Download

1 / 55

570 likes | 892 Vues

Money, Interest Rates, and the Exchange Rate. CHAPTER ORGANIZATION. Introduction Money Defined: A Review The Supply of Money The Demand for Money The Equilibrium Interest Rate: The Interaction of Money Supply and Money Demand The Interest Rate and the Exchange Rate in the Short Run

E N D

CHAPTER ORGANIZATION • Introduction • Money Defined: A Review • The Supply of Money • The Demand for Money • The Equilibrium Interest Rate: The Interaction of Money Supply and Money Demand • The Interest Rate and the Exchange Rate in the Short Run • Interest Rates, the Exchange Rate, and the Balance of Payments • Summary

INTRODUCTION • Exchange rates change almost every minute of every business day even though inflation and the growth rate of the GDP do not • Short-term interest rates influence exchange rate movement over short periods of time • A change in the interest rate leads to changes in a country’s financial account and changes in capital flows lead to changes in the exchange rate • These all interact with one another

MONEY DEFINED: A REVIEW • Money has to perform three different functions • It’s most important function is as a medium of exchange • It eliminates relative pricing • It also serves as a unit of account • It standardizes values of goods, improves the efficiency of economic transactions, and makes it easy to compare transactions

MONEY DEFINED: A REVIEW • Money is a store of value • There is often a mismatch in timing between income and consumption • Money is not perishable and can be kept in checking accounts or other convenient places • Smoothes inconsistencies between money earned and money spent • It is useful for long-run savings • Individuals in high inflation countries my keep other currencies or goods as a store of value

THE SUPPLY OF MONEY • Coins and paper currency are money because they act as primary mediums of exchange • Demand deposits held at commercial banks and depository institutions are money because they provide the same function as currency • The sum of currency plus demand deposits is called the money supply • This is called M1 and in known internationally as narrow money

THE SUPPLY OF MONEY • Other definitions of money are possible • These are referred to as near monies that can be used as money in many circumstances • Near monies are savings accounts, time deposits, and short-term government securities • In the U.S., M1 plus money market mutual funds and time deposits constitute M2 • Internationally this is knows as broad money

THE SUPPLY OF MONEY • The monetary base (B) is an important part of the money supply • This is composed of cash in the hands of the public (C) and the total quantity of bank reserves (R) on deposit at the central bank B = C + R

THE SUPPLY OF MONEY • A country’s money supply is equal to the monetary base multiplied by the banking money multiplier • The banking money multiplier is equal to 1 divided by the reserve requirement • In most countries depository institutions must keep a legal or required reserve • The reserve requirement is an amount of funds equal to a specified percentage of its own deposits (r) MS = B 1/r

THE SUPPLY OF MONEY • When the central bank wants to change the money supply, it changes the monetary base and/or the money multiplier • This is one of three tools central banks can use to change the supply of money • They can change the discount rate, the interest rate the central bank charges commercial banks for borrowing reserves • When a commercial bank borrows reserves from the central bank, the money supply increases by a multiple of that amount

THE SUPPLY OF MONEY • When the central bank lowers the discount rate, commercial banks tend to borrow more • Using the discount rate to control the money supply is not very precise • The central bank can also change the reserve requirement • If the reserve requirements were lower, banks would be able to hold a smaller fraction of their deposits and could make more loans

THE SUPPLY OF MONEY • Changes in the reserve requirement change the size of the money multiplier • A relatively small change in the reserve requirement brings about relatively large changes in the money multiplier • This tool is rarely used because the effect is potentially too powerful • In countries with well-developed financial markets, the monetary base and the money supply are usually in a more precise fashion using open market operations

THE SUPPLY OF MONEY • Open market operations refer to the buying and selling of bonds by central bank in the open market • If the central bank buys bonds, money is given to bond seller (public or bank) and more money is in the economy • If the central bank sells bonds, money is taken from bond buyers (public or bank) and less money is in the economy • These operations affect only the supply of money

