Download

1 / 7

160 likes | 685 Vues

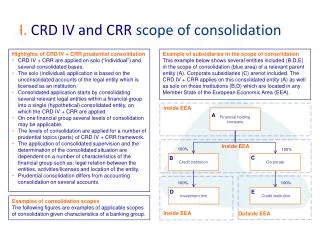

I . CRD IV and CRR scope of consolidation. Highlights of CRD IV + CRR prudential consolidation CRD IV + CRR are applied on solo (“individual”) and several consolidated bases.

E N D

I. CRD IV and CRR scope of consolidation • Highlights of CRD IV + CRR prudential consolidation • CRD IV + CRR are applied on solo (“individual”) and several consolidated bases. • The solo (individual) application is based on the unconsolidated accounts of the legal entity which is licensed as an institution. • Consolidated application starts by consolidating several relevant legal entities within a financial group into a single (hypothetical) consolidated entity, on which the CRD IV + CRR are applied. • On one financial group several levels of consolidation may be applicable. • The levels of consolidation are applied for a number of prudential topics(parts) of CRD IV + CRR framework. • The application of consolidated supervision and the determination of the consolidated situation are dependent on a number of characteristics of the financial group such as: legal relation between the entities, activities/licenses and location of the entity. • Prudential consolidation differs from accounting consolidation on several accounts. • Examples of consolidation scopes • The following figures are examples of applicable scopes of consolidation given characteristics of a banking group. Example of subsidiaries in the scope of consolidation This example below shows several entities included (B,D,E) in the scope of consolidation (blue area) of a relevant parent entity (A). Corporate subsidiaries (C) arenot included. The CRD IV + CRR applies on this consolidated entity (A) as well as solo on those institutions (B,D) which are located in any Member State of the European Economic Area (EEA). Inside EEA Financial holding company A Inside EEA 100% 100% C Credit institution B Corporate 100% 100% D E Investment firm Credit institution Inside EEA Outside EEA

II. Key factors in consolidation • Consolidation levels in the CRD IV + CRR framework • The application of CRD IV requirements on consolidation levels is additional to the application of CRD IV to the unconsolidated legal entity (“solo” = “individual”). However on the solo level, depending on the situation, waiver (CRR.7+8) may be granted. Within a complex banking group each of these levels may be applicable, however for less complex groups, some levels may not be applicable / coincide with other levels. • EU consolidation level • Member State consolidation level • CRR.22 sub-consolidation level • Specific liquidity sub-consolidation level • Inclusion of an entity in the scope of consolidation • An entity which is a subsidiary of a consolidating parent entity has to be included in the scope of consolidation, depending on a number of factors (non-exhaustive list): • Type (activities and licenses) of the parent undertaking • Location of the subsidiary • Type (activities and licenses) of the subsidiary • Size and risk of the subsidiary • Relation between the parent and the subsidiary • It should be noted that the parent undertaking is not necessarily the consolidating entity or itself subject to consolidated supervision. Any EEA Member State Relevant entity A EU consolidation group Any EEA Member State 100% B Relevant entity B Member State consolidation group Liquidity sub consolidation group 100% 100% Relevant entity D Relevant entity C CRR. 22 sub- consolidation group 100% 100% Relevant entity F Relevant entity E Other EEA Member State Non – EEA state

III. Relevant definitions CRR.4.1 – relevant definitions for this purpose (3) “institution” means a credit institution or an investment firm; (15) “parent undertaking” means: (a) a parent undertaking within the meaning of Articles 1 and 2 of Directive 83/349/EEC; (b) irrelevant (16) “subsidiary” means: (a) a subsidiary undertaking within the meaning of Articles 1 and 2 of Directive 83/349/EEC; (b) a subsidiary undertaking within the meaning of Article 1(1) of Directive 83/349/EEC and any undertaking over which a parent undertaking effectively exercises a dominant influence. Subsidiaries of subsidiaries shall also be considered to be subsidiaries of the undertaking that is their original parent undertaking; (18) “ancillary services undertaking” means an undertaking the principal activity of which consists of owning or managing property, managing data-processing services, or a similar activity which is ancillary to the principal activity of one or more institutions; (20) “financial holding company” means a financial institution, the subsidiaries of which are exclusively or mainly institutions or financial institutions, at least one of such subsidiaries being an institution, and which is not a mixed financial holding company; (26) “financial institution” means an undertaking other than an institution, the principal activity of which is to acquire holdings or to pursue one or more of the activities listed in points 2 to 12 and point 15 of Annex I to Directive 2013/36/EU, including a financial holding company, a mixed financial holding company, a payment institution within the meaning of Directive 2007/64/EC of the European Parliament and of the Council of 13 November 2007 on payment services in the internal market (1), and an asset management company, but excluding insurance holding companies and mixed-activity insurance holding companies as defined, respectively, in points (f) and (g) of Article 212(1) of Directive 2009/138/EC; (21) “mixed financial holding company” means mixed financial holding company as defined in point (15) of Article 2 of Directive 2002/87/EC; (28) “parent institution in a Member State” means an institution in a Member State which has a institution or a financial institution as a subsidiary or which holds a participation in such an institution or financial institution, and which is not itself a subsidiary of another institution authorised in the same Member State, or of a financial holding company or mixed financial holding company set up in the same Member State; (29) “EU parent institution” means a parent institution in a Member State which is not a subsidiary of another institution authorised in any Member State, or of a financial holding company or mixed financial holding company set up in any Member State; (30) “parent financial holding company in a Member State” means a financial holding company which is not itself a subsidiary of an institution authorised in the same Member State, or of a financial holding company or mixed financial holding company set up in the same Member State; (31) “EU parent financial holding company” means a parent financial holding company in a Member State which is not a subsidiary of an institution authorised in any Member State or of another financial holding company or mixed financial holding company set up in any Member State; (32) “parent mixed financial holding company in a Member State” means a mixed financial holding company which is not itself a subsidiary of an institution authorised in the same Member State, or of a financial holding company or mixed financial holding company set up in that same Member State; (33) “EU parent mixed financial holding company” means a parent mixed financial holding company in a Member State which is not a subsidiary of an institution authorised in any Member State or of another financial holding company or mixed financial holding company set up in any Member State;

