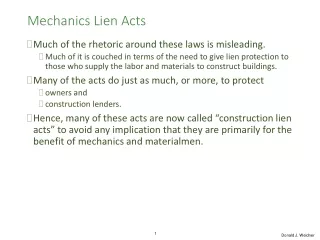

Mechanics Lien Acts

Mechanics Lien Acts Much of the rhetoric around these laws is misleading. Much of it is couched in terms of the need to give lien protection to those who supply the labor and materials to construct building. Many of the acts do at least as much, or more, to protect owners and

Mechanics Lien Acts

E N D

Presentation Transcript

Mechanics Lien Acts • Much of the rhetoric around these laws is misleading. • Much of it is couched in terms of the need to give lien protection to those who supply the labor and materials to construct building. • Many of the acts do at least as much, or more, to protect • owners and • construction lenders. • Hence, many of these acts are now called “construction lien acts” to avoid the implication that they are primarily for the benefit of mechanics and materialmen. Donald J. Weidner

Guignard Brick Works v. Gantt 159 S.E.2d 850 (S.C. 1968). Landowner General Guignard Brick Contract to build house for $19,000 22,000 bricks delivered to site Paid $7,000 on the contract Used 7,000 bricks and then ABANDONED the project Used remaining 15,000 bricks to complete construction, knowing they have not been paid for. Spent $29,000 to complete construction Sued Landowner, claiming “a lien for only the brick which has not been used in construction when the contract was abandoned by [General. Landowner] knew before he used these bricks” that Guignard Brick had not been paid. QUESTIONS: What is Guignard Brick’s argument on the basis of the statute at Supp. 70-71? Did not Guignard Brick furnish the brick with the “consent” of the owner? Donald J. Weidner

Guignard Brick (cont’d) • Bricksupplier claimed a lien under Section 1 set out in the Memorandum on Mechanics Liens (Supp. P. 74): • Saying it furnished bricks • That were actually used in the building • By virtue of an agreement with, or by consent of, the owner. • Concluding, therefore, that it had a lien on the building and upon the interest of the owner in the lot to secure the payment of the debt. • What is the Owner’s response to Bricksupplier’s claim under Section 1? • Bricksupplier is a subcontractor and subcontractors do not fall under Section 1. Donald J. Weidner

Guignard Brick (cont’d) • Section 2 (Supp. P. 74), on the other hand, refers to “[e]very laborer, mechanic, subcontractor or person furnishing material” • when an improvement has been authorized by the owner • gives a “lien” “subject to existing liens of which he has actual or constructive notice” • “to the value of the labor or material so furnished.” • Consider the last sentence in Section 4 (Supp. P. 75): • It states that the lien given by Section 2 attaches • When the laborer or materialman gives written notice to the owner of the furnishing of labor or material and its value • “But in no event shall the aggregate amount of liens set up hereby exceed the amount due by the owner on the contract price of the improvement made.” Donald J. Weidner

Guignard Brick (cont’d) • Mechanics lien statutes typically provide that the lien of all the subcontractors relates back to some earlier point prior to the point the materials or services were supplied or rendered. • Can you see why as a matter of policy this should be so? • See Section 7 for the “relation-back” mechanism: “Such a lien shall not avail or be of force against any mortgage actually existing and duly recorded prior to the date of the contract under which the lien is made.” • Highly atypical provision because it relates the lien back to the point of the contract (with the general contractor?). • Statutes more commonly provide that mechanics liens relate back to the commencement of construction (or to the filing of a notice of commencement of construction). Donald J. Weidner

More on Supplement pages 74-77 • B CLN & M L • B agrees to loan L • B Advance #1 L • B “I am not getting paid” Brick Co. • B Advance #2 L • What of the mechanics’ lien act? • Section 5 states that “no payment by the owner to the contractor [after notice] shall operate to lessen the amount recoverable by the person so giving the notice.” • Note: Is this a payment “by the owner?” • What of the “optional/obligatory” distinction? • Recall Florida Statute 697.04(1)(a) (Supp. P. 76) Donald J. Weidner

CASE ON “COMMENCEMENT” AND “PURCHASE MONEY MORTGAGE”Mechanics Lien v. 3d Party Purchase Money Mortgage Kloster-Madsen, Inc. v. Tafi’s Inc., 226 N.W.2d 603 (Minn. 1975), was an action to foreclose a mechanics lien Brought by Kloster-Madsen, a general contractor that furnished labor and material to remodel a 3-story building. The case involved a priority battle between Kloster-Madsen and Prudential Life Insurance Company, which had closed a loan that was part purchase-money loan and part improvement loan. Donald J. Weidner

