Other financial intermediaries in the money market: • Money lenders, indigenous bankers, • Unregulated loan companies, chit funds, nidhis. • Pension Funds • Insurance Companies