Download

1 / 12

120 likes | 411 Vues

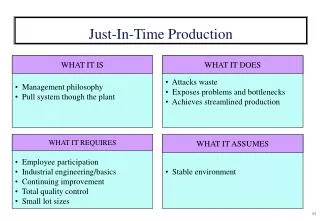

Just-in-Time Inventory and Production Management. No materials are purchased and no products are manufactured until they are needed. The primary goal of a JIT production system is to reduce or eliminate inventories at every stage of production. Key Features of the JIT Approach.

E N D

Just-in-Time Inventory and Production Management No materials are purchased and no products are manufactured until they are needed. The primary goal of a JIT production system is to reduce or eliminate inventories at every stage of production.

Key Features of the JIT Approach Smooth, uniform production rate Pull method of production Purchase is small lot sizes Quick, inexpensive setups High quality of materials Effective preventive maintenance Teamwork Multiskilled workers

JIT Purchasing Long-term contracts with suppliers. Only a few suppliers. Grouped payments to vendor. Minimal inspection of materials. Parts delivered in small lots.

Cost Assignment View Resource costs Process View Activity Analysis Activity Evaluation Performance Measures Root Causes Activity Triggers Activities Cost Objects Two-Dimensional ABC and Activity-Based Management

Assign resource costs to activity cost pools. Resource costs Performance Measures Root Causes Activity Triggers Activities Assign activity costs to cost objects using cost drivers. Cost Objects Two-Dimensional ABC and Activity-Based Management Cost Assignment View

Elimination of Non-Value-Added Costs Activities Analysis andClassification Nonvalue-addedActivities Value-addedActivities Reduce orEliminate Continually Evaluate and Improve

Using ABM to Eliminate Non-Value-Added Activities and Costs • Identify Activities. • Identify Non-Value-Added Activities. • Understand Activity Linkages, Root Causes, and Triggers. • Establish Performance Measures. • Report Non-Value-Added Costs. Specify parts Select vendor Receive parts Produce goods Inspect finished goods Rework defective products

Customer Profitability Analysis Customer profitability analysis uses activity-based costing to determine the activities, costs, and profit associated with serving particular customers.

Customer Profitability Analysis Requiredspecialpackaging. Orderssmallquantities. Demandfastservice. Oftenchangesorders. Ordersfrequently. A costly customer

Achieving Cost Reduction Activity Reduction Activity Selection Reduce Non-Value-Added Costs Activity Sharing Activity Elimination

Kaizen Costing The process of cost reduction during the manufacturing phase of an existing product. Product cost . Current year cost base. . Cost base for next year. 3/31/98 3/31/99

Kaizen Costing The process of cost reduction during the manufacturing phase of an existing product. Product cost . Kaizen goal cost-reduction amount. } . 3/31/98 3/31/99

![]Just In Time (JIT) Inventory Management](https://cdn4.slideserve.com/7168704/slide1-dt.jpg)