THE SUPPLY OF MONEY Table 15.1 Reserve Requirements for Selected Countries

THE DEMAND FOR MONEY • There are three major reasons for individuals and firms to hold money • Individuals and firms hold money to buy goods and services • This is called the transactions demand for money and varies directly with nominal GDP • Individuals and firms hold money in case of emergencies that require purchases above normal spending levels

THE DEMAND FOR MONEY • There is an opportunity cost to holding money because it as no explicit rate of return • The demand for money by individuals and firms is inversely related to the interest rate • The combination of these three motivations creates the demand for money, the total demand for money by all firms and individuals in the economy

THE DEMAND FOR MONEY • The demand for money is inversely related to the interest rate, directly related to the price level, and directly related to the real level of economic activity or real income MD = f(–I, +P, +Y) where I is the interest rate, P is the price level, and Y is real GDP

THE EQUILIBRIUM INTEREST RATE: THE INTERACTION OF MONEY SUPPLY AND MONEY DEMAND • The central bank determines money supply through open market operations, the discount rate, and the reserve requirement • When the money supply is completely inelastic with respect to interest rates it does not respond to interest rate changes • Under these conditions, the central bank can determine its level at some arbitrary level

Interest Rate(i) MS” Money Supply (MS) MS’ Money (M) THE EQUILIBRIUM INTEREST RATE: THE INTERACTION OF MONEY SUPPLY AND MONEY DEMAND Figure 15.1 Changes in the Supply of Money

THE EQUILIBRIUM INTEREST RATE: THE INTERACTION OF MONEY SUPPLY AND MONEY DEMAND • The demand curve for money slopes downward indicating that as interest rates fall, the amount of money that individuals and firms are willing and able to hold increases • As interest rates change, individuals and firms adjust the quantity of money they hold by moving along the demand curve • If real income or price level change, the entire demand curve for money will shift

Interest Rate(i) A B Demand for Money (MD) Money (M) THE EQUILIBRIUM INTEREST RATE: THE INTERACTION OF MONEY SUPPLY AND MONEY DEMAND Figure 15.2 The Demand for Money

Interest Rate(i) MD’ MD MD” Money (M) THE EQUILIBRIUM INTEREST RATE: THE INTERACTION OF MONEY SUPPLY AND MONEY DEMAND Figure 15.3 Changes in the Demand for Money

THE EQUILIBRIUM INTEREST RATE: THE INTERACTION OF MONEY SUPPLY AND MONEY DEMAND • Intersection of money demand and money supply determines the equilibrium interest rate • The equilibrium in the money market occurs as individuals and firms adjust their asset holdings • A change in either the real income or the price level shifts the demand curve and changes the equilibrium interest rate • The standard analysis of the money market also considers the effect of changes in the money supply on the equilibrium rate of interest

Interest Rate(i) Supply of Money (MS) E i Demand for Money (MD) Money (M) THE EQUILIBRIUM INTEREST RATE: THE INTERACTION OF MONEY SUPPLY AND MONEY DEMAND Figure 15.4 The Equilibrium Interest Rate

Interest Rate(i) MS G I” E i MD” F I’ MD MD’ Money (M) THE EQUILIBRIUM INTEREST RATE: THE INTERACTION OF MONEY SUPPLY AND MONEY DEMAND Figure 15.5 Shifts in the Demand for Money and the Equilibrium Interest Rate

THE EQUILIBRIUM INTEREST RATE: THE INTERACTION OF MONEY SUPPLY AND MONEY DEMAND • If the central bank changes the money supply, interest rates will also change • Given a stable money demand, a higher money supply implies lower interest rates • In developed countries, changes in the money supply are usually accomplished using open market operations • Changes in the equilibrium interest rate usually translate into changes in the country’s exchange rate

Interest Rate(i) MS” MS MS’ G I” E i F I’ MD Money (M) THE EQUILIBRIUM INTEREST RATE: THE INTERACTION OF MONEY SUPPLY AND MONEY DEMAND Figure 15.6 Shifts in the Supply of Money and the Equilibrium Interest Rate

