Download

1 / 7

70 likes | 275 Vues

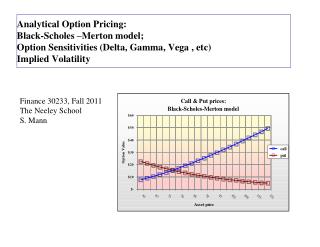

Options Pricing Using Black Scholes Model . By Christian Gabis. Variables. C = price of the call option S = price of the underlying stock X = option exercise price r = risk-free interest rate T = current time until expiration N() = area under the normal curve

E N D

Options Pricing Using Black Scholes Model By Christian Gabis

Variables • C = price of the call option • S = price of the underlying stock • X = option exercise price • r = risk-free interest rate • T = current time until expiration • N() = area under the normal curve • σ =standard deviation of stock return

The Formula • C = S N(d1) - X e-rT N(d2) • d1 = [ ln(S/X) + (r + σ2/2) T ] / σ T1/2 • d2 = d1 - σ T1/2

A Good Calculator • http://www.montegodata.co.uk/Consult/BS/bsm.htm • Also has many other pricing models • Black Scholes typically undervalues options

Using Options to Hedge • Using options as a kind of insurance • Reduces your return • Limits your downside • Will not work well with small amounts of capital ( too few shares for one option)

Example • You buy 100 shares of WAG for $36.00 for a position of $3600. • Then buy a $30 put to limit your downside. • The put option costs you $105 and is good until October. • There are 3 possible outcomes for this situation.

Outcomes • The stock goes to $30 leaving you with a position worth $3000 and a worthless option. Outcome: -$600-$105=-$705 • The stock climbs higher to $40 leaving you with a worthless put option and a $4000 position. Outcome : -$105+$400=$295 • The stock falls to $25 leaving you with a loss of $1100 and a gain on your option of roughly $500( market price will vary slightly). Your loss was limited because of the insurance effect of the option. Outcome : -$600