Download

1 / 70

730 likes | 993 Vues

General Ledger Accounting. Jennifer Rodenbeck, CPA, CPFO City of Cedar Falls Finance Manager/City Clerk July 24, 2013 Jennifer.rodenbeck@cedarfalls.com. Class Today . Class List with Email Handouts – Wait to email them to you Definitions Breaks. Introductions. What City you are from

E N D

General Ledger Accounting Jennifer Rodenbeck, CPA, CPFO City of Cedar Falls Finance Manager/City Clerk July 24, 2013 Jennifer.rodenbeck@cedarfalls.com

Class Today • Class List with Email • Handouts – Wait to email them to you • Definitions • Breaks

Introductions • What City you are from • Approximate size of City • What is your position • How long in your position • Most difficult thing you are dealing with currently at work as it relates to finances

Basic Accounting • Assets – Definition: Resources of the City that may or may not be currently available to conduct the activity of the City. Ex. Cash, investments, equipment (Debit Balance) • Liabilities – Definition: Demands and obligations upon the City. Ex. Accounts Payable(Credit Balance) • Fund Balance (Equity) – Credit Balance • Revenues – Credit Balance • Expenses – Debit Balance • Double Entry – Definition: Every entry has two parts, a debit and a credit • Journal Entry – Definition: A balanced set of entries used to reflect transactions.

Liabilities Assets Expenses Revenues Fund Balance (Net Difference)

Governmental Accounting • Why different??? • Funds • Double - Double Entries for everything

Manual Accounting • Why is it important??? • Understanding what your software is doing! • Why??? • Doesn’t Balance • Make Corrections • Setting up new software

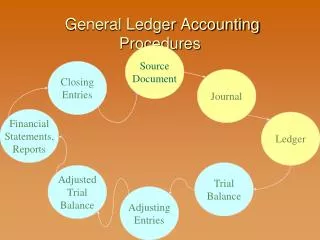

General Ledger • Why is it important to us??? • Accurate information for annual reporting, budgeting • Audit • Public record

MY CITY:LEDGERS • Three Ledgers needed • General Ledger • Subsidiary Ledger • Budget Ledger • Double Entry Accounting: Every entry has two parts, a debit and a credit within each of the ledger types.

GENERAL LEDGER • Definition: The fund summary or monthly recording of activities which combine the values of the subsidiary and budgetary ledgers to establish financial position of the City.

SUBSIDIARY LEDGER • Definition: The record of detail used for individual accounts within a cost center and/or fund. • Each line item or account number has a running total throughout the year • Each line item or account number must belong to a larger grouping: revenue type or department or function

BUDGET LEDGER • Definition: The record of budgetary expenditures compared to the allocated budget for that function, fund or project. • Used to monitor or control revenues by type • Used to monitor or control expenditures by functions • Usually some portion of account number or code is used to generate totals for ledger (chart of accounts)

CHART OF ACCOUNTS City Standard Chart of Accounts Definition: A standardized method to insure consistency between budget, accounting, and financial reporting activities.

Account Numbers Expense: 001-1010-6010 – General Fund – Police – Full Time Salary Revenue: 001-1010-1-4765 – General Fund – Police – Misc Revenue - Fines Cash: 001-1110 – General Fund – Cash Accounts Payable: 001-2020 – General Fund – Accounts Payable Fund Balance: 001-3860 – General Fund – Unreserved Fund Balance

GENERAL LEDGER A PRACTICAL GUIDE

GENERAL LEDGER Liabilities Assets Fund Balance Revenue Control Expenditure Control

SUBSIDIARY LEDGER - Revenue Property Taxes Revenue Control Hotel/Motel Taxes Interest Income

SUBSIDIARY LEDGER - Expenditures Office Supplies Expenditure Control Professional Fees Capital Outlay