IV. EU consolidation level • EU consolidation CRR.11.3 + CRD.111 • Trigger of consolidation • EU consolidation is triggered by the presence of at least one institution within the EEA. • Level of consolidation • EU level consolidation is applicable on the highest level of a group within the EEA (ultimate parent): • Special case if institutions are located in several MS controlled by a single non-EEA entity (CRD.111). • The highest level of a banking group at the EU consolidation level, could be a: • (Mixed) financial holding company • Institution. • Scope of consolidation • Within the scope of consolidation are all relevant entities, which are a subsidiary of the ultimate parent. • The location of those subsidiaries is irrelevant. • Relevant entities for EU consolidation are: • Financial institutions (including holding companies) • Institutions • Ancillary service undertakings • Consolidation of a subsidiary is evaluated from the perspective of the ultimate parent. Any EEA Member State Relevant entity A Any EEA Member State 100% B Relevant entity 100% C Relevant entity 100% 100% Relevant entity E Relevant entity D Other EEA Member State Non – EEA state

V. Member State consolidation level • Member State consolidation CRR.11.1 + CRR.1.2 • Trigger of consolidation • MS consolidation is triggered by the presence of at least one institution in the Member State concerned. • Level of consolidation • MS level consolidation is applicable on the highest level of a group within the Member State (MS parent): • Note: if MS level is identical to EU level, both apply • Note: MS level also triggers if there are no subs.. • The highest level of a banking group at the MS consolidation level, could be a: • (Mixed) financial holding company • Institution. • Scope of consolidation • Within the scope of consolidation are all relevant entities, which are a subsidiary of the MS parent. • The location of those subsidiaries is irrelevant. • Relevant entities for MS consolidation are: • Financial institutions (including holding companies) • Institutions • Ancillary service undertakings. • Consolidation of a subsidiary is evaluated from the perspective of the MS parent. Location irrelevant Irrelevant entity A Member State concerned 100% B Relevant entity 100% C Relevant entity 100% 100% Relevant entity E Relevant entity D Other EEA Member State Non – EEA state

VI. CRR.22 sub-consolidation level • CRR.22 sub-consolidation CRR.22 • Trigger of consolidation • CRR.22 sub-consolidation is triggered by the presence of an institution in the MS concerned and if there are any relevant non-EEA subsidiaries of any entity in the concerned MS. • Level of consolidation • CRR.22 sub level consolidation is applicable on the direct parent level of a sub-group (local parent). • Note: if CRR.22 is identical to MS level, both apply • Note: there are other separate cases of sub-consolidated supervision, not discussed here. • The highest level could be a: • (Mixed) financial holding company • Institution. • Scope of consolidation • Within the scope of consolidation are all relevant entities, which are a subsidiary of the local parent. • The location of those subsidiaries is irrelevant. • Relevant entities for CRR.22 sub-consolidation are: • Financial institutions (including holding companies) • Institutions • Ancillary service undertakings. Location irrelevant Irrelevant entity A Member State concerned 100% B Irrelevant entity 100% C Relevant entity 100% 100% Irrelevant entity E Relevant entity D Other EEA Member State Non – EEA state

VII. Liquidity specific sub-consolidation • Liquidity specific sub-consolidation CRR.8 • Trigger of consolidation • Liquidity specific sub-consolidation is triggered by a granted waiver under CRR.8.2 or CRR.8.3, and waives the solo liquidity application on those entities. • Upon granting the waiver, several institutions within the EEA (CRR.8.3 = sub-group 2) or within the same MS (CRR.8.2 = sub-group 1) form a single liquidity sub-group for the purpose of meeting CRR liquidity requirements: • Note a sub-group including subsidiaries in another MS may apply for a waiver as of 2015 (CRR.8.3). • Level of consolidation • Liquidity specific sub-consolidation is applicable on the direct parent level of the single liquidity sub-group: • Note: several liquidity groups could be formed. • The highest level of a banking group at the liquidity specific sub-consolidation level, could only be an: • Institution (CRR definition). • Scope of consolidation • Only those institutions which are in scope of the single liquidity sub-group are consolidated for this purpose. Location irrelevant Irrelevant entity A Member State concerned 100% B Relevant entity Single liquidity sub-group 1. 100% 100% Relevant entity D Relevant entity C Single liquidity sub-group 2. 100% 100% Relevant entity F Irrelevant entity E Other EEA Member State Non – EEA state