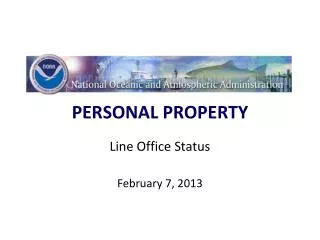

PERSONAL PROPERTY

PERSONAL PROPERTY. Line Office Status February 7, 2013. AGENDA. PMO CALENDAR BUBBLE CHART – DEPARTMENT OF COMMERCE OPEN CWIP PROJECTS CAPITALIZED ASSETS AWAITING LINE OFFICE ACTION CAPITALIZED ASSETS TO BE DISPOSED CAPITALIZED ASSETS TO BE ADDED IN SUNFLOWER LEASED ASSETS

PERSONAL PROPERTY

E N D

Presentation Transcript

PERSONAL PROPERTY Line Office Status February 7, 2013

AGENDA • PMO CALENDAR • BUBBLE CHART – DEPARTMENT OF COMMERCE • OPEN CWIP PROJECTS • CAPITALIZED ASSETS AWAITING LINE OFFICE ACTION • CAPITALIZED ASSETS TO BE DISPOSED • CAPITALIZED ASSETS TO BE ADDED IN SUNFLOWER • LEASED ASSETS • QUALITY CONTROL REVIEW ERRORS FOR ACCOUNTABLE PROPERTY • GSA LEASED VEHICLES • FY 2014 PHYSICAL INVENTORY – 1st QTR • BOR AND SBOR • UPR UPDATES • REMINDERS

PMO Calendar • PMO calendars are available at http://www.pps.noaa.gov/calendars/.

PMO Calendar PMO calendars are available at http://www.pps.noaa.gov/calendars/.

Open CWIP Projects That Have Outstanding UDO and/or CWIP Cost

Aged UPR as of 1/15/13 UPR transactions with age category of 0-30, and 61-90 days need improvement, when comparing 1/15/14 and 12/09/13 data. ** UPR transactions over 45+ days need improvement, per NOAA policy for timely reporting. **

FY 2014 UPRNumber of Records * Data unavailable due to government furlough

FY 2014 UPRDollar Value Amounts are in thousands * Data unavailable due to government furlough

Reminder • Financial Cut-Off Dates: 2/13/14 (February) • All Capitalized Disposals must have a signed Congressional Notification memo from the line office before the final event can be processed. A Congressional Notification must be provided to Congress at least 15 days in advance for Acquisition or Disposal of “any” capitalized assets $200K. • Due to Warehouse Closure, Line and Staff Offices are responsible for their disposal. • The Unreconciled Payments Report (UPR) is due to PPMB by the last Thursday of each month. Finance will be notified of all outstanding UPR certifications to be reported to the NOAA CFO each month. • Effective April 1, 2013, Line and Staff Offices will submit their UPR and CWIP UPR Certifications accompanied with a signed cover letter memorandum certified by the Assistant Administrator (AA) or Directors of the respective L/S Offices. All submitted certifications should have explanation for the expenditures listed on the download, have proper signatures, and have all necessary supporting documentation for the asset entry. • All accountable asset additions need to have the appropriate documentation (Contract/Purchase Order, Bank Card Statement, Vendor Invoice, Purchase Receipt) to support the acquisition cost.