THE INTEREST RATE AND THE EXCHANGE RATE IN THE SHORT RUN • The short run relationship between interest rates and the exchange rate is known as interest arbitrage • This relationship hinges on the existence of international markets in which short-term capital can flow unimpeded between countries • Firms must decide how to invest idle cash balances • The goal is to maximize the short-run rate of return • The highest short-term return might be in the U.S. or it might be in some foreign country

THE INTEREST RATE AND THE EXCHANGE RATE IN THE SHORT RUN • With the presence of exchange risk, the comparison of interest rates between two countries is not a sufficient guide to allocate funds • Moving money to another country involves an exchange rate risk • Even if interest rates are better, changes in the exchange rate over time could affect rate of return on an investment

THE INTEREST RATE AND THE EXCHANGE RATE IN THE SHORT RUN • To eliminate exchange rate risk, a firm can buy foreign currency in spot exchange market and at same time sell in forward exchange market with a delivery date that coincides with the maturity of the investment • Under most circumstances, the movement of funds between countries continues until the forward premium or discount equals the interest rate differential • The interest rate differential is exactly balanced by the loss or gain of buying and selling currency

THE INTEREST RATE AND THE EXCHANGE RATE IN THE SHORT RUN • The rate of return on an investment in both countries is identical and there is no reason to move funds from one country to another • When this situation occurs, it is said that the forward rate is at interest parity or that interest parity prevails between the two countries

U.S. Interest Rate(i) MS’ MS F i’ U.S. Money Market E i MD Money (M) THE INTEREST RATE AND THE EXCHANGE RATE IN THE SHORT RUN Figure 15.7(a) Effect of a Decrease in the U.S. Money Supply on the Dollar–Pound Exchange Rate

Dollar/Pound Exchange Rate S S’ $/£ E’ The Dollar/Pound Foreign Exchange Market $/£’ F’ D Pounds THE INTEREST RATE AND THE EXCHANGE RATE IN THE SHORT RUN Figure 15.7(b) Effect of a Decrease in the U.S. Money Supply on the Dollar–Pound Exchange Rate

MS MS’ U.S. Interest Rate U.S. Money Market E i G i’ MD Money (M) THE INTEREST RATE AND THE EXCHANGE RATE IN THE SHORT RUN Figure 15.8(a) Effect of a Increase in the U.S. Money Supply on the Dollar–Pound Exchange Rate

Dollar/Pound Exchange Rate S G’ $/£’ $/£ E’ The Dollar/Pound Foreign Exchange Market D’ D Pounds THE INTEREST RATE AND THE EXCHANGE RATE IN THE SHORT RUN Figure 15.8(b) Effect of a Increase in the U.S. Money Supply on the Dollar–Pound Exchange Rate

THE INTEREST RATE AND THE EXCHANGE RATE IN THE SHORT RUN • These examples can be generalized to many countries • Everything else equal, an increase in a country’s interest rate will tend to cause a capital inflow and an appreciation of the country’s currency • The mechanism that causes the exchange rate to change is the movement of capital between countries • As interest rates change, both the volume and direction of worldwide capital flows change

THE INTEREST RATE AND THE EXCHANGE RATE IN THE SHORT RUN • As changes in capital flows occur, the supply and demand for foreign exchange changes, which in turn affects exchange rate • Since it is unlikely that interest rates will stop fluctuating any time in the near future, one should not be too optimistic about exchange rates becoming very stable any time soon

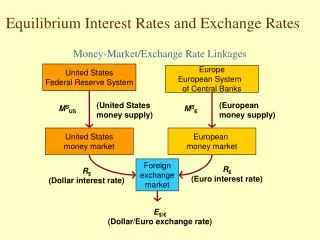

INTEREST RATES, THE EXCHANGE RATE, AND THE BALANCE OF PAYMENTS • Over time, a country’s inflows and outflows of money are balanced • The interaction of the current account and the capital and financial accounts jointly determine this balance • If domestic price levels and income change, trade flows between two countries would change • The equilibrium exchange rate would adjust to a new level • As money supply and interest rates change, capital flows and the exchange rate are affected

