The Black-Scholes Model

The Black-Scholes Model. Randomness matters in nonlinearity . An call option with strike price of 10. Suppose the expected value of a stock at call option’s maturity is 10. If the stock price has 50% chance of ending at 11 and 50% chance of ending at 9, the expected payoff is 0.5.

The Black-Scholes Model

E N D

Presentation Transcript

Randomness matters in nonlinearity • An call option with strike price of 10. • Suppose the expected value of a stock at call option’s maturity is 10. • If the stock price has 50% chance of ending at 11 and 50% chance of ending at 9, the expected payoff is 0.5. • If the stock price has 50% chance of ending at 12 and 50% chance of ending at 8, the expected payoff is 1.

Applying Ito’s Lemma, we can find • Therefore, the average rate of return is r-0.5sigma^2. (But there could be problem because of the last term.)

The history of option pricing models • 1900, Bachelier, the purpose, risk management • 1950s, the discovery of Bachelier’s work • 1960s, Samuelson’s formula, which contains expected return • Thorp and Kassouf (1967): Beat the market, long stock and short warrant • 1973, Black and Scholes

Why Black and Scholes • Jack Treynor, developed CAPM theory • CAPM theory: Risk and return is the same thing • Black learned CAPM from Treynor. He understood return can be dropped from the formula

The Concepts Underlying Black-Scholes • The option price and the stock price depend on the same underlying source of uncertainty • We can form a portfolio consisting of the stock and the option which eliminates this source of uncertainty • The portfolio is instantaneously riskless and must instantaneously earn the risk-free rate • This leads to the Black-Scholes differential equation

The Derivation of the Black-Scholes Differential Equation continued

The Derivation of the Black-Scholes Differential Equation continued

The Differential Equation • Any security whose price is dependent on the stock price satisfies the differential equation • The particular security being valued is determined by the boundary conditions of the differential equation • In a forward contract the boundary condition is ƒ = S – K when t =T • The solution to the equation is ƒ = S – K e–r (T – t )

The payoff structure • When the contract matures, the payoff is • Solving the equation with the end condition, we obtain the Black-Scholes formula

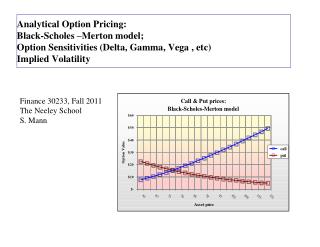

Properties of B-S formula • When S/Ke-rT increases, the chances of exercising the call option increase, from the formula, d1 and d2 increase and N(d1) and N(d2) becomes closer to 1. That means the uncertainty of not exercising decreases. • When σ increase, d1 – d2 increases, which suggests N(d1) and N(d2) diverge. This increase the value of the call option.

Variable S0 K ? ? T r D Effect of Variables on Option Pricing c p C P – – + + – – + + + + + + + + – – + + – – + +

Calculating option prices • The stock price is $42. The strike price for a European call and put option on the stock is $40. Both options expire in 6 months. The risk free interest is 6% per annum and the volatility is 25% per annum. What are the call and put prices?

Solution • S = 42, K = 40, r = 6%, σ=25%, T=0.5 • = 0.5341 • = 0.3573

Solution (continued) • =4.7144 • =1.5322

The Volatility • The volatility of an asset is the standard deviation of the continuously compounded rate of return in 1 year • As an approximation it is the standard deviation of the percentage change in the asset price in 1 year

Estimating Volatility from Historical Data • Take observations S0, S1, . . . , Sn at intervals of t years • Calculate the continuously compounded return in each interval as: • Calculate the standard deviation, s , of the ui´s • The historical volatility estimate is:

Implied Volatility • The implied volatility of an option is the volatility for which the Black-Scholes price equals the market price • The is a one-to-one correspondence between prices and implied volatilities • Traders and brokers often quote implied volatilities rather than dollar prices

Causes of Volatility • Volatility is usually much greater when the market is open (i.e. the asset is trading) than when it is closed • For this reason time is usually measured in “trading days” not calendar days when options are valued

Dividends • European options on dividend-paying stocks are valued by substituting the stock price less the present value of dividends into Black-Scholes • Only dividends with ex-dividend dates during life of option should be included • The “dividend” should be the expected reduction in the stock price expected

Calculating option price with dividends • Consider a European call option on a stock when there are ex-dividend dates in two months and five months. The dividend on each ex-dividend date is expected to be $0.50. The current share price is $30, the exercise price is $30. The stock price volatility is 25% per annum and the risk free interest rate is 7%. The time to maturity is 6 month. What is the value of the call option?

