Download

1 / 27

290 likes | 464 Vues

Efficient and Effective Trade Services at Your Door Steps: Understanding Afreximbank’s African Correspondent Banking and Letter of Credit Confirmation Scheme (AFRICORRBANKING). By Mrs. Kanayo Awani Director (Trade Finance & Branches, Afreximbank).

E N D

Efficient and Effective Trade Services at Your Door Steps: Understanding Afreximbank’s African Correspondent Banking and Letter of Credit Confirmation Scheme (AFRICORRBANKING) By Mrs. Kanayo Awani Director (Trade Finance & Branches, Afreximbank) Presentation at Afreximbank Annual Structured Trade Finance Seminar Cairo, December 2, 2010

Table of Contents Partnership between Afreximbank and Africorrbanking Partners • Introduction Product outline Conclusion

Introduction 1. 1 Context: African banks face many challenges in providing import financing to their clients due to : • Inability of most African banks to build efficient correspondent banking relationships with international banks; • Few international banks are willing to offer significant correspondent banking lines to African banks due to country, regulatory and credit risks constraints; • Lines granted are at uncompetitive terms, including significant cash collateralization of “Nostro Accounts”, high pricing, and capricious withdrawal of services

1.1 (continued) • The consequence is that Africa faces high cost of trade finance; • Afreximbank (the “Bank”) was created to solve, among other problems, the unrelenting high cost of trade finance. Afreximbank’s ability to deal decisively with the problem is constrained by its non-presence in foreign markets where African businesses trade; and • The Bank's operations as a wholesale bank have also meant that it does not have adequate back-office arrangements to offer extensive correspondent banking services. Solution: Building Partnerships that enables the Bank to leverage its strengths while dealing with its weaknesses.

1.2 Correspondent Banking / African Letter of Credit Facility Under this Facility therefore, the Bank (a) offers correspondent banking services to African banks assisting them to make payments and collections around the world, and (b) offers dedicated Letter of Credit Confirmation Facility for promotion of intra- and Extra-African trade. This Facility is hinged on the extensive experience the Bank has gained across Africa through the use of African banks as Trade Finance Intermediaries (TFIs). Benefits are :reduced costs;improved correspondent banking relationships; andhigher intra-African trade possibilities

2. Africorrbanking Partners • Afreximbank is working with leading international banks – Africorrbanking Partners (APs) - that offer full banking services around the world especially in Europe and Asia. These are banks that are already entrenched in Africa (eg Standard Chartered Bank) or have taken a decision to expand and support their operation in Africa, eg Landesbank Baden Wűrttemberg (LBBW), Sumitomo Mitsui Banking Corporation (SMBC). • These banks have the skills and resources for offering sophisticated correspondent banking services around the globe. Based on extensive branch network and correspondent relationships, they are able to advise, confirm and negotiate L/Cs across major regions of the world.

2.1 (continued) • Afreximbank has an extensive network of African banks, called its Trade Finance Intermediaries (TFIs), through whom it delivers its trade finance services. Many of the TFIs are also the Bank’s Shareholders; • The Bank in many cases has years of credit experience with the TFIs; • Afreximbank and the Africorrbanking Partners combine their individual strengths in a co-branded product targeted at expanding access of African banks to correspondent banking services that are:

2.1 (continued) • tailored to specific bank’s needs; • efficient, reliable and flexible; • cost-effective; • Africa-friendly; and • that leverages on long-term relationships that Afreximbank has built with potential beneficiary banks.

