Download

1 / 14

140 likes | 249 Vues

Explore the concepts of arbitrage and the law of one price in international finance along with key terms like spot rate, forward rate, forward discount, and forward premium. Understand theoretical economic relationships such as purchasing power parity, Fisher effect, and interest rate parity for currency forecasting. Dive into the world of currency exchange rates and their impact on financial markets.

E N D

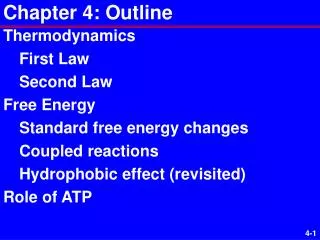

Chapter 4 Outline • Arbitrage and the Law of One Price • Key Terms • Theoretical Economic Relationships • Currency Forecasting • In real life, all calculations are handled by computer models. Therefore the emphasis is on the Directional Analysis! Chapter 4: Parity Conditions in International Finance and Currency Forecasting

4.A Arbitrage and the Law of One Price • Arbitrage – the simultaneous purchase and sale of the same assets or commodities on different markets to profit from price discrepancies • Law of One Price – in competitive markets, exchange-adjusted prices of identical tradable goods and financial assets must be within transaction costs of equality worldwide. • Absent market imperfections, arbitrage ensures that exchange-adjusted prices of identical traded goods follow the Law of One Price. Chapter 4: Parity Conditions in International Finance and Currency Forecasting

x 360 Forward premium/discount = f1 – e0 e0 Forward contract number of days 4.B Key Terms • Spot rate e0 – current exchange rate of currency • Forward rate f1 – exchange rate of currency on a specified future date • Forward discount – the discount applied to a currency if the forward rate is below the spot rate • Forward premium – the premium applied to a currency if the forward rate is above the spot rate. Must be able to do!!!!! Chapter 4: Parity Conditions in International Finance and Currency Forecasting

4.C Theoretical Economic Relationships (1) • In the absence of market imperfections, risk-adjusted expected returns on financial assets in different markets should be equal. • Five key theoretical economic relationships result from arbitrage. • Purchasing power parity (PPP) – for prices in two countries to be equal, the exchange rate between the two countries must change by the difference between the domestic and foreign rates of inflation. • Fisher effect (FE) – If expected real interest rates differ between the home and foreign countries,capital will flow to the country with the higher real rate until the real rates in both countries are equal and equilibrium is reached. • International Fisher effect (IFE) – combines the conditions underlying PPP and FE; if real interest rates differ between the home and foreign countries,capital will flow to the country with the higher real rate until the exchange-adjusted returns are equal in both countries and equilibrium is reached. • Interest rate parity (IRP) – in an efficient market with no transaction costs,the interest rate differential between two countries should approximate the forward differential. • Forward rates as unbiased predictors of future spot rates (UFR) – Equilibrium is achieved when the forward differential equals the expected change in the spot rate. Chapter 4: Parity Conditions in International Finance and Currency Forecasting

4.C Theoretical Economic Relationships (2) • Note: The equations presented in the discussions of the theoretical economic relationships are “approximations” of formal equations. For example, in the discussion of purchasing power parity, we present the equilibrium state as achieved when e1 – e0 ih – if = e0 This equation is a commonly used and accepted approximation of the following formal equation, which is presented and discussed in the textbook. (1 + if)t et = e0 (1 + ih)t The approximation equations are used to graphically illustrate each theoretical economic relationship. Chapter 4: Parity Conditions in International Finance and Currency Forecasting

4.C.i Theoretical Economic Relationships: Purchasing Power Parity (PPP) (4*) • Nominal exchange rate versus real exchange rate, continued • If changes in et are offset by changes in inflation between two countries, et’ remains unchanged. • Thus, a change in et’ is equivalent to a deviation from PPP. • E.g., compute and compare changes in the real and nominal values of the yen relative to the dollar (i.e., et and et’ = $/¥) from 1982 to 2006 • etin 1982 (e0 = base year) = $1/¥249.05, et in 2006 (e25) = $1/¥116.34 • CPIJapan in 1982 = 80.75, CPIJapan in 2006 = 97.72; if = 21% • CPIUS in 1982 = 56.06, CPIUS in 2006 = 117.07; ih = 109% (1 + 21%) = $.004981 e25’ = $1/¥116.34 (1 + 109%) • e0’ = $1/¥249.05 = $.004015. • Change in et’ = ($.004981 - $.004015) / $.004015 = 24%, meaning the yen appreciated 24% against the dollar in real terms – that is, the real dollar prices of Japanese exports rose by 24%. Chapter 4: Parity Conditions in International Finance and Currency Forecasting