Solution • The present value of the dividend is • 0.5*exp (-2/12*7%)+0.5*exp(-5/12*7%)=0.9798 • S=30-0.9798=29.0202, K =30, r=7%, σ=25%, T=0.5 • d1=0.0985 • d2=-0.0782 • c= 2.0682

American Calls • An American call on a non-dividend-paying stock should never be exercised early • Theoretically, what is the relation between an American call and European call? • What are the market prices? Why? • An American call on a dividend-paying stock should only ever be exercised immediately prior to an ex-dividend date

Put-Call Parity; No Dividends (Equation 8.3, page 174) • Consider the following 2 portfolios: • Portfolio A: European call on a stock + PV of the strike price in cash • Portfolio C: European put on the stock + the stock • Both are worth MAX(ST, K ) at the maturity of the options • They must therefore be worth the same today • This means that c + Ke -rT = p + S0

An alternative way to derive Put-Call Parity • From the Black-Scholes formula

Arbitrage Opportunities • Suppose that c = 3 S0= 31 T = 0.25 r= 10% K =30 D= 0 • What are the arbitrage possibilities when p = 2.25 ? p= 1 ?

Application to corporate liabulities • Black, Fischer; Myron Scholes (1973). "The Pricing of Options and Corporate Liabilities

Put-Call parity and capital tructure • Assume a company is financed by equity and a zero coupon bond mature in year T and with a face value of K. At the end of year T, the company needs to pay off debt. If the company value is greater than K at that time, the company will payoff debt. If the company value is less than K, the company will default and let the bond holder to take over the company. Hence the equity holders are the call option holders on the company’s asset with strike price of K. The bond holders let equity holders to have a put option on there asset with the strike price of K. Hence the value of bond is

Value of debt = K*exp(-rT) – put • Asset value is equal to the value of financing from equity and debt • Asset = call + K*exp(-rT) – put • Rearrange the formula in a more familiar manner • call + K*exp(-rT) = put + Asset

Example • A company has 3 million dollar asset, of which 1 million is financed by equity and 2 million is finance with zero coupon bond that matures in 5 years. Assume the risk free rate is 7% and the volatility of the company asset is 25% per annum. What should the bond investor require for the final repayment of the bond? What is the interest rate on the debt?

Discussion • From the option framework, the equity price, as well as debt price, is determined by the volatility of individual assets. From CAPM framework, the equity price is determined by the part of volatility that co-vary with the market. The inconsistency of two approaches has not been resolved.

Homework • The stock price is $50. The strike price for a European call and put option on the stock is $50. Both options expire in 9 months. The risk free interest is 6% per annum and the volatility is 25% per annum. If the stock doesn’t distribute dividend, what are the call and put prices? If the stock is expected to distribute $1.5 dividend after 5 months, what are the call and put prices?

Three investors are bullish about Canadian stock market. Each has ten thousand dollars to invest. Current level of S&P/TSX Composite Index is 12000. The first investor is a traditional one. She invests all her money in an index fund. The second investor buys call options with the strike price at 12000. The third investor is very aggressive and invests all her money in call options with strike price at 13000. Suppose both options will mature in six months. The interest rate is 4% per annum, compounded continuously. The implied volatility of options is 15% per annum. For simplicity we assume the dividend yield of the index is zero. If S&P/TSX index ends up at 12000, 13500 and 15000 respectively after six months. What is the final wealth of each investor? What conclusion can you draw from the results? Homework

Homework • Use Excel to demonstrate how the change of S, K, T, r and σ affect the price of call and put options. If you don’t know how to use Excel to calculate Black-Scholes option prices, go to COMM423 syllabus page on my teaching website and click on Option calculation Excel sheet

Homework • The price of a non-dividend paying stock is $19 and the price of a 3 month European call option on the stock with a strike price of $20 is $1. The risk free rate is 5% per annum. What is the price of a 3 month European put option with a strike price of $20?

Homework • A 6 month European call option on a dividend paying stock is currently selling for $5. The stock price is $64, the strike price is $60 and a dividend of $0.80 is expected in 1 month. The risk free interest rate is 8% per annum for all maturities. What opportunities are there for an arbitrageur?

Homework • A company has 3 million dollar asset, of which 1 million is financed by equity and 2 million is finance with zero coupon bond that matures in 10 years. Assume the risk free rate is 7% and the volatility of the company asset is 25% per annum. What should the bond investor require for the final repayment of the bond? What is the interest rate on the debt? How about the volatility of the company asset is 35%?