Download

1 / 23

230 likes | 404 Vues

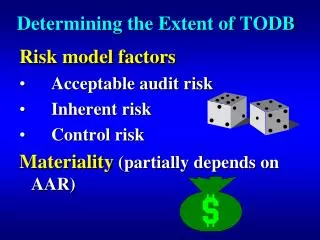

Determining the Extent of TODB. Risk model factors Acceptable audit risk Inherent risk Control risk Materiality (partially depends on AAR). Determining the Extent of TODB. Risk model factors Materiality Results of other tests Tests of controls Substantive tests of transactions

E N D

Determining the Extent of TODB • Risk model factors • Acceptable audit risk • Inherent risk • Control risk • Materiality(partially depends on AAR)

Determining the Extent of TODB • Risk model factors • Materiality • Results of other tests • Tests of controls • Substantive tests of transactions • Analytical procedures

Analytical Procedures • 2007 Gross 2006 Gross • Margin Margin • GW IND GW IND • Hardwood 36.3 32.4 36.4 32.5 • Softwood23.9 22.0 20.3 22.1 • Plywood 40.3 50.1 44.2 54.3

Analytical Procedures • Softwood increased 3.9%, industry stable • Changes usually most informative(also want to understand differences from industry) • Easier to spot errors in disaggregated data

Analytical Procedure Follow-up • Client will be able to suggest likely non-error causes, which you will evaluate. • Consider error causes • What errors would cause gross profit to increase?

Error Causes of Gross Profit Increase • Sales overstated • Fictitious sales • Cutoff error - January sale recorded in December (COS not matched) • Cost of sales understated • Inventory overstated • Purchases understated or cutoff error - December purchase recorded in January

Extent of Tests • Amount of testing for TODB objectives will depend upon results of TOT for related transaction objectives: • see following slide for related objectives (from Ch. 6) • see table in notes for specific tests • main sampling application in TODB for AR is confirmations

Assertion Trans. Obj. Balance Obj. • ExistenceOccurrence Existence • Completeness Completeness Completeness • Accuracy Accuracy • Valuation Classific. Classific. • or Timing Cutoff • Allocation Post. & Summ. Detail tie-in • None NRV • Rights & Obl. N/A Rights & Obl. • Pres. & Disc. N/A Pres. & Discl

Confirmations • Key Objectives • existence • accuracy (valuation) • Weak evidence for completeness - why?

Confirmation are required unless (SAS # 67): • Accounts receivable are immaterial. • Confirmations are expected to be ineffective. • Combined IR and CR are low, and other evidence reduces audit risk to an acceptably low level.

Confirmations • Why would auditors like to minimize confirmations? • What is the alternative to confirmations?

Positive Confirmations • Emphasis in testing is usually larger, and older accounts • Testing may be balance or individual invoice • Invoice may increase response rate • Reduces extent of reconciling items • However, provides less assurance

Negative Confirmations • Used when • Internal control effective • Many small balances • Customers expected to give adequate consideration

Alternative Procedures • 1. Subsequent cash receipts • 2. Shipping document • Any untested portion should be treated as an error for projection purposes.

95% of returned confirmations indicated the customer owed a smaller balance. This may be explained by: • a. Cash receipts journal was held open after • year-end. • b. There are a large number of unrecorded • liabilities. • c. Sales journal was closed prior to y/e. • d. Sales journal was held open after year- • end.

Aged Trial Balance for Hillsburg Hardware Co. • FIGURE 16 - 3

Analysis of Allowance for Uncollectible Accounts for Hillsburg Hardware Co. • FIGURE 16 -4

Estimated Estimated • Age Percentage Percentage • (days) Amount Uncollectible Uncollectible • Less than • 30 14,217,156 3 426,515 • 31-60 2,869,366 6 172,162 • 61-90 1,408,642 15 211,296 • 91-120 1,038,926 25 259,732 • > than • 120 662,710 40 265,084 • Totals 20,196,800 1,334,789

Auditing Allowance • Beginning Balance from prior year • Less: write-offs tested • Plus: current provision • (bad debt expense) residual • Ending balance tested TODB

Cutoff Testing • Sales Cutoff - Primary focus is on sales recorded just beforeyear-end • Cash receipts cutoff -Primary focus is on receipts recorded beforeyear-end • Purchases Cutoff -Primary focus is on purchases recorded afteryear-end • ( does not affect A/R)

Sales Cutoff Errors • Key issue is whether COS is matched. Determining factor is whether good are included or excluded from inventory. • Y/E physical - inventory normally correct

Sales Cutoff Errors • Shipped 1/2 Sale - $10,000 • Recorded 12/31 COS - $7,000 • Counted in Income Effect • inventory? of Error___ • Yes $10,000 • No $3,000

Cutoff Adjustments • Error 1 - inventory correct • Sales 10,000 • Accounts receivable 10,000 • Error 2 - inventory not correct • Sales 10,000 • Inventory 7,000 • Accounts receivable 10,000 • Cost of sales 7,000