Derivatives : A Primer on Bonds

730 likes | 1.08k Vues

Derivatives : A Primer on Bonds. First Part: Fixed Income Securities Bond Prices and Yields Term Structure of Interest Rates Second Part: TSOIR Term Structure of Interest Rates Interest Rate Risk & Bond Portfolio Management. Bond Prices and Yields. Time value of money and bond pricing

Derivatives : A Primer on Bonds

E N D

Presentation Transcript

Derivatives: A Primer on Bonds • First Part: Fixed Income Securities • Bond Prices and Yields • Term Structure of Interest Rates • Second Part: TSOIR • Term Structure of Interest Rates • Interest Rate Risk & Bond Portfolio Management

Bond Prices and Yields • Time value of money and bond pricing • Time to maturity and risk • Yield to maturity • vs. yield to call • vs. realized compound yield • Determinants of YTM • risk, maturity, holding period, etc.

Bond Pricing • Equation: • P = PV(annuity) + PV(final payment) • = • Example: Ct = $40; Par = $1,000; disc. rate = 4%; T=60

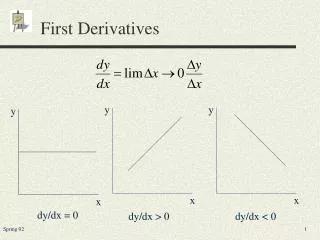

Prices vs. Yields • P yield • intuition • convexity • BKM6 Fig. 14.3; ; BKM4 Fig. 14.6 • intuition: yield P price impact

Measuring Rates of Return on Bonds • Standard measure: YTM • Problems • callable bonds: YTM vs. yield to call • default risk: YTM vs. yield to expected default • reinvestment rate of coupons • YTM vs. realized compound yield • Determinants of the YTM • risk, maturity, holding period, etc.

Measuring Rates of Return on Bonds 2 • Yield To Maturity • definition • discount rate such that NPV=0 • interpretation • (geometric) average return to maturity • Example: Ct = $40; Par = $1,000; T=60; sells at par

Measuring Rates of Return on Bonds 3 • Yield To Call • definition • discount rate s.t. NPV=0, with TC = earliest call date • deep discount bonds vs. premium bonds • BKM6 Fig. 14.4; ; BKM4 Fig. 14.7 • Example: Ct = $40, semi; Par = $900; T=60; P = $1,025; callable in 10 years (TC=20), call price = $1,000

Measuring Rates of Return on Bonds 4 • Yield To Default • definition • discount rate s.t. NPV=0, with TD= expected default date • default premium and business cycle • economic difficulties and “flight to quality” • Example: Ct = $50, semi; Par = $1,000; T=10; P = $200; expected to default in 2 years (TC=4), recover $150

Measuring Rates of Return on Bonds 5 • Coupon reinvestment rate • YTM assumption: average • problem: not often true • “solution”: realized compound yield • forecast future reinvestment rates • compute future value (BKM6 Fig.14.5; BKM4 Fig.14.9) • compute the yield (rcy) such that NPV = 0 • practical? • need to forecast reinvestment rates

Bond Prices over Time • Discount bonds vs. premium bonds • coupon rate < market interest rates • built-in capital gain (discount bond) • coupon rate > market interest rates • built-in capital loss (premium bond) • Behavior of prices over time • BKM6 Fig. 14.6; BKM4 Fig. 14.10 • Tax treatment • capital gains vs. interest income

Discount Bonds • OID vs. par bonds • original issue discount (OID) bonds • less common • coupon need not be 0 • par bonds • most common • Zeroes • what? mostly Treasury strips • how? “certificates of accrual”, “growth receipts”, ... • annual price increase = 1-year disc. factor (BKM6 Fig. 14.7; BKM4 Fig. 14.11)

OID tax treatment -- Discount Bonds 2 • Idea for zeroes • built-in appreciation = implicit interest schedule • tax the schedule as interest, yearly • tax the remaining price change as capital gain or loss • Other OID bonds • same idea • taxable interest = coupon + computed schedule

OID tax treatment -- Discount Bonds 3 • Example • 30-year zero; issued at $57.31; Par = $1,000 • compute YTM: • 1st year taxable interest

