Short-Term Financial Planning

190 likes | 444 Vues

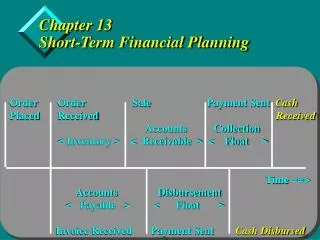

Short-Term Financial Planning. FIL 341 Prepared by Keldon Bauer. Sources of Cash Obtaining financing: Increase in long-term debt Increase in equity Increase in current liabilities Selling assets Decrease in current assets Decrease in fixed assets. Uses of Cash

Short-Term Financial Planning

E N D

Presentation Transcript

Short-Term Financial Planning FIL 341 Prepared by Keldon Bauer

Sources of Cash Obtaining financing: Increase in long-term debt Increase in equity Increase in current liabilities Selling assets Decrease in current assets Decrease in fixed assets Uses of Cash Paying creditors or stockholders Decrease in long-term debt Decrease in equity Decrease in current liabilities Buying assets Increase in current assets Increase in fixed assets Sources and Uses of Cash

Working Capital Simple Cycle of operations Cash Raw materials inventory Receivables Finished goods inventory

The Operating Cycle • The time it takes to receive inventory, sell it and collect on the receivables generated from the sale • Operating cycle = inventory period + accounts receivable period • Inventory period = time inventory sits on the shelf • Accounts receivable period = time it takes to collect on receivables

The Cash Cycle • The time between payment for inventory and receipt from the sale of inventory • Cash cycle = operating cycle – accounts payable period • Accounts payable period = time between receipt of inventory and payment for it • The cash cycle measures how long we need to finance inventory and receivables

Flexible (Conservative) Policy Large amounts of cash and marketable securities Large amounts of inventory Liberal credit policies (large accounts receivable) Relatively low levels of short-term liabilities High liquidity Restrictive (Aggressive) Policy Low cash and marketable security balances Low inventory levels Little or no credit sales (low accounts receivable) Relatively high levels of short-term liabilities Low liquidity Short-Term Financial Policy

Current Assets Net Working Capital > 0 Fixed Assets Current Liabilities Long-Term Debt Equity low cost low return high cost high return highest cost The Tradeoff Between Profitability & Risk • Positive Net Working Capital (low return and low risk)

Current Assets Fixed Assets Current Liabilities Net Working Capital < 0 Long-Term Debt Equity low return low cost high return high cost highest cost The Tradeoff Between Profitability & Risk (cont.) • Negative Net Working Capital (high return and high risk)

Carrying versus Shortage Costs • Carrying costs • Opportunity cost of owning current assets versus long-term assets that pay higher returns • Cost of storing larger amounts of inventory • Shortage costs • Order costs – the cost of ordering additional inventory or transferring cash • Stock-out costs – the cost of lost sales due to lack of inventory, including lost customers

Temporary versus Permanent Assets • Are current assets temporary or permanent? • Both! • Permanent current assets refer to the level of current assets that the company retains regardless of any seasonality in sales • Temporary current assets refer to the additional current assets that are added when sales are expected to increase on a seasonal basis

Choosing the Best Policy • Best policy will be a combination of flexible and restrictive policies • Things to consider • Cash reserves • Maturity hedging • Relative interest rates • Compromise policy – borrow short-term to meet peak needs, maintain a cash reserve for emergencies

Modeling the Policy • To model this policy, we must add lines on the balance sheet (if they aren’t there already). • Marketable securities. • Short-term borrowings. • Add a way of checking for balance at the bottom of the balance sheet. • Balance check. • Absolute difference. • Check figure.

Modeling the Policy • Add a line that shows the balances of all accounts on both sides of the balance sheet except for the marketable securities and liabilities/equity. • One for each side of the balance sheet. • These are there to use in bringing the whole thing iteratively into balance.

Modeling the Policy • Using the All-But lines, balance by bringing the lower one up by the amount needed to balance. • This is done on Excel with if statements. • Then we will add lines that add the interest income and expense to the income statement. • Which means that new lines are also added to the income statement to ease our modeling.

Modeling the Policy • Finally, a macro is written to copy and paste the necessary lines into the balance sheet and income statement respectively. • Then an iteration is added to have it continue until the balance sheet balances. • See the example we did in class.

Sources of Short Term Borrowing • Bank loans • Commitment • Maturity • Rate of interest • Syndicated loans • Loan sales • Security • Commercial paper • Medium term notes