Kloster-Madsen, Inc. v. Tafi’s Inc., 226 N.W.2d 603 (Minn. 1975). $PM (+Improvement $) Deed Seller Buyer Pru note Purchase A’ment for $225,000 July 1970 Seller Buyer • Court was faced with 2 issues: • Whether the electricians work on July 30 constituted an “improvement’ to the premises and “the actual and visible beginning of the improvement on the ground” within the meaning of the Mechanics Lien Act and • If yes, whether “a purchase money mortgage interest filed subsequent to the beginning of such improvement is entitled to priority if neither the vendor nor the purchase money mortgagee authorized the commencement of the work constituting the improvement.” anticipating purchase, enters into contract July 20, 1970 Buyer General Sub K Commenced work on the light fixtures (cut four holes in ceiling and crawl space without: 1)knowledge or authorization of lender or 2) authorization of seller [but, held, seller had knowledge]) July 30, 1970 Sub August 3, 1970 Purchase closed Donald J. Weidner

Kloster-Madsen (cont’d) • First, was the work on the light fixtures an “improvement”? • Second, was the improvement “visible”? • Contractor argued that you could see it. • Prudential argued, “not good enough” that it be visible “to the naked eye” • it had to be visible “to the mind’s eye.” Donald J. Weidner

Kloster-Madsen (cont’d) • The Court upheld the trial court’s finding that the improvement was “visible”: “The test for determining visibility is not, as Prudential argues, that the improvement, although ‘visible to the naked eye, must also be discernible to ‘the mind’s eyes insofar as they tell one’s mind that an improvement has been commenced.’ Rather, the test is whether the person performing the duty of examining the premises to ascertain whether an improvement has begun is able in the exercise of reasonable diligence to see it.” • The “mind’s eye” must use reasonable care? Donald J. Weidner

Kloster-Madsen (cont’d) • Third, is any pre-existing mortgage or mechanics lien defeated by Prudential’s purchase money mortgage? • Prudential relied on the special treatment given to purchase money mortgages • In general, purchase money mortgages are special because they are preferred to certain pre-existing claims against the buyer/purchase money mortgagor. • The purchase money mortgage has been explained in terms of instantaneous transitory seisin • This is what Prudential argued Donald J. Weidner

Kloster-Madsen (cont’d) Gets judgment lien on all real estate owned by Debtor CR Debtor Purchase Money Mortgages are special because they often permit the mortgagee to defeat pre-existing claims against the buyer/mortgagor. A purchase money mortgage takes precedence over: • Judgment liens against the mortgagor; • Liens arising from after-acquired property clauses in prior mortgages executed by the mortgagor; and • Claims against the mortgagor for dower and homestead. One Formalistic Explanation: Instantaneous transitory seisin. Pays $ Loans $ Seller Debtor Purchase Money Mortgagee contemporaneous convey Mortgage Under the purchase money mortgage rule, the mortgage of the purchase money mortgagee has priority over the prior creditor’s judgment lien. Donald J. Weidner

Kloster-Madsen (cont’d) • Court: the purpose of the doctrine of instantaneous seisin is “to protect mortgagees from hidden or undiscoverable liens.” • The mechanic’s lien here is not hidden or undiscoverable • “Prudential is chargeable with constructive notice of the attachment of a lien when the actual beginning of visible improvements occurs prior to the mortgage transaction.” • Further, the court said: the mechanics lien act does not make any distinction between purchase money mortgages and other mortgages. Donald J. Weidner

Kloster-Madsen (cont’d) • Contrary to Kloster-Madsen, the general rule is: a purchase money mortgage, whether in favor of the grantor or a third party, takes precedence over a mechanics’ lien. • An additional rationale for deciding opposite to Kloster-Madsen: • A mechanics’ lien statute does not include a contracting vendee in possession within the meaning of “owner” of an interest in the property to which the lien could attach. • In short, Kloster-Madsen was an extreme case insofar as the mechanics’ lien was preferred to a purchase money mortgagee who neither authorized nor knew of the improvements, when the vendor knew but did not authorize the improvements. Donald J. Weidner

Kelly Kelly holds the 1st Mortgage and the 2nd Mortgage, both of which Kelly acquired after actual knowledge of the work W & W had previously performed. Williams & Works, Inc. v. Springfield Corp.(Text p. 733) Contacts with interest in bldg. Apt. complex Convey Developer Springfield Mechanics Lien Claimant W & W Engineers Fee Owners Law Dev. Co. Kelly M & Inv. Co. Developer had the right to terminate the engineering contract at end of any phase June 1972 Formal contract: W&W to perform engineering services 8/29/72 12 holes into ground, 6” diameter “staked” Phase #1: Feasibility Studies Actual knowledge of W&W’s work Phase #2: Finalize all plans Sells and conveys land Developer Springfield 1/4/73 Mortgages land to CNB City Nat’l Bank 1/9/73 Records the 1st mortgage Assigns Mortgage (unclear when) 2nd Mortgage Developer Springfield Records 2nd Mortgage Phase #3: Physical Construction Begins; W & W supervises—sets stakes out ML 2/10/73 Files action to foreclose its mechanics lien ML 3/25/74 Donald J. Weidner

