Download

1 / 54

1.04k likes | 2.76k Vues

Standard Costing and Variance Analysis. Operation of a Standard Costing System Setting of Standards Definition of Standard Cost Types of Standard Costs Standard Cost Setting and Learning Curve Advantages of Standard Costing System. Standard Costing and Variance (cont.).

E N D

Standard Costing and Variance Analysis Operation of a Standard Costing System Setting of Standards Definition of Standard Cost Types of Standard Costs Standard Cost Setting and Learning Curve Advantages of Standard Costing System

Standard Costing and Variance (cont.) • Basic Variance Analysis • Advanced Variance Analysis • Planning and Implementation of Variance Analysis • Operating Statement • Variance Investigation • Limitations of Variance Analysis

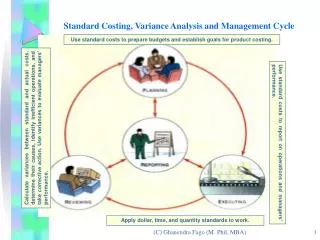

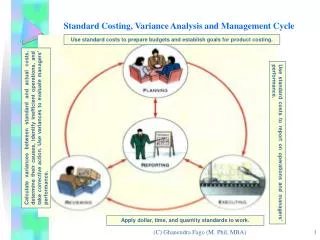

Operation of a Standard Costing System • Most suited to a series of common or repetitive organisation • Variances are traced to responsibility centres (not products) • Actual costs are not required • Comparisons after the event provide information for corrective action or highlight the need to revise the standards

Standard cost of actual output recorded for each responsibility Actual costs traced to each responsibility centre Standard and actual costs compared And variance analysed and reported Variance investigated and Corrective action taken Standards monitored and adjusted to reflect changes in std usage and /or prices

Variance allocated to responsibility centres (RC) • Different RC responsible for each operation • Cost control requires that RCs be identified with the std cost for the output achieved • For effective control only compare total actual costs with the total std cost for each operation or RC

Detailed analysis of variances • Report a detailed analysis of variances • Variances for each RC can be identified for each element of cost and analysed according to price and quantity • Accountant role: assist managers to pinpoint where variances have arisen and investigate reasons for the variances

Definition of Standard Cost • Target costs for each operation that can be use built up to produce a product standard cost

Cost Assignment Approaches Direct Direct MaterialsLaborOverhead • Actual costing Actual Actual Actual • Normal costing Actual Actual Budgeted • Standard costing Standard Standard Standard Manufacturing Costs

Standard Costs • Standard costs are benchmarks based on standards established in advance for (1) the quantity of resources that should be consumed by each product or other unit of output and (2) the price of these resources • The unit standard cost for a particular input = standard price x standard quantity

Standard costs • Standard costs are benchmarks based on standards established in advance for (1) the quantity of resources that should be consumed by each product or other unit of output and (2) the price of these resources • The unit standard cost for a particular input = standard price x standard quantity

Standard Costs vs Budgeted Costs • Standard cost are predetermined costs; they are target costs that should be incurred under efficient operating conditions • Not the same as budgeted costs. A budget relates to an entire activity /operation. • A standard provides same information on a per unit basis.

Standard costs vs Budgeted Costs • Standard relates to a cost per unit of activity • Budget relates to the cost for total activity

Purposes of Standard Costing • To provide a prediction of future costs that can be used for decision making • To provide a challenging target that an individuals are motivated to achieve • To assist in setting budgets and evaluating performance • To act as a control device by highlighting those activities • To simplify the task of tracing costs to products for inventory valuation

Establishing Standards • Need to establish price and quantity standards for inputs (direct materials, direct labour and overhead) • Potential sources of quantitative standards include historical experience, engineering studies and input from operating personnel

Establishing standards (cont.) • Historical experience should be used with caution because it may perpetuate operating inefficiencies • Engineering studies and input from operating personnel help determine the most efficient level of input quantities • the use of an engineering study approach by itself may produce standards that are too rigorous

