Download

1 / 55

550 likes | 786 Vues

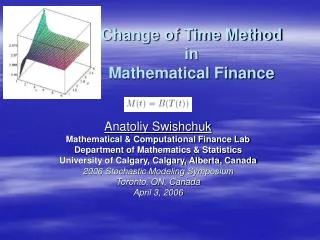

Paper Review: “On the Pricing and Hedging of Volatility Derivatives†by S. Howison, A. Rafailidis and H. Rasmussen (Applied Mathematical Finance J., 2004). Anatoliy Swishchuk Math & Comp Finance Lab Dept of Math & Stat, U of C “Lunch at the Lab†Talk February 10, 2006. Variance Swap.

E N D

Paper Review:“On the Pricing and Hedging of Volatility Derivatives”by S. Howison, A. Rafailidis and H. Rasmussen (Applied Mathematical Finance J., 2004) Anatoliy Swishchuk Math & Comp Finance Lab Dept of Math & Stat, U of C “Lunch at the Lab” Talk February 10, 2006

Three Approaches to the Risk-Neutral Pricing • Pricing Independently of the Volatility Model • Pricing by Expectations in a SV Framework • Pricing via Partial Differential Equations

1st Approach: Pricing Independently of the Volatility Model (cntd)

1st Approach: Pricing Independently of the Volatility Model (cntd)

2nd Approach: Pricing by Expectations in a SV Framework (cntd)

2nd Pricing Approach: Pricing by Expectations in a SV Framework (cntd)

2nd Pricing Approach: Pricing by Expectations in a SV Framework (cntd)

3d Approach: Pricing via PDE (PDE Itself for the Value V of Derivative)

![Study Strategies in Various Disciplines (Math) at St. Cloud [MN] State University](https://cdn3.slideserve.com/6787961/slide1-dt.jpg)