BUDGET LEDGER Appropriations Estimated Revenues Budget Fund Balance

GENERAL LEDGER 001-2020 Accts Payable 001-1110 Cash $5,000 001-3860 Unreserved Fund Balance $5,000 Dr. Cash $5,000 Cr. Equity $5,000 - To record beginning balance

BUDGET LEDGER Appropriations Estimated Revenues $50,000 $50,000 Budget Fund Balance $0

Received the following revenues: $40,000 Property Tax Revenue $2,000 Building Permits $1,000 Interest Income

Dr. Cash $43,000 Cr. P/T Rev $40,000 Cr. Bldg Permit Rev $ 2,000 Cr. Int Income $ 1,000 Total $43,000 $43,000

SUBSIDIARY LEDGER - Revenue 001-4000 Property Taxes $40,000 001-1900 Revenue Control $43,000 001-4122 Building Permits $2,000 001-4300 Interest Income $1,000

GENERAL LEDGER 001-2020 Accts Payable 001-1110 Cash $5,000 $43,000 001-3860 Unreserved Fund Balance $5,000 $43,000

BUDGET LEDGER Appropriations Estimated Revenues $50,000 $50,000 $43,000 Budget Fund Balance $0 $43,000

Paid the following expenditures: $3,000 New City Clerk Desk $10,000 Audit Fee $20,000 Police Car

Dr. Office Supp $3,000 Dr. Prof Fees $10,000 Dr. Cap Outlay $20,000 Cr. Cash $33,000 Total $33,000 $33,000

SUBSIDIARY LEDGER - Expenditures 001-6506 Office Supplies $3,000 001-2900 Expenditure Control $33,000 001-6401 Professional Fees $10,000 001-6700 Capital Outlay $20,000

GENERAL LEDGER 001-2020 Accts Payable 001-1110 Cash $5,000 $33,000 $43,000 $15,000 001-3860 Unreserved Fund Balance $5,000 $33,000 $43,000 $15,000

BUDGET LEDGER Appropriations Estimated Revenues $50,000 $50,000 $43,000 $33,000 $17,000 $7,000 Budget Fund Balance $0 $43,000 $33,000 $10,000

City of Boondocks • Cash on Hand at Beginning of Year = $10,000 • Only One Fund – General Fund • Received the following revenues: • Property taxes - $75,000 • Mobile home taxes = $1,000 • Interest Income = $2,000 • Electrical Permits = $5,000 • Swimming Pool receipts = $20,000 • Library donation = $30,000 • Paid the following expenses: • Staff training = $2,000 • Building repair = $10,000 • Auditor = $25,000 • Engineer Study = $50,000 • Clerk’s desk = $5,000 • Total budgeted revenues = $200,000 • Total budgeted expenses = $180,000

Case Study Entries & Annual Financial Report Preparation

Payroll • Gross Payroll - • payroll + city share of benefits = • TOTAL COST OF PAYROLL

Dr. Salaries $500 Dr. FICA $ 38 Dr. IPERS $ 45 Cr. Cash $422 Cr. Cash $ 83 Cr. W/H Liab $ 78 Total $583 $583

GENERAL LEDGER 001-2120 Accrued Payroll Taxes 001-1110 Cash $422 $78 $83 $505 001-3860 Unreserved Fund Balance $583

SUBSIDIARY LEDGER - Expenditures 001-6020-6010 Salaries $500 Expenditure Control $583 001-6020-6110 FICA $38 001-6020-6130 IPERS $45

GENERAL LEDGER 001-2120 Accrued Payroll Taxes 001-1110 Cash $422 $78 $83 $505 $78 $78 $583 001-3860 Unreserved Fund Balance $583 Assets + Liab = Equity

Voided Checks 001-1110 Cash on Hand 001-4310 Rents Journal Entry: DR CR 001-4310 25.00 Returned: Bad check for rental 001-1110 25.00

Sale of Bonds 300-1110 Cash on Hand 300-4820 Proceeds from Bonds and Premiums Journal Entry: DR CR 300-1110 250,000 Bond Fund 300-4820 250,000