Standard Costing, Variance Analysis and Management Cycle

330 likes | 884 Vues

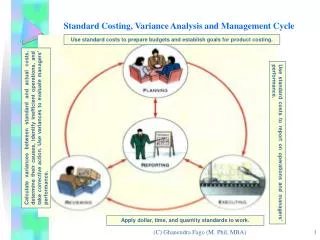

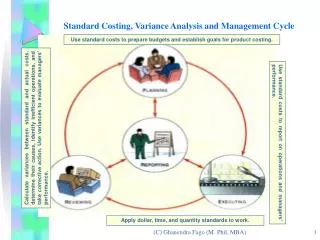

Use standard costs to prepare budgets and establish goals for product costing. Calculate variances between standard and actual costs, determine their causes, identify inefficient operations, and take corrective action. Use variances to evaluate managers’ performance. .

Standard Costing, Variance Analysis and Management Cycle

E N D

Presentation Transcript

Use standard costs to prepare budgets and establish goals for product costing. Calculate variances between standard and actual costs, determine their causes, identify inefficient operations, and take corrective action. Use variances to evaluate managers’ performance. Use standard costs to report on operations and managers’ performance. Apply dollar, time, and quantity standards to work. Standard Costing, Variance Analysis and Management Cycle (C) Ghanendra Fago (M. Phil, MBA)

Standard Costs • Standard costs are predetermined costs that are developed from analyses of both: • a. Past operating costs, quantities, and times • b. Future costs and operating conditions. • In a standard costing system, standard costs for direct materials, direct labor, and manufacturing overhead flow through the inventory accounts and eventually into the Cost of Goods Sold account. (C) Ghanendra Fago (M. Phil, MBA)

The Management Cycle Managers use standard costs throughout the management cycle: • In the planning stage of the management cycle, standard costs aid in the development of budgets. • During the executing stage, standard costs, quantities, and time are applied to work performed. • During the reviewing stage, actual costs are compared with standard costs to compute variances, and managers analyze the causes of those variances to improve operations. • During the reporting stage, a variance report provides information on operations and managerial performance (C) Ghanendra Fago (M. Phil, MBA)

The Management Cycle In today’s globally competitive environment, new standards or measurements are necessary to help managers: • Reduce processing time. • Improve quality. • Improve customer satisfaction. • Improve on-time deliveries (C) Ghanendra Fago (M. Phil, MBA)

Standard Costs • Standard costs are used with existing job order or process costing systems. • Standard costs are usually expressed as the cost per unit of a finished product or process. • Standard costs are based on: • Engineering estimates. • Forecasted demand. • Worker input. • Time and motion studies. • Type and quality of direct materials (C) Ghanendra Fago (M. Phil, MBA)

Standard Costing • The technique for application of standard cost is known as Standard Costing. It is the preparation of standard cost and applying them to measure the variation between standard cost and actual cost. • The preparation of standard costs of products and service and a technique whereby the planned activities of an undertaking are expressed in budgets, standard costs, standard selling price and standard profit margins, and the differences between these and the comparable actual results are accounted for.’ • Standard costing is expensive to use because the management accounting system must keep separate records of actual costs to compare with what should have been spent. (C) Ghanendra Fago (M. Phil, MBA)

Standard costing may be summarized as • To fix the standard cost for material, labour and overhead. • To find out the actual cost • To compare the actual cost with standard cost • To analyse the variance between standard cost and actual cost (C) Ghanendra Fago (M. Phil, MBA)

Preparing operating budgets. • Identifying production costs and processes that must be managed to reduce waste and inefficiency. • Evaluating the performance of managers and workers. • Setting prices. • Simplifying inventory and product costing procedures Use of Standard Costs (C) Ghanendra Fago (M. Phil, MBA)

Standard Cost per Unit • There are six standards used to determine the standard cost per unit: • Direct materials price standard • 2. Direct materials quantity standard • 3. Direct labor time standard • 4. Direct labor rate standard • 5. Standard variable manufacturing overhead rate • 6. Standard fixed manufacturing overhead rate (C) Ghanendra Fago (M. Phil, MBA)