OID tax treatment -- Discount Bonds 4 • Example (continued) • interests on 30-year bonds fall to 9.9% • capital gain • tax treatment: taxable interest = $5.73; capital gain

Term Structure of Interest Rates • Basic question • link between YTM and maturity • Bootstrapping short rates from strips • forward rates and expected future short rates • Recovering short rates from coupon bonds • Interpreting the term structure • does the term structure contain information? • certainty vs. uncertainty

“Term”inology • Term structure = yield curve (BKM6 Fig. 15.1) • = plot of the YTM as a function of bond maturity • = plot of the spot rate by time-to-maturity • Short rate vs. spot rate • 1-period rate vs. multi-period yield • spot rate = current rate appropriate to discount a cash-flow of a given maturity • BKM6 Figure 15.3; BKM4 Figure 14.3

Extracting Info re:Short Interest Rates • From zeroes • non-linear regression analysis • bootstrapping • From coupon bonds • system of equations • regression analysis (no measurement errors) • Certainty vs. uncertainty • forward rate vs. expected future (spot) short rate

Bootstrapping Fwd Rates from Zeroes • Forward rate • “break-even rate” – BKM Fig. 15.4 • equates the payoffs of roll-over and LT strategies • Uncertainty • no guarantee that forward = expected future spot • General formula • f1 = YTM1 and

Bootstrapping Fwd from Zeroes 2 • Data • BKMTable 15.2 & Fig. 15.1 • 4 bonds, all zeroes (reimbursable at par of $1,000) • T Price YTM • 1 $925.93 8% • 2 $841.75 8.995% • 3 $758.33 9.66% • 4 $683.18 9.993%

Bootstrapping Fwd Rates from Zeroes 3 • Forward interest rate for year 1 • Forward interest rate for year 2

Bootstrapping Fwd Rates from Zeroes 4 • Short rate for years 3 and 4 • keep applying the method • you find f3 = 11% = f4 • General Formula • f1 = YTM1

Yield, Maturity and Period Return • Data • 2 bonds, both zeroes (reimbursable at par of $1,000) • T Price YTM • 1 $925.93 8% • 2 $841.75 8.995% • Question • investor has 1-period horizon; no uncertainty • does bond 2 (higher YTM) dominate bond 1?

Yield, Maturity and Period Return 2 • Answer: Nope • Bond 1 HPR: • Bond 2 HPR: • f2 = 10% • price in 1 year = Par/(1+ f2) = $ 909.09 • capital gain at year-1 end =

Fwd Rate & Expected Future Short Rate • Interpreting the term structure • Short perspective • liquidity preference theory (investors) • liquidity premium theory (issuer) • Expectations hypothesis • Long perspective • Market Segmentation vs. Preferred Habitat • Examples

Fwd Rate & Exp. Future Short Rate 2 • Short perspective • liquidity preference theory (“short” investors) • investors need to be induced to buy LT securities • example: 1-year zero at 8% vs. 2-year zero at 8.995% • liquidity premium theory (issuer) • issuers prefer to lock in interest rates • f2 E[r2] • f2= E[r2] + risk premium

Fwd Rate & Exp. Future Short Rate 3 • Long perspective • “long investors” wish to lock in rates • roll over a 1-year zero at 8% • or lock in via a 2-year zero at 8.995% • E[r2]f2 • f2= E[r2] - risk “premium”

Fwd Rate & Exp. Future Short Rate 4 • Expectation Hypothesis • risk premium = 0 and E[r2]=f2 • idea: “arbitrage” • Market segmentation theory • idea: clienteles • ST and LT bonds are not substitutes • reasonable? • Preferred Habitat Theory • investors do prefer some maturities • temptations exist

Fwd Rate & Exp. Future Short Rate 5 • In practice • liquidity preference + preferred habitat • hypotheses have the edge • Example • BKM Fig. 15.5

Fwd Rate & Exp. Future Short Rate 6 • Example 2 • short term rates: r1=r2 =r3 = 10% • liquidity premium = constant 1% per year • YTM