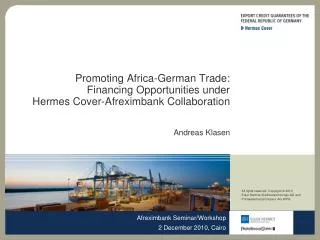

2.2 The Operating Model: The effectiveness and appeal of the co-branded product to the market depends on how the individual strengths of Afreximbank and Africorrbanking Partners are leveraged to offer an efficient and competitive service. The diagram below sets out the operating model and relationship between all parties in implementing the product. STRUCTURE Afreximbank establishes risk sharing partnership with international banks (APs), leveraging synergies between Afreximbank’s pan-African experience with international partner’s extensive correspondent network in OECD markets AfriCorrBanking partners pre-approve list of African banks to participate under the scheme Afreximbank Trade Finance Intermediary(TFI) applies for line of credit under the AfriCorrBanking scheme Line of credit is linked to importation of essential/capital goods & services AfriCorrBanking agent bank confirms/advises LC to exporters bank Afreximbank provides Reimbursement Guarantees to participating international banks to cover all or part of the pre-approved African banks risk. Commercial Contract LC application Exporter African Importer African Bank (TFI) TFI issues LC under AfriCorrBankingscheme Bank pays exporter [1] [5] LC Confirmation/ Refinancing Line of Credit with Africorrbankig Sponsoring banks [2] Exporters Bank LC confirmation/ refinancing Request LC Confirmation [4] [3] Confirming Facility Agents Afreximbank issues Irreceivable Reimbursement Guarantees to cover all or part of pre-approved African banks risk

2.3 Key Success Factors of the Partnership • Key success factors of the partnership include: • Origination: Afreximbank currently has about 71 Trade Finance Intermediaries (TFIs) spread across Africa. The TFIs are based in countries that have granted the Bank preferred creditor status. Their economies also have acceptable clearing and settlement systems, as well as acceptable communication facilities and automation standards. There are therefore satisfactory initial conditions for the product; • A strong Network: Correspondent banking is all about reaching as far out as possible to the largest number of clientele and with the maximum geographical coverage. Our APs have extensive reach through their network of branches and correspondents that will make it possible to reach key African trading partners around the world;

2.3 Key Factors of Success (continued) • Automation: Correspondent banking is a retail-based service which profitability depends on volumes. In choosing Africorrbanking, clients will evaluate reliability, speed and quality of service. To be able to balance these requirements i.e. volume, speed, quality of service, etc, Africorrbanking partners need to have a well developed and tested automated system that can achieve this balance with minimal human interference. Our selected partners have systems considered sufficiently sound and robust for an efficient correspondent banking offering; and • Human Resources: As indicated above, correspondent banking is primarily a retail-based service involving large volumes that tend to be administration intensive, even in the presence of a strong automated system. Thus, sufficient support staffing - usually lower skilled - is required to be able to provide a good and reliable service. The resources are available and sufficient within the partnership.

2.3 Key Factors of Success (Continued) • Due Diligence: Correspondent banking is a high risk business that requires careful evaluation of counterparty risk. It has also become a prime regulatory concern for potential money laundering activities. Afreximbank and APs have robust Customer Due Diligence (CDD) procedures that mitigates this risk. In addition, the banks admitted to the scheme are those with whom Afreximbank has had a minimum of 3 years satisfactory relationship.

3. Product Features 3.1 Product Name: This African Correspondent Banking and Letter of Credit Confirmation Services is branded “AFRICORRBANKING” for ease of reference and as a marketing tool. The brand name is meant to convey the message that the product touches the core of correspondent banking needs of African banks. 3.2 Service Offering: Africorrbanking offers a comprehensive suite of correspondent banking services, namely: 3.2.1 Trade Services: These include: • Letters of Credit Advising; • Letters of Credit Opening and/or confirmation

3.2.1Trade Services (continued) • Bills negotiation for Discounting /Acceptance; • LC reimbursement; • Documentary bills for collection; • Guarantees; and • Standby Letters of Credit.

3.2.2 Treasury: The range of products include: • Foreign exchange quotations (spot, forwards, and swaps); • Foreign currency hedging solutions; • Money Market lines for investment and short-term borrowing needs; and • Other liquidity and risk management solutions.

3.2.3 Retail: The services on offer under Retail Services include: • Current, Demand and other account types; • Check Collections and Clearing, including Cash Letter Services; and • Wire Transfers and other payment forms, especially access to international funds transfer systems such as SWIFT, CHIPS and Fedwire.

