BACCT3201 AUDIT II

320 likes | 665 Vues

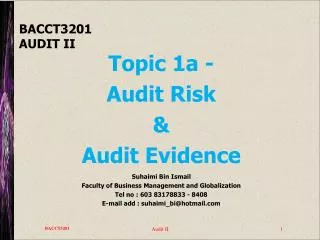

BACCT3201 AUDIT II. Topic 1a - Audit Risk & Audit Evidence Suhaimi Bin Ismail Faculty of Business Management and Globalization Tel no : 603 83178833 - 8408 E-mail add : suhaimi_bi@hotmail.com. Learning Objectives.

BACCT3201 AUDIT II

E N D

Presentation Transcript

Audit II BACCT3201AUDIT II Topic 1a - Audit Risk & Audit Evidence Suhaimi Bin Ismail Faculty of Business Management and Globalization Tel no : 603 83178833 - 8408 E-mail add : suhaimi_bi@hotmail.com

Learning Objectives • Explain the importance of the concept of audit risk & its three components • Describe the relationship between audit risk and audit evidence • Define the concept of materiality used in auditing

Learning Objectives • State how the auditor arrives at judgements about materiality at the financial report level and in relation to individual account balances • Describe the relationship between materiality and audit evidence • State the categories of mgmt’s financial report assertions

Learning Objectives • Derive specific audit objectives from the categories of assertions • Indicate the factors that affect the sufficiency and appropriateness of audit evidence • Identify the types of corroborating information available to the auditor • Describe the three classifications of auditing procedure and their purpose

References • Text Chapter 5 • AUS 202 Objective & General Principles • AUS 306Materiality • AUS 402 Risk Assessments &Internal Control • AUS 502 Audit Evidence

References • AUS 504 External Communications • AUS 520 Management Representations • AUS 606 Using the Work of an Expert • AAS 5 Materiality • AASB1031 Materiality

Key Terms & Concepts • Analytical procedures • Audit evidence • Audit risk • Audit risk model • Completeness • Confirmations

Key Terms & Concepts • Control risk • Detection risk • Financial report assertions • Inherent risk • Materiality • Substantive procedures

Audit Risk Components • Inherent risk • A material misstatement will occur in the absence of controls • Control risk • Material misstatements will not be prevented or detected by controls

Audit Risk Components • Detection risk • Material misstatements will not be detected by the auditor • Audit risk • The auditor may express an inappropriate audit opinion

Summary of risk components not prevented or detected by IC’s Material mis-statement remaining undetected Susceptibility of assertions to material mis-statements Unqualified materially misstated FS Mis-statements prevented or detected by IC’s Detected by audit procedures INHERENT RISK CONTROL RISK DETECTION RISK AUDIT RISK internal control structure Auditor’s procedures for verifying assertions

Relationship among audit risk components • Quantified audit risk model AR = IR x CR x DR DR = AR IR x CR DR = 0.05 0.5 x 0.5 DR = 20%

Risk components matrix Control risk High Medium Low Low Low Medium High Inherent risk Low Medium Medium High Low Medium High High

Materiality • The concept of materiality • The auditor considers materiality when: • Determining the nature, timing & extent of audit procedures • Evaluating the effect of misstatements on the fair presentation of financial reports

Materiality • Financial report materiality • Fairness of financial report taken as a whole • Quantitative guidelines • Qualitative considerations

Materiality - Quantitative guidelines • Threshold • An amount equal to or greater than 10% of an appropriate base amount is regarded as material • An amount equal to or less than 5% of an appropriate base amount is regarded as immaterial

Materiality - Quantitative guidelines • Common bases • equity • appropriate asset or liability class total • operating profit or loss • average operating profit or loss • revenue

Materiality - Qualitative considerations • Irregularities • Inadequate or improper description of accounting policy • Imposition of regulatory restrictions • Related party transaction or event requiring disclosure

Materiality • Materiality at the account balance level • Fairness of individual account balances • Allocating financial report materiality

Materiality • Preliminary judgements about materiality • The relationship between materiality and audit evidence • Using materiality to evaluate audit evidence

Audit Objectives • Management’s Financial Report Assertions • Existence or occurrence • Completeness • Rights & obligations • Valuation & measurement • Disclosure • Specific audit objectives

Audit Evidence • Sufficiency of audit evidence • Materiality and risk • Economic factors • Population size & characteristics

Audit Evidence • Appropriateness of audit evidence • Relevance • Reliability • Source and nature of information • Timeliness • Objectivity • Reasonable basis

Analytical Confirmations Documentary Written representations Mathematical Oral Physical Electronic Types of Evidence

Reliability of documentary evidence MOST RELIABLE Examples Externally generated documents sent directly to the auditor • Cut-off bank statement • Confirmations Externally generated documents held by the client • Suppliers’ invoice • Bank statement • Receipted deposit slip • Receipted shipping document Internally generated documents that are circulated externally Internally generated documents that are not circulated • Duplicate sales invoice • Purchase requisitions LEAST RELIABLE

Auditing Procedures • Types of auditing procedure • Analytical procedures • Inspecting • Tracing • Vouching • Confirming

Auditing Procedures • Types of auditing procedure • Inquiring • Counting • Observing • Reperforming • Computer-assisted audit techniques

Vouching (test for overstatement) Tracing (test for understatement) Vouching vs Tracing DIRECTION OF TESTING ASSERTION Existence or occurrence Source document Journal Ledger Completeness

Auditing Procedures • Classification of auditing procedures • Procedures to obtain understanding • Tests of control • Substantive procedures • Tests of details of transactions • Tests of details of balances

Summary • Audits risk consists of three components • Materiality is considered at both the financial statement and account balance level • The auditors form an opinion by evaluating evidence

Further Information? • Insert details of additional resources here