Download

1 / 21

220 likes | 1.47k Vues

Limitations of Analysis. Dr. Clive Vlieland-Boddy. No more ratios, please!. Limitations of Financial Statement Analysis. Differences in accounting methods between companies sometimes make comparisons difficult. We use the FIFO method to value inventory.

E N D

Limitations of Analysis Dr. Clive Vlieland-Boddy

Limitations of Financial Statement Analysis Differences in accounting methods between companies sometimes make comparisons difficult. We use the FIFO method to value inventory. We use the LIFO method to value inventory.

Changes within the company • Industry trends • Consumer tastes • Technological changes • Economic factors Limitations of Financial Statement Analysis Analysts should look beyond the ratios.

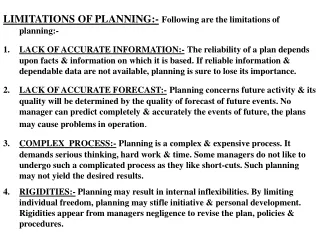

Limitations Of Financial Analysis • Horizontal, vertical, and ratio analysis are frequently used in making significant business decisions. • One should be aware of the limitations of these tools and the financial statements. • Business decisions are made in a world of uncertainty. • No single ratio or one-year figure should be relied upon to provide an assessment of a company’s performance.

What are some potential problems and limitations of financial ratio analysis? • Comparison with industry averages is difficult if the firm operates many different divisions. • “Average” performance is not necessarily good. • Seasonal factors can distort ratios. (More…)

Problems and Limitations (Continued) • Sometimes it is difficult to tell if a ratio value is “good” or “bad.” • Often, different ratios give different signals, so it is difficult to tell, on balance, whether a company is in a strong or weak financial condition.

Ratio Analysis Limitations Ratios are presented on a percentage basis Relative size is ignored (e.g., both large & small firms can be compared) It is assumed that all numbers used are correct (consider both possible errors and earnings management) If the numbers are not reliable, ratios are not particularly useful

Limitations of Financial Analysis • Business decisions are made in a world of uncertainty. • No single ratio or one-year figure should be relied upon to provide an assessment of a company’s performance.

Limitations of Ratio Analysis • A firm’s industry category is often difficult to identify • Published industry averages are only guidelines. Rarely are two companies exactly the same. • Accounting practices differ across firms • Sometimes difficult to interpret deviations in ratios • Industry ratios may not be desirable targets • Seasonality affects ratios

Analysts should understand the following aspects when dealing with ratios • A ratio is not "the answer". A ratio is an indicator of some aspect of a company's performance in the past. It does not reveal why things are as they are. Also a single ratio by itself is not likely to be very useful. • Differences in accounting policies can distort ratios (e.g. inventory valuation, depreciation methods). • Not all ratios are necessarily relevant to a particular analysis. Analysts should know the questions for which they want to find answers, and know the questions that particular ratios can help answer. • Ratio analysis does not stop with computation; • Interpretation of the result is vital

Continued • How homogeneous is the company? • Are the ratios comparable between divisions within a company? It is critical to derive comparable industry ratios. However, many companies have multiple lines of business, making it difficult to identify the appropriate industry to use in comparing companies. • Companies are required to provide segmented information that allows the user to see the impact of various segments on the overall company.

Continued • Are the results of the ratio analysis consistent? • An analyst needs to look at several ratios in conjunction in order to form a sensible conclusion. Total portfolio of the company should be used instead of only one set of ratios. • A company must be viewed along all these lines since the company may have strengths and/or weaknesses in different areas. For example, a highly profitable company may have very poor short-term liquidity.

Concerns • Is the ratio within a reasonable range for the industry? • Analysts must look at a range of values for a particular ratio because a ratio can be too high or too low.

Accounting Issues • Are alternative companies' accounting treatments comparable? • In comparing companies, even within the same industry, the companies may be using different accounting treatments and/or different estimates to capture the same event. • Companies could use different estimates to calculate depreciation or bad debts expense. Companies could use different inventory methods and may have operating versus capital leases in the financial statements. All of these accounting choices and estimates affect financial statements. • However with IFRS replacing every countries GAAP, the issue of distortion by accounting treatment should be minimised.

Looking Beyond The Numbers: • Good financial analysis involves more than just calculating numbers. • There are Qualitative factors to be considered when evaluating a company’s future financial performance. • These important and basic skills are necessary when making business decisions, when evaluating performance, and when forecasting likely future developments.

Ratio Analysis • Limitations of Ratio Analysis: • Usefulness dependent on the accuracy of the figures – Enron, WorldCom or Parmalat? • Only a part of the jig-saw – needs other information to make full judgement • What has happened in the past is not necessarily a pointer to what will happen in the future! • Statistics always have a limitation in that it depends when they are used and how they are used. • No two businesses are fully comparable as the differences between them will always influence the performance of the business • Ratios do not always reflect the degree of ‘intuition’/’genius’ that may influence the performance of a business The Crooked E – ironic logo of Enron. Statistics do have their limitations!

What are some qualitative factors analysts should consider when evaluating a company’s likely future financial performance? • Are the company’s revenues tied to a single customer? • To what extent are the company’s revenues tied to a single product? • To what extent does the company rely on a single supplier?

Looking Beyond The Numbers: • Are the firm’s revenues tied to One key customer, product, or supplier? • What percentage of the firm’s business is generated overseas? • Competition. • Future prospects. • Legal and regulatory environment.

Qualitative Issues • The sustainability of an enterprise is not just down to current profits. • Today's businesses need to care and respect the environment. • CSR and Corporate Governance are essential. • Investors are waking up this and understand that sustainability is key.