What Comes After Bitcoin

What Comes After Bitcoin

What Comes After Bitcoin

E N D

Presentation Transcript

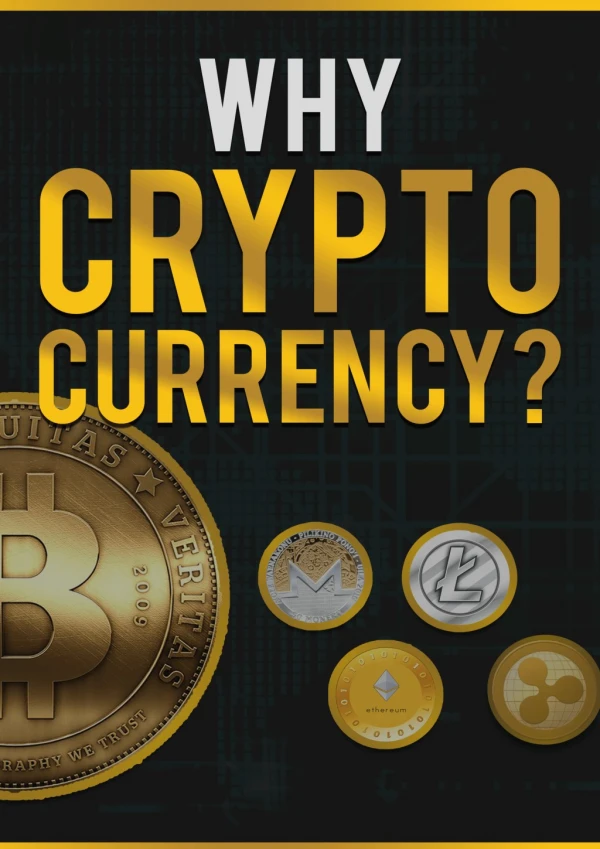

Bitcoin, a digital currency launched by the pseudonymous programmer Satoshi Nakamoto in 2009, hit a peak trading value of $266 per coin in April 2013, the biggest point in a bubble that would burst soon after. The cryptocurrency, which is anonymous, untrackable, and can be used to buy illicit goods online, caught the attention of the U.S. government—and not in a good way. In May, the U.S. Department of Homeland Security froze the Wells Fargo account of Mt. Gox, the largest exchange that trades Bitcoin for other currencies, arguing that the company broke anti-money laundering laws. On June 20, the exchange suspended withdrawals from its accounts in USD, leaving users with piles of less-than-liquid Bitcoin (still worth around $95 each).

But even as it drew political and legal controversy, Bitcoin highlighted the possibilities of a mainstream digital currency. “The current banking system sucks because it was invented 60 years ago, before the Internet was created,” Jonathan Mohan, the founder of BitcoinNYC, a digital currency-focused meet-up group, complained to me in a recent phone conversation. Cold, hard cash has inherent inefficiencies. It’s bulky and difficult to transfer between owners (wheelbarrows notwithstanding). These days, money is barely even paper bills—it’s just a number stored on a computer signifying credit or debit. Digital currencies take that idea one step further, creating self-regulating mediums of exchange through peer-to-peer networks.

Bitcoin might be the largest such network, but its success has given rise to a new generation of digital currencies, each with its own vision for the future of money. Ripple is one of the main contestants for the title of Bitcoin successor. Launched by OpenCoin, a company founded by Chris Larsen in 2012, Ripple is both a currency and a payment system that promises to create a frictionless, transparent method for instantly transferring money anywhere in the world, in any currency. It’s already catching on—in May of this year, the company received investment from none other than Google Ventures. “We are doing for money what email did for communication,” Larsen wrote to me.

OpenCoin is Larsen’s third technology start-up, but each business has changed how we think of money and what can be done with it. E-Loan made credit scores free and available to customers while Prosper created an online infrastructure for making personal loans outside of the banking system. “All three companies share a common DNA—to eliminate needless waste and middlemen in the financial process,” Larsen explained.

Ripple exists in two parts: the XRP, a mathematically regulated currency unit similar to Bitcoin, and a payment system. Users have “wallets” on the Ripple system that they can add value to in any currency by means of an online exchange backed by a bank, like Bitstamp (Mt. Gox doesn’t deal in XRP). Once the wallet is full, that value can be transferred to any other user on the Ripple network in any currency in seconds. Bitcoin transactions, in comparison, can often take minutes to verify.

When transferring money between currencies in today’s normal international banking system, the value has to move through several entities like banks and exchanges before it gets to the end user, and each middleman takes a cut of the value. Ripple minimizes that process to one step, moving effortlessly between USD, Yen, Bitcoin, XRP, or even Icelandic Krona with just one exchange. The only charge is a tiny fraction of an XRP (currently worth slightly more than a penny), which guards against the kind of large-scale cyber attacks that have disrupted Bitcoin.

Ripple’s potential is to make businesses like Western Union, which charges an average of 10.8 percent in money transfer fees, obsolete, giving a capital influx to countries that depend on worker remittances. It could also subsume Bitcoin itself. On July 2, OpenCoin announced that Ripple holders can send money to Bitcoin users in any currency, and they will receive it in Bitcoins. The move provides access to the Bitcoin economy for the newer currency, and also creates a simple bridge between Bitcoin and other non-digital currencies.

Sources: http://www.coinsetter.com Article: http://www.psmag.com/business-economics/ Template: http://www.dvd-ppt-slideshow.com/