Responsibilities for establishing standard prices • Operation managers determine the quality of the inputs required • Personnel and purchasing have the responsibility to acquire the input quality at the lowest price that is limited by the market forces and trade union • Note: purchasing must consider discounts, freights and quality, personnel must consider payroll tax, fringe benefits and qualifications • Accounting is responsible for recording the price standards and for preparing reports

Standard Cost Sheet A listing of the standard costs and standard quantities of direct material, direct labour and overhead that should apply to a single product

Types of Standards • Ideal standards • Standard that demand maximum efficiency • Can be achieved only if everything operates perfectly • Basic cost standards • (constant standards that are left unchanged for a long time) • Advantage: efficiency can be established

Types of Standards (cont..) • Currently attainable standard • Can be achieved under efficient operating conditions • Allowance made for normal breakdowns, interruptions • Kaizen standard • Continuous improvement standard • Reflect planned improvement • Type of currently attainable standard with a cost reduction focus

Types of Standard Costs • Ideal standards demand maximum efficiency and can be achieved only if everything operates perfectly. • Currently attainable standards can be achieved under efficient operating conditions. • Kaizen standardsreflect a planned improvement and are a type of currently attainable standard.

Standard Cost Setting and Learning Curve Theory • Learning curve effect should be take into account in estimating labour costs for relatively new products or production processes • As cumulative production output increases, the average labour time required per unit declines • A nonlinear curve that show how the labour hours decrease as the volume produced increases • Learning rate expressed as percent, gives the percentage of time needed to make the next unit, based on the time it took to make the previous unit

Basic Variance Analysis • Direct Material Variance • Material Price Variance • Material Quantity Variance • Direct Labour Cost Variance • Labour Rate Variance • Labour Efficiency Variance • Variable Overhead Variance • Fixed Overhead Variance

Direct Material Variance • Total direct material cost variance =SC – AC • (SP x SQ) – (AP x AC) • Price Variance • Quantity (Usage ) Variance

Direct material price variance • Formula: (SP – AP) AQ • AQ = actual quantity purchased • The material price variance should be recorded at the time materials are purchased. This permits: • Early recognition of the variance • Carrying materials in inventory at standard cost

Material Price Variance • May not always indicate the efficiency of purchasing department • Possible causes: • a change in market condition causing a general price increase for the type of material used • failure by the purchasing department to seek the most advantageous sources of supply • purchase of inferior quality materials which may lead to inferior product quality or more wastage • Other department may be responsible for all or part of price variance

Direct material quantity variance • Formula: (SQ – AQ) SP • Normally controllable by the manager of the appropriate production responsibility centre • Common causes include: • careless handling of materials • purchase of inferior quality materials • pilferage • changes in quality control requirements • changes in method of production

Direct Labour Variance • Direct Labour Rate Variance • Direct Labour Efficiency Variance

Direct Labour Rate Variance • Formula: (SR – AR) AH • Least subject to control by management • Possible causes • Due to a negotiated increase in wage rates not yet having been reflected in the standard wage rate • A standard is used that represents a single average rate for a given operation performed by workers who are paid at several different rates

Direct Labour Efficiency Variance • Formula: SR (AH – SH) • Normally controllable by the manager of the appropriate production responsibility centre • Possible causes: • Use of inferior quality materials • Different grades of labour • failure to maintain machinery • The introduction of new equipment • Changes in the production processes, poor production scheduling

Variable Overhead Variance • Variable Overhead Spending Variance • Variable Overhead Efficiency Variance

Variable Overhead Variance • Total Variable Overhead Variance is the difference between the standard variable overhead charged to production and the actual variable overhead incurred • Overhead Spending Variance • Formula: AH (AR – SR) • Overhead Efficiency Variance • Formula: SR (AH – SH)

Variable overhead spending Variance • Need to compare actual expenditure for each individual item of variable overhead expenditure against the budget • Variable overhead expenditure variance is equal to the difference between the budgeted flexed variable for the actual direct labours hours of input (BFVO) and the actual variable overhead costs incurred(AVO)

