Download

1 / 21

210 likes | 237 Vues

Learn about the shortcomings of simple job order costing and how implementing activity-based costing can provide a superior way to allocate costs for various products. Discover the nuances of activity-based costing and its application through detailed examples and steps. Explore how designing and applying an activity-based costing system can lead to better product costing insights and informed decision-making processes. Gain valuable insights on activity-based management and optimizing production processes through ABC analysis.

E N D

May 12-13, 2009 Systems Design: Activity Based Costing

Activity Based Costing • Shortcomings of Simple Job Order Costing • What is Activity Based Costing? • How is it Superior? • How is it Applied? • Journal Entries

Shortcomings of Simple Job Order Costing • Plant-wide allocation of costs may be a reasonable methodology for single product facilities • Increasingly, companies produce a multitude of products out of the same plant • These different products tend to consume different amounts of overhead • Additionally overhead is increasing as a proportion of overall cost and consequently its allocation becomes more meaningful • In these circumstances, a simple plant wide allocation is not granular enough to capture good product cost information

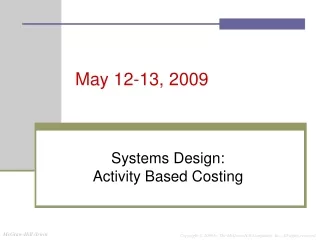

First-Stage Cost Assignment LaborRelated Pool MachineRelated Pool SetupPool ProductionOrder Pool PartsAdmin. Pool GeneralFactory Pool Second-Stage Allocations $/DLH $/MH $/Setup $/Order $/Part Type $/MH Products Unit-LevelActivity Batch-LevelActivity Product-LevelActivity Facility-LevelActivity Graphic Example ofActivity-Based Costing Various Manufacturing Overhead Costs

What is Activity Based Costing (ABC)? • Activity Based Costing is a methodology for allocating costs based on: • Each of the activities associated with producing a product, and • The level of overhead that each of these require • There are a number of allocation bases for assigning costs to products • We end up with a more accurate understanding of Product Cost • Better basis for manufacturing and pricing decisions

Applying Activity Based Costing • Applying ABC requires: • Detailed understanding of the organization • Overhead departments, functions and activities • Manufacturing departments, functions and activities • Detailed costing for all • Judgment • Selecting which costs to map to which products • What allocation base to use • The impact of these decisions can be material and therefore managers must understand the underlying information to trouble-shoot

Designing an Activity-BasedCosting System • Select a few activities which capture most of the overhead • Group the related activities; eg materials handling • Interview company managers to understand which overhead costs they believe are most costly and most critical to efficient production • Interview marketing and sales people to understand which products are most sensitive to pricing • Establish which cost objects to focus upon in more detail • Design the system from cost-down and product-up • Ensure all costs are captured

Applying Activity-Based Costing • List all Cost Objects; i.e., products to be costed • List all Overhead Departments / Costs • Identify Activity Cost Pools that production of each product requires • E.g., maintaining machines. Other examples? • Establish which overhead costs are consumed for the activity • E.g., Maintenance Mechanics Department • Measure the activity • Calculate the cost • E.g., the overall cost of the Mechanics Department • Select the Allocation Bases and Activity Rate • Simply the POHR, except for each activity • E.g., Cost of Maintenance Mechanics / Estimated hours of machine operation

First-Stage Cost Assignment LaborRelated Pool MachineRelated Pool SetupPool ProductionOrder Pool PartsAdmin. Pool GeneralFactory Pool Graphic Example of Activity-Based Costing Various Manufacturing Overhead Costs • Where cost correlations and overhead support required are similar, it is practical to consolidate the Activity Pools • Information systems are strong and can support extraordinary complexity • However, at a certain point the complexity becomes overly cumbersome interpret

First-Stage Cost Assignment LaborRelated Pool MachineRelated Pool SetupPool ProductionOrder Pool PartsAdmin. Pool GeneralFactory Pool Second-Stage Allocations $/DLH $/MH $/Setup $/Order $/Part Type $/MH Products Unit-LevelActivity Batch-LevelActivity Product-LevelActivity Facility-LevelActivity Graphic Example ofActivity-Based Costing Various Manufacturing Overhead Costs

Using Activity-Based Costing • An electronics manufacture produces Cell Phones and Servers • It uses a DL hours bases Overhead allocation system • What are the product costs of each product? • What are your observations?

Using Activity-Based Costing • Note that Manufacturing Overhead as a percentage of product cost is more than 4 times higher for cell phones!

Computing Activity Rates • The company undertook to implement ABC • Established Cost Objects, Activity Pools, and Rates

Methodology Results- A Comparison • Which methodology is more accurate? Why? • Cell phone costs decreased by 5% under ABC. Why? • What opportunities are there for the company?

Targeting Process Improvements • Activity Based Management • Using ABC output to identify areas of improvement • Reduce costs • Reduce production time, and • Reduce defects / improve quality • Identify high cost areas first • Benchmark against 3rd party data to identify weaknesses • What areas might we take a closer look at in the Electronics Manufacturer example?

ABC – Cost Flows and Journal Entries • Cost flows are the same for ABC as for Job-Order Costing, except ABC has more POHRs • Over and under allocations of Manufacturing Overhead are dealt with through COGS • As with Job-Order Costing

Review • Shortcomings of Simple Job Order Costing • What is Activity Based Costing? • When should it be Applied? • How is it Superior? • Journal Entries

Tutorial • Assignment • Review Problem • Complete Alternative Problem 3-15-B • Submit as homework – May 13th Tutorial