Download

1 / 23

230 likes | 252 Vues

Learn the essential steps for making informed decisions in engineering economy, including problem definition, objective setting, alternative identification, consequences evaluation, selection, implementation, and auditing.

E N D

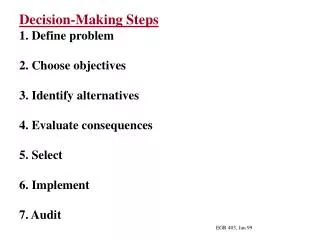

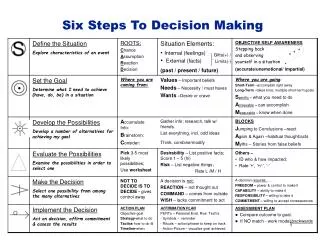

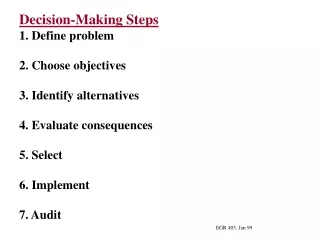

Decision-Making Steps 1. Define problem 2. Choose objectives 3. Identify alternatives 4. Evaluate consequences 5. Select 6. Implement 7. Audit EGR 403, Jan 99

Engineering Economy uses mathematical formulas to account for the time value of money and to balance current and future revenues and costs. Cash flow diagrams depict the timing and amount of expenses (negative, downward) and revenues (positive, upward) for engineering projects. EGR 403, Jan 99

Example on Cash Flow Diagram Draw the cash flow diagram for a Corolla with the following cash flow: Down payment $1000, refundable security deposit $ 225, and first month’s payment $189 which is due at signing (total $1414). Monthly payment $ 189 for 36 month lease (total $ 6804). Lease-end purchase option $ 7382. EGR 403, Jan 99

Interest is the return on capital or cost of using capital. Simple Vs Compound interest rate Equivalence(page 45) When we are indifferent as to whether we have a quantity of money now or the assurance of some other sum of money in the future, or series of future sums of money, we say that the present sum of money is equivalent to the future sum or series of future sums. Equivalence depends on interest rate EGR 403, Jan 99

Notation: i = Interest rate per payment period n = Number of payment periods P = Present value of a sum of money (time 0) Fn = Future value of a sum of money in year n (end of year n) Considering Compound interest Single Payment Compound Amount: (F|P,i,n) = (1+i)n = F/P, thus F = P(F|P, i, n) Single Payment Present Worth: (P|F,i,n) = 1/(1+i)n, thus P = F(P|F, i, n) EGR 403, Jan 99

Example on P and F 1- An antique piece is purchased for $10,000 today. How much will it be worth in three years if its value increases 8% per year? 2- What sum can you borrow now, at an 8% interest rate, if you can pay back $6,000 in five years? 3- How long will it take for an investment of $300 to double considering 8% interest rate? 4- An investment of $2,000 has been cashed in as $3,436 eight years later. What was the interest rate? 5- How much will a deposit of $400 in a bank be six years from now, if the interest rate is 12% compounded quarterly?

Different Methods for Solving Engineering Economy Problems: 1- Mathematical formulas (use calculator) 2- Engineering Economy functional notation (use compound interest tables) 3- Software such as Excel (use defined functions) EGR 403, Jan 00

In most Eng. Econ. Formula, there are four parameters , i.e. F, P, i, and n. If three of these are known you can find the fourth one. Specific Situations: * The required number of years is not in the compound interest table * There is no compound interest table for the required interest rate * The interest is compounded for some period other than annually EGR 403, Jan 00

Different Skills (Tricks) to Solve Cash Flow Diagram • Shift origin (time 0) to an imaginary point of time • Add and subtract imaginary cash flows • Dissect cash flow diagram EGR 403, Jan 04

Notation: A = A series of n uniform payments at the end-of-period Considering Compound interest Uniform series compound amount: F = A(F|A, i, n) Uniform series sinking fund: A = F(A|F, i, n) Uniform series capital recovery: A = P(A|P, i, n) Uniform series present worth: P = A(P|A, i, n) Deferred annuities: EGR 403, Jan 99

Example on A 1- You make 12 equal annual deposits of $2,000 each into a bank account paying 4% interest per year. The first deposit will be made one year from today. How much money can be withdrawn from this bank account immediately after the 12th deposit? 2- Your parents deposit $7,000 in a bank account for your education now. The account earns 6% interest per year. They plan to withdraw equal amounts at the end of each year for five years, starting one year from now. How much money would you receive at the end of each one of the five years? 3- How much should you invest today in order to provide an annuity of $6,000 per year for seven years, with the first payment occurring exactly four years from now? Assume 8% interest rate.