4.C.i Theoretical Economic Relationships: Purchasing Power Parity (PPP) (5*) • Nominal exchange rate versus real exchange rate, continued • E.g., compute and compare the changes in the real and nominal values of the yen relative to the dollar from 1982 to 2006, continued • Change in et = (($1/¥116.34) – ($1/¥249.05)) / ($1/¥249.05) = 114%, meaning the nominal dollar prices of Japanese exports rose by 114% over the period. • Difference between et and et’ = 114% - 24% = 90%. • Conclusion: Inflation differentials justify only a 90% rise in et . Thus, the increase in et’causes a deviation from PPP by 24%. Chapter 4: Parity Conditions in International Finance and Currency Forecasting

4.C.ii Theoretical Economic Relationships: Fisher Effect (FE) (1) • The nominal interest rate compensates lenders for the erosion of future purchasing power of dollars loaned. • Because virtually all financial contracts are stated in nominal terms, the real interest rate a must be adjusted to reflect expected inflation. • FE states that the nominal interest rate r = a required rate of return a and an inflation premium equal to expected inflation i: r = a + i + ai • Real returns are equalized across countries through arbitrage; i.e., over time, ah= af. • If expected ah≠ af, capital would flow to the country with the higher real rate until ah= af and equilibrium is reached. • In equilibrium with no government interference, rh - rf = ih- if Chapter 4: Parity Conditions in International Finance and Currency Forecasting

4.C.iii Theoretical Economic Relationships: International Fisher Effect (IFE) (1) • IFE combines the conditions underlying PPP and FE. • Thus, in equilibrium, ē1 – e0 rh – rf = e0 • If rh ≠ rf, capital will flow from the country with the lower expected return to the country with the higher expected return, causing e0to adjust by the interest rate differential such that rh = rf and a new equilibriumis established. • Interest rate differentials are thus unbiased (while not necessarily accurate) predictors of ē1. Chapter 4: Parity Conditions in International Finance and Currency Forecasting

4.C.iv Theoretical Economic Relationships: Interest Rate Parity (IRP) (2*) • Covered interest arbitrage (CIA) – profiting from interest rate differentials in rhand rf(when IRP does not hold). E.g.: • rUK= 12%, rUS = 7% • e0= $/£ = $1.95, f1 = $1.88 • rUK –rUS = 5% • (f1 – e0)/e0 = ($1.88 - $1.95)/$1.95 = -3.6% = forward discount • rUK –rUS≠ (f1 – e0)/e0 • Funds will flow from U.S. to U.K. to exploit profit opportunity (CIA) • As pounds are bought spot and sold forward, e0 will increase and f1will decrease, increasing the forward discount • As funds flow from U.S. to U.K., rUSwill increase and rUK will decrease. • CIA will continue until IRP is achieved. Chapter 4: Parity Conditions in International Finance and Currency Forecasting

4.C.v Theoretical Economic Relationships: Forward Rate and Future Spot Rate (1) • Absent government intervention, e0 and f1 are heavily influenced by current expectations of future events. • The two rates move in tandem, linked by interest differentials. • E.g., the pound is expected to depreciate. • Holders of pounds sell pounds forward. • Sterling-area dollar earners reduce sales of dollars in the forward market. • f1 will decrease. • Banks will sell e0 to offset f1 positions. • Earners of pounds will accelerate their collection and conversion of pounds. • Thus, pressure from the forward market is transmitted to the spot market, and vice versa. Chapter 4: Parity Conditions in International Finance and Currency Forecasting

ē1 – e0 f1 – e0 = e0 e0 ft = ēt 4.C.v Theoretical Economic Relationships: Forward Rate and Future Spot Rate (2) • Equilibrium is achieved when the forward differential equals the expected change in e0 (ē1). • Thus, in equilibrium, • In equilibrium, incentives to buy or sell currency forward do not exist. • ft should reflect ēt on the date of settlement of the forward contract. • Thus, the unbiased forward rate (UFR) condition is Chapter 4: Parity Conditions in International Finance and Currency Forecasting

4.D Currency Forecasting (1) • Requirements for successful currency forecasting • Exclusive use of a superior forecasting model • Consistent access to information • Exploiting small, temporary deviations from equilibrium • Predicting the nature of government intervention in the foreign exchange market • Market-based forecasts can be obtained by extracting the predictions embodied in interest and forward rates. • f1is an unbiased estimate of ē1 (forecasting usefulness limited to one year given the general absence of longer-term forward contracts) • Interest rate differentials can be used as predictors beyond one year. Chapter 4: Parity Conditions in International Finance and Currency Forecasting

4.D Currency Forecasting (2) • Model-based forecasts are based on technical and/or fundamental analysis • Fundamental analysis involves examining macroeconomic variables and policies likely to influence a currency’s prospects. • Technical analysis focuses exclusively on past price and volume movements to identify price patterns. • Model-based forecasts are inconsistent with the efficient market hypothesis – because markets are forward looking, exchange rates will fluctuate randomly as market participants assess and react to news. • Exchange controls and restrictions on imports and capital flows often mask the true pressures on a currency to devalue. Chapter 4: Parity Conditions in International Finance and Currency Forecasting