Exchange Rate Dollar/Pound S Foreign Exchange Market Without Capital Flows $/£ E D Money (M) INTEREST RATES, THE EXCHANGE RATE, AND THE BALANCE OF PAYMENTS Figure 15.9(a) The Foreign Exchange Market With and Without Capital Flows

S Exchange Rate Dollar/Pound S’ $/£ E Capital Inflow Foreign Exchange Market With Capital Flows $/£’ F G D Money (M) INTEREST RATES, THE EXCHANGE RATE, AND THE BALANCE OF PAYMENTS Figure 15.9(b) The Foreign Exchange Market With and Without Capital Flows

Exchange Rate Yen/Dollar S Foreign Exchange Market Without Capital Flows ¥/$ E D Money (M) INTEREST RATES, THE EXCHANGE RATE, AND THE BALANCE OF PAYMENTS Figure 15.10(a) The Foreign Exchange Market With and Without Capital Flows

S Exchange Rate Yen/Dollar F ¥/$’ Foreign Exchange Market With Capital Flows G E ¥/$ Capital Outflow D’ D Money (M) INTEREST RATES, THE EXCHANGE RATE, AND THE BALANCE OF PAYMENTS Figure 15.10(b) The Foreign Exchange Market With and Without Capital Flows

SUMMARY • Money is an asset that acts as a medium of exchange, a unit of account and a store of value • The monetary base is equal to cash in the hands of the public plus the total quantity of bank reserves • In practice, a country’s central bank changes the money supply by changing the discount rate, changing the required reserve ratio, or by conducting open market operations

SUMMARY • Individuals’ and businesses’ demand for money is inversely related to the interest rate, positively related to the price level, and positively related to the level of real income • When the demand for money is equal to the supply of money, the money market is in equilibrium • Interest rates and exchange rates are interrelated though interest arbitrage • The Foreign Exchange market equates the total inflow of foreign exchange with the total outflow of foreign exchange

The Relationship Between the Monetary Base and the Money Supply A P P E N D I X 1 5 . 1

THE RELATIONSHIP BETWEEN THE MONETARY BASE AND THE MONEY SUPPLY • In the chapter it was assumed that individuals and businesses did not want to hold any currency • It is important to understand the logic and limits of the expansion process • We can accomplish this by employing the concept of the monetary base • The monetary base includes all currency and coins in circulation plus the sum of the Federal Reserve accounts that depository institutions own

THE RELATIONSHIP BETWEEN THE MONETARY BASE AND THE MONEY SUPPLY • The Federal Reserve directly controls the monetary base, or “high powered money,” and is the ultimate source of the U.S. money supply • The monetary base, B, consists of the total depository reserves, R, plus cash in the public’s hand, C B = R + C • The money supply consists of total deposits, D, plus cash MS = C + D

THE RELATIONSHIP BETWEEN THE MONETARY BASE AND THE MONEY SUPPLY • In equilibrium, all depository institution reserves are required reserves (R) where r denotes the reserve ratio R = [r]D • Assume the public wants to hold a constant fraction, k, of its money as cash and the rest as deposits C = k(D)

THE RELATIONSHIP BETWEEN THE MONETARY BASE AND THE MONEY SUPPLY • Thus the monetary base equals B = [r]D + k(D) = [r + k]D • Or the total deposits of all financial institutions are D = B(1/[r + k]) • Thus MS = D + C = D + k(D) = (1 + k)D

THE RELATIONSHIP BETWEEN THE MONETARY BASE AND THE MONEY SUPPLY • Substituting for D, we can obtain MS = (1 + k)D = [(1 + k)/(r + k)] B • The money multiplier is [(1 + k)/(r + k)]