Williams & Works (cont’d) • Consider the “much amended” Section 1 of the act, in fn. 5. • Do you see the language that embraces a general contractor? • “Every person who shall, in pursuance of any contract . . . existing between himself as contractor, and the owner . . . .” • General is called simply “contractor” for most of the statute • [but is also referred to as “original or principal contractor”] • Do you see the language that specifically embraces subcontractors? Near the end of Section 1: • “and every person who shall be subcontractor, laborer, or material man . . . to such original or principal contractor” • Section 1 specifically refers to “any engineering plan” • Court: Section 1 does nothing more than describe what is “lienable.” Donald J. Weidner

Williams & Works (cont’d) • Section 9[3] of the mechanics’ lien act in fn. 1 contains a priority rule. • Consider the lien priority point: • Mechanics’ liens shall take priority over other liens “which shall either be given or recorded subsequent to the commencement of said building . . . or improvement.” • “Improvement” is defined in FN. 6 to include “designs or engineering plans.” • Engineers Williams & Works—argue that their mechanics lien is superior to the mortgages that were both given and recorded after their “improvement” (their “engineering plan”) was begun. • How could the mechanics lien claimants possibly lose this case? • “non-visible, off-site engineering services . . . although lienable under Michigan law, do not signal ‘commencement’ of a building . . . or improvement for the purpose of fixing priority under Michigan’s Mechanics’ Lien Law.” Donald J. Weidner

Summary of Major Concepts • When does a lien attach? • The three most common possibilities are the date • when the general contract is first executed • on commencement of construction, or • when a claim for payment is first filed. • What must be done to perfect a lien? • Typically, a lien must be perfected by filing the underlying claim within a certain amount of time after the work has been performed or the service provided. • How much time is allowed to foreclose a perfected lien? • Varies from jurisdiction to jurisdiction. Donald J. Weidner

Summary of Major Concepts (cont’d) • As of what time does the perfected lien take priority? • A. Commencement of Construction, or • B. Filing of a Notice of Commencement of Construction • The Uniform Construction Lien Act (similar to Florida) requires the owner to file a “Notice of Commencement” prior to the beginning of work. • If a lien claimant subsequently records a lien, the priority of that lien is as of the date of the recording of the Notice of Commencement. Donald J. Weidner

Undisbursed or Wrongly Disbursed Funds • A subcontractor may not be able to recover if the property is exhausted by liens that have first priority • such as a construction loan mortgage or a purchase money mortgage. • Equity might help the subcontractor in certain situations by imposing a lien on undisbursed loan proceeds if special circumstances can be shown. • Some states provide a “stop notice” remedy that gives a subcontractor priority as to undisbursed loan proceeds if the construction lender continues to disburse money after notice of a subcontractor’s claim. • An owner or lender who disburses money after receiving a “Stop Notice” or “Notice to Owner” must comply with local law or run the risk of losing lien priority • It may be possible to pay some lienors while getting releases from them Donald J. Weidner

Undisbursed or Wrongly Disbursed Funds (cont’d) • Some states say that the Mechanics Lien (Construction Lien) Act preempts the area and precludes courts from fashioning common law or equitable remedies. • Wrongful disbursal of funds can result in the lender’s loss of priority as against a construction lien claimant just as it can as against a subordinator • The same considerations apply as in the case of a priority fight between a construction lender and a subordinator • including whether the optional vs. obligatory distinction applies Donald J. Weidner

Undisbursed or Wrongly Disbursed Funds (cont’d) • Compare Seitz (Text p. 745) • “The lien of a deed of trust securing a construction loan has priority over mechanics’ and materialmen’s liens only to the extent that: • the funds disbursed actually went into the construction, or • to the extent that the construction lender used reasonable diligence in disbursing the construction loan.” Donald J. Weidner

Partial Recap • In many states, the term “general contractor” is not used in the construction lien statute. Rather, a “contractor” is defined as someone in privity with the owner • Florida uses the privity concept • Lienors in privity can recover on their contract with the owner • The owner’s liability to lienors who are not in privity with it (subcontractors) can often be summarized as follows: Contract Price Minus: Proper Payments (at least those prior to “Stop Notice”) Minus: Reasonable Cost to Complete (upon “abandonment”) Equals: Extent of owner’s liability to all non-privity lienors. Donald J. Weidner