Direct Materials Price Standard The direct materials price standard is found by carefully considering: • Expected price increases • Changes in available quantities. • Possible new sources of supply. Direct Materials Quantity Standard The direct materials quantity standard is affected by: • Product engineering specifications. • Quality of direct materials. • Age and productivity of machines. • Quality and experience of the work force. (C) Ghanendra Fago (M. Phil, MBA)

Direct Labor Time Standard The direct labor time standard is based on current time and motion studies of workers and machines and past performance. Direct Labor Rate Standard The direct labor rate standards are affected by labor union contracts and company personnel policies. (C) Ghanendra Fago (M. Phil, MBA)

Standard Direct Materials, Standard Direct Labor Costs Manufacturing Overhead Costs Standard Direct Materials Cost = Direct Materials Price Standard X Direct Materials Quantity Standard Standard Direct Labor Cost = Direct Labor Time Standard X Direct Labor Rate Standard Standard Manufacturing Overhead Cost = (Standard Variable Overhead Rate +Standard Fixed Overhead Rate) X Application Basis (C) Ghanendra Fago (M. Phil, MBA)

Standard Rates Standard Variable Manufacturing Overhead Rate = Total budgeted variable manufacturing overhead costs ÷ Expected number of standard machine hours Standard Fixed Manufacturing Overhead Rate = Total budgeted fixed manufacturing overhead costs ÷Normal capacity in terms of standard machine hours (C) Ghanendra Fago (M. Phil, MBA)

Standard Unit Cost • A product’s standard unit cost is determined by adding standard direct materials cost, standard direct labor cost and standard manufacturing overhead rate. (C) Ghanendra Fago (M. Phil, MBA)

Four Step Approach of Variance Analysis • Compute the variance. If the variance is insignificant, actual operating results are close to or equal to anticipated operation conditions, no corrective action is needed. • Determine the cause of any significant variance. • Identify the performance measures that track those activities. • Take action to correct the problem or continue to improve operations. (C) Ghanendra Fago (M. Phil, MBA)

No Is the Variance Material Significant? No Corrective Action Needed Yes Determine Cause(s) of Variance Identify and Analyze Performance Measures to Determine Corrective Action Take Corrective Action Using Variance Analysis to Control Costs Compute Variance (C) Ghanendra Fago (M. Phil, MBA)

Material Variance Analysis • The term variance refers to the deviation of the actual cost from the standard cost due to the various causes. • Variances will occur if in any given production period the actual costs vary from the standard costs. • "Cost variance is the difference between the standard cost and the comparable actual cost incurred during a given period“ : ICMA • For example, if the price paid for material bought during a given production period, differed from the standard (expected) price for that material, a material price variance will arise. • Similarly if the amount of material actually used exceeded the standard (expected) usage a material usage variance will arise. (C) Ghanendra Fago (M. Phil, MBA)

Material Cost Variance The difference between material at the standard material price and actual material price is known as material usage variance. The variance can be favorable or unfavorable .If the actual cost is lower than the standard cost, it is considered as a favorable variance and if the actual cost exceeds the standard cost the difference is deemed to be unfavorable. • Material Cost Variance (MCV): • = SQSP–AQAP = (SQ*SP)-(AQ*AP) = ((SQ/SO*AO)*SP)-(AQ*AP) (C) Ghanendra Fago (M. Phil, MBA)

Material Price Variance (MPV) • Material price variance is the deviation of the actual price paid from the standard price specified. Formula: • Material Price Variance (MPV)= AQ (SP–AP) (C) Ghanendra Fago (M. Phil, MBA)

Possible Causes of Direct Materials Price Variance • Changes in vendor prices, inaccurate or outdated direct materials price standards, and differences between the quality of direct materials purchased and the quality desired. • Differences between quantity discounts received and those anticipated. • The purchase of substitute direct materials that differ from product specifications. (C) Ghanendra Fago (M. Phil, MBA)

Material Usage Variance (MUV) • It indicates the difference between the standard quantities of the material specified from the actual quantity of output and actual quantities of material used .The material usage variance can be calculated by multiplying the difference between the actual quantity and standard quantity by standard price. Formula: • Material Usage Variance (MUV) = SP*(SQ-AQ) (C) Ghanendra Fago (M. Phil, MBA)

Material Mix Variance (MMV) The material mix variance is the result of the deviation of the actual composition of a mixture of the material from the standard one. Normally, a material mix variance arises where there is the change in the composition of the material mixture Formula: Material Mix Variance (MMV) = (Total Weight of AM/Total weight of SM)(SC of SM)–SC of AM (C) Ghanendra Fago (M. Phil, MBA)