3.2.4 Other Services: These are ancillary services that can be offered to banks which makes Africorrbanking a one-stop shop for their international banking needs. They include: • Advisory Services; • Arranging Syndications; • Structured Trade Finance; • Country Risk Guarantee Facility; and • Factoring.

3.3 Eligibility Criteria: Participating banks (the “ Participating Banks ” ) are: 3.3.1 banks based in Afreximbank member countries acceptable to APs; and 3.3.2 African-owned banks in the Diaspora. 3.3.3 In addition, Participating Banks must be: • banks with whom Afreximbank has had a minimum of 3 years satisfactory experience, unless specifically waived by the Bank and Africorrbanking Partners; and • banks that meet the credit, including CDD, criteria of Afreximbank and APs, it being understood that where only one of the Partners is taking the full risk of the transaction then the bank in question must meet the credit criteria of the partner assuming the full risk. In all cases CDD must be satisfactory to Afreximbank and Africorrbanking Partners.

3. 4 Eligible Transactions: The following transactions are eligible for support under Africorrbanking; • All eligible exports of Afreximbank Participating States acceptable to Africorrbanking Partners (“Africorr Eligible States” or “AES”); • All eligible imports of AES, that is, export-generating African imports, including raw materials, equipment, spare parts and other essential items; • Intra-African trade in Eligible Items; • South-South trade in Eligible Items; and • All Eligible imports of Non-Participating States from AES.

3.5 Eligible Items: Africorrbanking supports transactions in all traded goods and services except; • Armaments, ammunition and other military equipment; • Psychotropic drugs or narcotics; • All items for which international trade is prohibited for environmental reasons or by international conventions; and • Pornographic and obscene materials. In addition, Africorrbanking Partners will respect the trade policies of AES and will thus have country specific negative lists, corresponding to items which are prohibited for international trade in AES.

3. 6 Limits and Financing Margin: • The maximum limit per Participating Bank is 60% of its shareholders’ funds; and • Unless specifically waived by Africorrbanking Partners, all L/Cs to be confirmed, acceptances, etc. are subject to a cash collateral of a minimum of 15% of the transaction amount. Other marketable liquid assets may be a substitute for the cash collateral.

3.7 Pricing and Sharing of Revenues: • Pricing and charges are market conform and will from time to time be agreed by Afreximbank and APs who will periodically publish Africorrbanking Pricing Schedules; and • Afreximbank and APs will agree how to share income for services to be rendered under Africorrbanking.

3.8 Marketing and Implementation Arrangement: • Afreximbank and APs sign a Co-branding Agreement to which a Master Risk Participation Agreement that provides the legal framework for implementing the product is annexed; • Afreximbank and APs market the Product through their respective websites as well as print marketing brochures for its marketing; • Each of Afreximbank and APs designate one officer as the Africorrbanking contact person who implements a marketing plan for the product, including developing a schedule for making joint marketing calls to prospective clients; and • APs and Afreximbank jointly develop implementation tools, such as a Standardized Application Form, appropriate communication tools and channels, etc.

3.9 Documentation 3.9.1 Afreximbank and APs will enter into: • a Co-branding Agreement; • a Master Risk Participation Agreement to be annexed to the Co-branding Agreement; and • Revenue Sharing Agreement.

3.9 (Continued) 3.9.2 Participating Banks will enter the following Agreements with Africorrbanking Partners: • Framework Africorrbanking Participation Agreement under which an Uncommitted Credit Limit will be granted to the relevant Participating Bank; and • Specific agreements relevant to specific services that may be offered to the Participating Banks.

CONCLUSION • Although the scheme was developed with a few pilot APs, Afreximbank is working at developing partnerships with other commercial banks with Pan African focus (such as UBA, Ecobank etc) to develop correspondent banking and payment solutions for Intra-Africa Trade. • Pulling together our strengths, we are then able to deliver similar solutions for Intra-Africa Trade. • We will welcome meetings and discussions after the event to expand this roadmap.

Thank You For Listening African Export-Import Bank December, 2010