Download

1 / 10

100 likes | 292 Vues

CHARITABLE GIFT ANNUITY very simple explanation.

E N D

CHARITABLE GIFT ANNUITY very simple explanation • Donor(s) and nonprofit contractually agree that in exchange for an irrevocable gift of cash, appreciated marketable securities, or other acceptable assets, the nonprofit will pay to one or two predetermined annuitants (the annuity income recipients) annual fixed lifetime payments, which often can be broken down into quarterly, semi-annual, or annual payments. • Very often the donor(s) is also the annuitant. • The lifetime payments are guaranteed and fully backed by all of the nonprofit’s assets. • Once the lifetime annuity payments stop, the remaining funds go to the nonprofit. example for explanation purposes only - this is not tax or legal advice

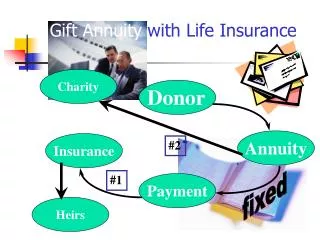

CHARITABLE GIFT ANNUITY CONTRIBUTION Nonprofit • REMAINDER Nonprofit Charitable Gift Annuity GIFT ANNUITY PAYMENTS TAX DEDUCTION example for explanation purposes only - this is not tax or legal advice

Charitable Gift Annuity “Rules & Regs” • Each State has different regulations: • Notices, permits, contracts, reserve funds, filings should be checked on website for American Council for Gift Annuities (ACGA) www.acga-web.org • Funded with cash, appreciated marketable securities (and sometimes other marketable assets, including real estate) and cannot be added to once established. • Maximum of two annuitants (income recipients). • Assets are segregated and protected from creditors. • Donor(s) get tax deduction for charitable interest. • Annuity payments are tax advantaged (due to return of some principal) • Tax advantaged treatment of capital gain example for explanation purposes only - this is not tax or legal advice

Current Payouts begin immediately and are prorated. Current tax deduction for charitable interest (max of 30% of AGI for gift of appreciated property and 50% for cash gift) Very competitive rates compared to CDs, money markets, and some equity and bond yields (this comparison is frowned upon because the vehicles are not really comparable) Deferred Payments begin on a pre-determined date, after at least a year has passed since the gift was made. Current tax deduction for charitable interest max of 30% of AGI for gift of appreciated property and 50% for cash gift) High rates due to deferral period. Flexible (type of deferred) Elect to start receiving payments on any one of a range of dates specified in contract, which also includes amounts to be paid. Current, Deferred & Flexible Gift Annuities example for explanation purposes only - this is not tax or legal advice

BENEFITS INCLUDE: 1) They will qualify for a federal income tax deduction of approximately $38,698. The deduction may vary modestly depending on the timing of your gift. Note that deductions for this and other gifts of cash and non-appreciated property will be limited to 50% of donor’s adjusted gross income. If necessary, unused deductions of this kind may be taken over the next five years, subject to the same 50% limitation. If the donation were appreciated property, the deduction is limited to 30% of donor’s adjusted gross income. 2) The designated annuitant will receive fixed payments in quarterly installments totaling $5,400 each year for life. In addition, $4,228.20 of each year's payments will be tax-free for the first 14.5 years. 3)Donor’s estate may enjoy reduced probate costs and estate taxes. 4)Generous support eventually goes to your nonprofit. Prepared for easyPG June 26, 2012 These calculations are for illustration purposes only and should not be considered legal, accounting, or other professional advice. Your actual benefits may vary depending on the timing of the gift. • EXAMPLE FOR ONE LIFE CURRENT ANNUITY: • On 6/26/12, your donor irrevocably transfers $100,000 in cash to your nonprofit in exchange for a $5,400 annuity for an annuitant, age 72. example for explanation purposes only - this is not tax or legal advice

CHARITABLE GIFT ANNUITY CONTRIBUTION $100,000.00 CASH Nonprofit • REMAINDER Nonprofit Charitable Gift Annuity 72 year Old donor and also annuitant Current recommended ACGA rate for 72 yr. old = 5.4% ANNUAL GIFT ANNUITY PAYMENTS OF $5,400.00 (of which$4,228.20 is tax-free for life expectancy of 14.5 years) CHARITABLE TAX DEDUCTION $38,968.00 example for explanation purposes only - this is not tax or legal advice

example for explanation purposes only - this is not tax or legal advice

example for explanation purposes only - this is not tax or legal advice

THIS FORM MUST BE PROVIDED TO DONOR IF USING A 7520 RATE WITH A TWO MONTH DIFFERENTIAL (as in this example) Applicable Mid-Term Rate Election Charitable Gift Annuity Donor Name: Taxpayer ID: According to Reg. Sec. 301.9100-8(a)(1), I, , am making an election as provided under Section 7520(a) of the Internal Revenue Code. The interest being valued is a charitable gift annuity agreement with <Charity Name> made on June 26, 2012. The payout rate of the gift is 5.4%, payable for the lifetime benefit of an individual, age 72. The rate being used to value the transferred interest is that for May, 2012, 1.6% (120% of the Applicable Mid-Term Federal Interest Rate rounded to the nearest two-tenths of one percent). • Instructions to Donor • You are receiving the above election statement because the IRS discount rate used to compute the value of your charitable contribution was based on a rate for one of the two months prior to the month of your gift. • The IRS requires a planned gift donor to make an explicit election in the event that the value of the donor's charitable contribution was computed using the IRS discount rate for either of the two months prior to the month of gift. The month of your gift is June, 2012 and the IRS discount rate used to compute the value of your charitable contribution is for May, 2012. • You must attach the election statement to your federal income tax return for the tax year in which you claim your income tax charitable deduction for this gift. You should provide your tax preparer with a copy of this election statement example for explanation purposes only - this is not tax or legal advice

Why I Really Like Charitable Gift Annuities • They enable donations from supporters who might not otherwise be able to make a gift. • They bring in revenues that might not otherwise be contributed to charity. • They actually benefit donors during their lifetime (enhancing their love for your nonprofit). • They can be an additional incentive to give. • They are irrevocable (although you may end up better off if the same amount is contributed through a revocable will or POD designation instead) • Part of the gift is given back through annuity payments so only ½ to 1/3 may remain for the nonprofit example for explanation purposes only - this is not tax or legal advice