Variable overhead efficiency Variance • Arise because more or less of input (direct labour hours) were required for actual production • Variable overhead efficiency variance is the difference between the standard hours of output (SH) and the actual hours of input (AH) multiplied by the standard variable overhead rate

Fixed Overhead Variance • Total fixed overhead variance • Fixed overhead expenditure variance • Volume variance

Advanced Variance Analysis • Mixed variance • Yield variance • Sales variance

Mix variance • Variance will occur if its is possible to substitute one DN input for another or one type of DL for another • A mix variance results whenever the actual mix of input differs from the standard mix

Mix Variance • Direct material mix variance is the difference between the standard cost of the actual mix of inputs and the stand cost of the mix of inputs that should have been used • (AQ – SM) SP • SM = std mix proportion x Total actual input quantity • Std mix qty (SM) is the quantity of each input that should have been used given the total actual input quantity

Mix and Yield Variance • For direct materials the sum of the mix and yield variances equals the material usage variance • For direct labour, the sum is the labour efficiency variance

Yield Variance • A yield variance results whenever tha actual yield (output) differs from the standard yield • DM yield variance is the difference between the std cost of the actual yield of output units and the std cost of the yield of output that should have been produced

Mix and Yield Variances:Materials and Labor Standard Mix Information: Direct Materials Direct Material Mix Mix Proportion SP Standard Cost Peanuts 128 lbs. 0.80 $0.50 $64 Almonds 32 lbs. 0.20 1.00 32 Total 160 lbs. $96 Yield 120 lbs. Yield ratio: 0.75 (1.20/160) Standard cost of yield (SP): $0.80 per pound ($96/120 pounds of yield)

Mix and Yield Variances:Materials and Labor Malcom Nut Company produces a batch of 1,600 pounds and produces the following actual results: Direct Material Actual Mix Percentages Peanuts 1,120 lbs. 70 % Almonds 480 30 Total 1,600 lbs. 100 % Yield 1,300 lbs. 81.3 %

Mix and Yield Variances:Materials and Labor Direct Materials Yield Variance Yield variance= (Standard yield – Actual yield) SPy Standard yield = Yield ratio x Total actual inputs Yield variance= (1,200 – 1,300)$0.80 = $80 F

Mix and Yield Variances:Materials and Labor Standard Mix Information Labor TypeMixMix ProportionSPStandard Cost Shelling 3 hrs. 0.60 $ 8.00 $24 Mixing 2 hrs. 0.40 15.00 30 Total 5 hrs. $54 Yield 120 lbs. Yield ratio: 24 = (120/5), or 2,400% Standard cost of yield (SPy ): $0.45 per pound ($54/120 pounds of yield)

Mix and Yield Variances:Materials and Labor Shelling 20 hrs. 40% Mixing 30 hrs. 60% Total 50 hrs. 100% Yield 1,300 lbs. 2,600% *Uses 50 hours as the base. Direct Labor Type Actual Mix Percentages*

Direct Labor Yield Variance Yield variance = (Standard yield – Actual yield)SPy = [(24 x 50) – 1,300]$0.45 = (1,200 – 1,300)$0.45 = $45 F Mix and Yield Variances:Materials and Labor Direct Labor Mix Variance Direct Labor AH SM AH – SM SP (AH – SM)/SP type Shelling 20 30 -10 8.00 $-80 Mixing 30 20 10 15.00 150 Direct Labor mix variance $-70 U

Direct Labor Yield Variance Yield variance = (Standard yield – Actual yield)SPy = [(24 x 50) – 1,300]$0.45 = (1,200 – 1,300)$0.45 = $45 F Mix and Yield Variances:Materials and Labor Direct Labor Mix Variance Direct Labor Type AH SM AH – SM SP AH – SM)/SP Shelling 20 30 -10 RM 8.00 RM-80 Mixing 30 20 10 15.00 150 Direct Labor mix variance -70 U

Sales variance • Two possible causes in sales variance • Sales price different from budgeted price • Sales volume different from budgeted volume • Sales price variance • Formula : AV (ASP – SSP) • Sales margin variance • Formula: SP (AV – BV)