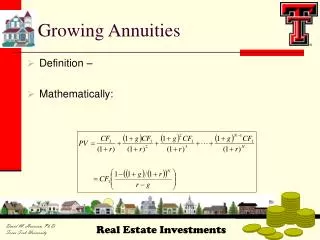

Annuities

Annuities. Definitions of Annuities . Annuity A contract with an insurance company to accumulate money on a tax deferred basis (No tax while in the annuity) Annuitize Give up access to your accumulated dollars in exchange for a stream of payments. Categories of Annuities. Fixed

Annuities

E N D

Presentation Transcript

Definitions of Annuities • Annuity A contract with an insurance company to accumulate money on a tax deferred basis (No tax while in the annuity) • Annuitize Give up access to your accumulated dollars in exchange for a stream of payments. • Categories of Annuities Fixed • Account credited with a fixed interest rate • Held in the insurance companies general account • Need insurance license to sell Variable • Deposits purchase “shares” called accumulation units (similar to a mutual fund) • Assets are held in a separate account • Need insurance license and security license (Series 6 or 7) to sell • Upon annuitization, the annuitant receives a fixed amount of annuity units ImmediateORDeferred Annuitize nowDo not annuitize now (maybe later) AND

Funding of Annuities ImmediateDeferred YES Lump Sum YES NO Fixed Installments YES NO Periodic Payments (deposits) YES

Annuity Accumulation FixedVariable • Cost: Investment charges & mortality charges • Many different accounts to choose from for specific allocations • Accumulation Units “shares” can change daily • (like a mutual fund) • Cost: Usually no annual fee • Interest Rate – • Current rate guarantee w/ • Minimum rate guarantee • May also receive “bonus” rate • Two Tiered • Fixed Interest with a • “mirror” Account (bigger interest rate) • with a designated time frame (7-10 years) • If annuitized, annuitant can use the bigger account to draw payments. • Equity Indexed • Assigned a “Cap” Rate (ex: 7%) • (Upside potential with no risk of losing principal)

Annuity Distribution Uncle Sam Insurance Company Taxes / Penalties Contract Charges / CDSC’s • Beneficiary is taxed on any gain as ordinary income Death • Generally no surrender charge • Gain comes first LIFO (Last In First Out) • 10% - Penalty – If prior to age 59 ½ • Loans not recognized by IRS • Decreasing surrender charge or • Market Value surrender charge – higher surrender charge if interest rates have increased -lower surrender charges if interest rate have decreased Partial Withdraw • No 10% penalty if you annuitize over • annuitants lifetime. • Exclusion Ratio = Investment in contract • Expected Return* • *Expected Return = Annual Amount received x Life Expectancy • (IRS table 590) Annuitize • None

Annuitizing Options LifePayoutTemporary Payout • Guaranteed payments for life of theNot based on annuitants life - but on either: • annuitant– they cannot out live payments • If joint annuity – payments stop at • Specific Time (ex: 5,10,15,20 years, etc.) • first death. or • If joint and survivor annuity - • Specific Amounts (ex: $X,XXX per: mo, yr, etc.) • payments stop at last death. (for however long it takes for balance to be paid) Options: A) Minimum TIME guarantees (Period Certain) can be added at a cost (causing lower payments) (the longer the minimum time guarantee - thelower the payment.) B) Minimum AMOUNTguarantees (Refund Annuity) Can be added at a cost (lower payment) - balance of initial premium amount is paid to beneficiaries (either in installments or lump sum) if annuitant dies before initial premium amount is paid out.