Notation: G = Arithmetic gradient series, fix amount increment at the end-of-period Considering Compound interest Arithmetic gradient uniform series: A = G(A|G, i, n) Arithmetic gradient present worth: P = G(P|G, i, n) G 2G 0 1 2 3 EGR 403, Jan 99

Notation: g = Geometric gradient series, fix % increment at the end-of-period Considering Compound interest A’ A’(1+g) A’(1+g)2 0 1 2 3 EGR 403, Jan 99

Example on G and g 1- Suppose that certain end-of-year cash flows are expected to be $2,000 for the second year, $4,000 for the third year, and $6,000 for the fourth year. What is the equivalent present worth if the interest rate is 8%? What is the equivalent uniform annual amount over four years? 2- Overhead costs of a firm are expected to be $200,000 in the first year, and then increasing by 4% each year thereafter, over a 6-year period. Find the equivalent present value of these cash flows assuming 8% interest rate.

Types of Interest Rates: r = Nominal interestrate per period (compounded as sub period) = m*i i = Effective interest rate per sub period (i.e., month) ia = Effective interest rate per year (annum) m = Number of compounding sub periods per period Super period = Cash flow less often than compounding period Sub period = Cash flow more often than compounding period Continuous Compounding: EGR 403, Jan 99

Example on Different Interest Rates 1- A credit card company charges an interest rate of 1.5% per month on the unpaid balance of all accounts. What is the nominal rate of return? What is the effective rate of return per year? 2- Suppose you have borrowed $3000 now at a nominal interest rate of 10%. How much is it worth at the end of the ninth year? a) If interest rate is compounded quarterly. b) If interest rate is compounded continuously.

Timing of cash flow: • End of the period • Beginning of the period • Middle of the period • Continuous during the period EGR 403, Jan 99

Example on Different Timing 3- We would like to find the equivalent present worth of $4,000 paid sometime in future. Assume 20% interest rate. a) How much is the equivalent present worth if it is paid at the end of the first year? b) How much is the equivalent present worth if it is paid in the middle of the first year? c) How much is the equivalent present worth if it is paid at the beginning of the first year? d) How much is the equivalent present worth if it is paid continuously during the first year? Assume continuous compounding with nominal interest rate of 20%. EGR 403, Jan 04

Example on Patterns Recognition in Cash Flow Diagram You have two job offers with the following salary per year. Assume you will stay with a job for four years and the interest rate is 10%. Which one of the jobs will you select and why? Year 1 2 3 4 Job A $50,000 $52,500 $55,125 $57,881 Job B $52,000 $53,200 $54,400 $55,600

Example on Loan Analysis Assume you borrow $2,000 today, with an interest rate of 10% per year, to be repaid over five years in equal amounts (payments are made at the end of each year). The $2,000 is known as the principal of the loan. The amount of each payment can be calculated as below: A = 2000(A|P, 10%, 5) = $527.6 Each payment consists of two portions: interest over that year and part of the principal. The following table shows the amount of each portion for each of the payments. Notice that as time goes by you will pay less interest and your payment will cover more of the principal.

Loan Analysis A = 2000(A|P, 10%, 5) = 527.6 EGR 403, Jan 2000

Bond Analysis Bond is issued to raise funds through borrowing. The borrower will pay periodic interest (uniform payments: A) and a terminal value (face value: F) at the end of bond’s life (maturity date). The timing of the periodic payments and its amount are also indicated on each bond. Sometimes the bond's interest rate (rb), that is a nominal interest rate, is mentioned instead of the amount of each payment. The market price of a bond does not need to be equal to its face value. A = F * rb / m

Example on Bond A bond pays $100 quarterly. Bond’s face value is $2,000 and its maturity date is three years from now. a) What is the bond’s interest rate? rb = A*m/F = 100 * 4 / 2000 = 20% quarterly b) What is the present worth of the bond assuming that a nominal interest rate of 12% compounded quarterly is desirable. i = r/m = 12/4 = 3% per quarter Number of payments = n = 3*4 = 12 quarters P = 100(P|A, 3%, 12) + 2000(P|F, 3%, 12) = $2,398.2 EGR 403, Jan 2000