Possible causes of a direct materials quantity variance • Inaccurate or outdated direct materials quantity standards • Poor workmanship or excellent workmanship • Faulty equipment • Inferior or superior quality of direct materials • Poor materials handling (C) Ghanendra Fago (M. Phil, MBA)

Material Yield Variance (MYV) • The difference between the standard yield output) specified and actual yield (output) obtained • This variance is based on the output of the product • The standard loss during its processing is expected to be 15%. Formula: Material yield variance (MYV): (Actual yield or output-Standard yield or output for actual input)*Standard cost per unit = SC/SO (Actual Yield –standard Yield) (C) Ghanendra Fago (M. Phil, MBA)

VERIFICATION Material Cost Variance (MCV) Material Usage Variance (MUV) Material Price Variance (MPV) Material Yield Variance (MYV) Material Mix Variance (MMV) (C) Ghanendra Fago (M. Phil, MBA)

Direct Cost Variance (LCV) • Is the difference between the standard direct labor cost for the actual output and the actual labor cost paid. • The deviation of the actual direct wages paid from the direct wages specified for the standard output. Formula: • Labour Cost Variance (LCV) = ST SR – AT A = ((ST/SO AO)*SR) -(AT AR) (C) Ghanendra Fago (M. Phil, MBA)

Labor Rate (wage) Variance • Difference between standard wage rate per hour/day/week/month/fixed and actual wage rate paid. • It is usually caused due to increases in wage rate because of negotiation with the union or other causes. • Labour Rate Variance = AT (SR – AR) Causes of Direct Labor Rate Variance • A worker is hired at a pay rate that is higher or lower than expected. • An employee performed the duties of a higher- or lower-paid position. (C) Ghanendra Fago (M. Phil, MBA)

Labor Efficiency Variance (LEV) • “Have the workers performed as efficiently as they were expected to perform”? • It compares the quantity of work achieved in the time paid for, with the production that should have been achieved in that time if the labor force had worked according to standard timings. Labour Efficiency Variance (LEV) = SR (ST – AT) Causes of Direct Labor Efficiency Variance • Overall wage rates changed due to New labor agreements, labor strikes that cause the temporary hiring of unskilled help, large layouts that result in unusual usage of remaining workers etc. (C) Ghanendra Fago (M. Phil, MBA)

Favorable Direct Labor Efficiency Variance A favorable direct labor efficiency variance can be caused by improved training of employees, new machinery and higher quality of materials. Unfavorable Direct Labor Efficiency Variance An unfavorable direct labor efficiency variance can be caused by machine breakdowns, inferior direct materials, poor supervision, slow materials handling, and poor employee performance (C) Ghanendra Fago (M. Phil, MBA)

Labor Mix Variance (MMV) • It is possible when more than one type of labor is used for the job. • It represents the variance due to the change in standard and actual labor force composition. Labour Mix Variance (LMV) = (Total AT Mix/Total ST Mix)– SC of AM (C) Ghanendra Fago (M. Phil, MBA)

Labor Yield Variance (LYV) • It represents that portion of labor efficiency variance which is due to difference between the standard output and the actual output. • If the actual labor output is higher as compare to the relative standard, then variance would be favorable and vice versa Labour Yield Variance (LYV)= SR (Actual Yield or Output – Standard Yield for Actual Input i.e. Time) (C) Ghanendra Fago (M. Phil, MBA)

Labor Idle Time Variance (LITV) • Sub efficiency variance. • Indicates the standard cost of the actual hours for which the employees may remain idle due to abnormal circumstances like strikes, lockouts, power failure, breakdown of machinery, unavailability or raw materials etc. • Always unfavorable. • For the accurate of the labor efficiency variance labor, idle time should be adjusted. • Labour Idle Time Variance = Idle Time SR (U) (C) Ghanendra Fago (M. Phil, MBA)

VERIFICATION Labour Cost Variance (LCV) Labour Efficiency Variance (LEV) Labour Idle Time Variance (LITV) Labour Rate Variance (LRV) Labour Yield Variance (LYV) Labour Mix Variance (LMV) (C) Ghanendra Fago (M. Phil, MBA)