Measurement: Zeroes vs. Coupon Bonds • Zeroes • ideal • lack of data may exist (need zeroes for all maturities) • Coupon Bonds • plentiful • coupons and their reinvestment • low coupon rate vs. high coupon rate • short term rates -> they may have different YTM

Short Rates, Coupons and YTM • Example • short rates are 8% & 10% for years 1 & 2; certainty • 2-year bonds; Par = $1,000; coupon = 3% or 12% • Bond 1: • Bond 2:

Measurements with Coupon Bonds 2 • Example • 2-year bonds; Par = $1,000; coupon = 3% or 12% • Prices: $894.78 (coupon = 3%); $1,053.87 (coupon = 12%) • Year-1 and Year-2 short rates • $ 894.78 = d1 x 30 + d2 x 1,030 • $ 1,053.87 = d1 x 120 + d2 x 1,120 • Solve the system: d2 = 0.8417, d1 = 0.9259 • Conclude ...

Measurements with Coupon Bonds 3 • Example (continued)

Measurements with Coupon Bonds 4 • Practical problems • pricing errors • taxes • are investors homogenous? • investors can sell bonds prior to maturity • bonds can be called, put or converted • prices quotes can be stale • market liquidity • Estimation • statistical approach

Rising yield curves • Causes • either short rates are expected to climb: E[rn] E[rn-1] • or the liquidity premium is positive • Fig. 15.5a • Interpretative assumptions • estimate the liquidity premium • assume the liquidity premium is constant • empirical evidence • liquidity premium is not constant; past -> future?!

Inverted yield curve • Easy interpretation • if there is a liquidity premium • then inversion expectations of falling short rates • why would interest rates fall? • inflation vs. real rates • inverted curve recession? • Example • current yield curve: The Economist

Fixed Income Portfolio Management • In general • bonds are securities just like other • -> use the CAPM • Bond Index Funds • Immunization • net worth immunization • contingent immunization

Bond Index Funds • Idea • US indices • Solomon Bros. Broad Investment Grade (BIG) • Lehman Bros. Aggregate • Merrill Lynch Domestic Master • composition • government, corporate, mortgage, Yankee • bond maturities: more than 1 year • Canada: ScotiaMcLeod (esp. Universe Index)

Bond Index Funds 2 • Problems • lots of securities in each index • portfolio rebalancing • market liquidity • bonds are dropped (maturities, calls, defaults, …)

Bond Index Funds 3 • Solution: • “cellular approach” • idea • classify by maturity/risk/category/… • compute percentages in each cell • match portfolio weights • effectiveness • average absolute tracking error = 2 to 16 b.p. / month

Special risks for bond portfolios • cash-flow risk • call, default, sinking funds, early repayments,… • solution: select high quality bonds • interest rate risk • bond prices are sensitive to YTM • solution • measure interest rate risk • immunize

Interest Rate Risk • Equation: • P = PV(annuity) + PV(final payment) • = • Yield sensitivity of bond Prices: • P yield • Measure?

Interest Rate Risk 2 • Determinants of a bond’s yield sensitivity • time to maturity • maturity sensitivity (concave function) • coupon rate • coupon sensitivity • discount bond vs. premium bond • zeroes have the highest sensitivity • intuition: coupon bonds = average of zeroes • YTM • initial YTM sensitivity

Duration • Idea • maturity sensitivity • to measure a bond’s yield sensitivity, • measure its “effective maturity” • Measure • Macaulay duration:

Duration 2 • Duration = effective measure of elasticity • Proof • Modified duration with

Duration 4 • Interpretation 1 • = average time until bond payment • Interpretation 2 • % price change of coupon bond of a given duration • = % price change of zero with maturity = to duration

Duration 4 • Example (BKM Table 15.3) • suppose YTM changes by 1 basis point (0.01%) • zero coupon bond with 1.8853 years to maturity • old price • new price

Duration 5 • Example: BKM4 Table 15.3 • suppose YTM changes by 1 basis point (0.01%) • coupon bond • either compare the bond’s price with YTM = 5.01% relative to the bond’s price with YTM = 5% • or simply compute the price change from the duration