Annuities

Annuities. Chapter 11. Annuities. Equal Cash Flows at Equal Time Intervals Ordinary Annuity (End): Cash Flow At End Of Each Period Annuity Due (Begin): Cash Flow At Beginning Of Each Period Examples: Savings Plan : Save $50 at the end of each month

Annuities

E N D

Presentation Transcript

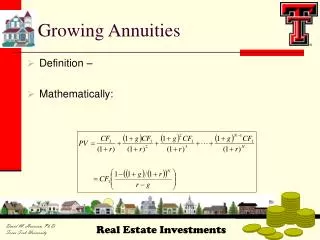

Annuities Chapter 11

Annuities • Equal Cash Flows at Equal Time Intervals • Ordinary Annuity (End): Cash Flow At End Of Each Period • Annuity Due (Begin): Cash Flow At Beginning Of Each Period • Examples: • Savings Plan: Save $50 at the end of each month • Savings Plan: How Much Do I have to put in bank each month for 35 years to become a millionaire? • Borrow Money: What is my monthly payment if I borrow $190,000? • Asset Valuation: How much should I pay for a machine if it will yield Cash Flow of $10,000 at the each of each year for the next 15 years?

Annuities • Annuity Definition: • A level steam of cash flows for a fixed period of time • Each payment is for the same amount • Payments are referred to as: PMT • The time between PMT is always the same • Timing for annuities: • Ordinary Annuity (Savings Plans, Mortgage contracts) • PMT are made at the end of each period • The day you sign the contract, you do not make a PMT • Annuity due (Lease contracts) • PMT are made at the beginning of each period

Types of Annuities • Savings plan: • If I put $50 (PMT) in the bank at the end of each month for 50 years, how much will I have when I retire? What is the future value? • Future value of future cash flows valuation: • If I want to be a millionaire, how much do I have to put in the bank at the end of each month. What is the PMTFV? • Loan (DEBT) periodic payment: • If I take out a loan for $190,000, what is the monthly payment amount paid at the end of each month (PMT)? What is the PMTPV? • Present value of future cash flows valuation • If I know the asset will give me $10,000 (PMT) at the end of each year for the next 15 years, what should I pay for this asset today? What is the present value?

FV & PMTFV forfor Ordinary Annuity (End) Math Formulas: Excel Functions: FV (Savings Plan) =FV(rate , nper , -PMT) PMT (Savings Plan) =PMT(rate , nper , , FV) **Skip PV arguments (put 2 commas)** If you put –PV in, it just means you had so $ in bank to start… FV =PMT*((1+i/n)^(x*n)-1)/(i/n) PMT =FV/(((1+i/n)^(x*n)-1)/(i/n))

FV & PMTFV for Annuity Due (Begin) Math Formulas: Excel Functions: FV (Savings Plan) =FV(rate , nper , -PMT , , 1) PMT (Savings Plan) =PMT(rate , nper , , FV , 1) **Skip PV arguments (put 2 commas)** If you put –PV in, it just means you had so $ in bank to start… FV =PMT*((1+i/n)^(x*n)-1)/(i/n)*(1+i/n) PMT =FV/(((1+i/n)^(x*n)-1)/(i/n))/(1+i/n)

PV & PMTPVfor Ordinary Annuity (End) Math Formulas: Excel Functions: PMT (Borrower Loan) =PMT(rate , nper , PV) **PV positive cuz bank lends it to you (regardless of whether you immediately pay the loan $ out) PV (Asset Valuation) =PV(rate , nper , PMT)**PMT positive cuz cash come into business, PV negative cuz that is max you should pay for asset PMT =PV/(((1+i/n)^-(x*n)-1)/(i/n)) PV =PMT*((1+i/n)^-(x*n)-1)/(i/n)

PV & PMTPVfor Annuity Due (Begin) Math Formulas: Excel Functions: PMT (Borrower Loan) =PMT(rate , nper , PV, ,1) **Skip FV arguments (put 2 commas) **PV positive cuz bank lends it to you (regardless of whether you immediately pay the loan $ out) PV (Asset Valuation) =PV(rate , nper , PMT, ,1)**PMT positive cuz cash come into business, PV negative cuz that is max you should pay for asset PMT =PV/(((1+i/n)^-(x*n)-1)/(i/n))/(1+i/n) PV =PMT*((1+i/n)^-(x*n)-1)/(i/n)*(1+i/n)

PMTPVfor Ordinary Annuity (End) Excel Functions: PMT (Withdraw During Retirement) =PMT(rate , nper , -PV) **PV negative cuz you put $ in bank, PMT positive cuz you get money in each period