J.I.Kislak Mortgage Corp. v. William Matthews Builder, Inc.(Text p. 679) • Developer and Construction lender entered into a construction loan agreement • Developer executed a construction loan note and mortgage • Construction lender recorded the mortgage • Construction lender’s draw inspector fraudulently authorized progress payments for work that was not done • Some subcontractors were fully paid • Masonry subcontractor was paid nothing • Construction lender was not repaid, filed to foreclose on its construction loan mortgage. • Masonry subcontractor intervened in the foreclosure, asserting that its mechanics’ lien should be considered prior to the lien of the construction loan mortgage. Donald J. Weidner

Kislak Mortgage (cont’d) • “In the usual case it is apparent that a mortgage lien would take priority over a mechanics’ lien that was filed after the effective date of the mortgage provided none of the work covered by the mechanics’ lien was done prior to the recording of the mortgage.” • “However, there is an exception to the rule which applies when a construction loan agreement covering a construction mortgage provides for progress payments over a period of time and some of the disbursements are voluntarily made at a time subsequent to the effective date of the mechanics’ lien.” Donald J. Weidner

Kislak Mortgage (cont’d) • “Where a mortgage is recorded prior to the time that a mechanics’ lien attaches to the property and it is optional with the mortgagee as to whether a further advance is to be made, and where the mortgagee has made an advance with knowledge of the fact that the mechanics’ lien has already attached, to the extent of such later advances, the mortgage is inferior to the mechanics’ lien. • Even though the lender “did not have actual notice of attachment at the time that the advancements were made” • The lender was “charged with knowledge of the law that mechanics’ liens relate back” Donald J. Weidner

Kislak Mortgage (cont’d) • “As between a subcontractor which did not have the protection of a construction loan agreement and a mortgage lender which did not avail itself of the protection it had under the agreement it is not inappropriate . . . that the mortgage lender bear the loss.” • Note, in this case, the lender did not even ask for receipts when it made the voluntary payments. Donald J. Weidner

Florida Statute on Mortgages for Future Advances (Supp. P. 76) 697.04 Future advances may be secured. -- • “(1)(a) Any mortgage or other instrument given for the purpose of creating a lien on real property, or on any interest in a leasehold upon real property,may, and when so expressed therein shall, secure not only existing indebtedness, but also such future advances, whether such advances are obligatory or to be made at the option of the lender, or otherwise, as are made within 20 years from the date thereof, to the same extent as if such future advances were made on the date of the execution of such mortgage or other instrument . . . . Such lien, as to third persons without actual notice thereof, shall be valid as to all such indebtedness and future advances from the time the mortgage or other instrument is filed for record as provided by law.” Donald J. Weidner

Depreciation of Tenant-Constructed Improvements: The Background Rules • In a tax on income: match receipts with the cost of generating those receipts. • A landlord must capitalize the cost of obtaining a tenant and amortize that cost over the life of the lease (See text p. 783). • That is, the landlord is not permitted to expense (currently deduct) all of the cost of obtaining a tenant because it will generate receipts for years. • The landlord must attribute a portion of the cost to each year’s rent receipts Donald J. Weidner

Depreciation of Tenant-Constructed Improvements (cont’d) • Similarly, bonus payments by a tenant to acquire a lease can not be deducted by the tenant; • They are treated as a cost of acquiring the lease and must be capitalized (added to the cost of the asset—the lease) and then amortized over each year of the life of the lease. (See Text p. 784). • However, a tenant’s payment of advance rent to a landlord at the acquisition of the lease is taxable to the landlord when the landlord receives it. (See Text p. 784). Donald J. Weidner

Depreciation of Tenant-Constructed Improvements (cont’d) • Tenants often construct buildings on land that they lease. • If a tenant invests in a building that is • used in its trade of business or • held for the production of income, it is allowed to recover its investment in the building through depreciation (“cost recovery”) deductions. (See Text p. 784). Donald J. Weidner

Write-offs Available to Tenants Who Construct Improvements • In short, a tenant may be doing all of the following: • amortizing its investment in a lease • deducting the rent it is paying under the lease and • depreciating its investment in the building it constructs on the leased land. Donald J. Weidner

Pays $800,000 Conveys tract of land Chirelstein: Tenant-Constructed Improvements as Rent NFO LL FO 20 year ground lease MFG T T to pay relatively low annual rent T to construct factory at minimum cost of $1,000,000 Factory to become property of LL on termination of the lease [“thus…apparently… a form of ‘rent in kind’.”] Constructs building T With 25 year U.L. (5 years longer than the lease) That has an expected depreciated value of $200,000 at the time the 20-year lease expires Pays relatively low annual Cash Rentals LL T Donald J. Weidner

General Considerations In defining income, Glenshaw Glass emphasized a “realized” disposable increase in wealth: • “Here we have instances of undeniable accessions to wealth, clearly realized, and over which the taxpayers have complete dominion.” • Is the factory building “income” to the Landlord? Is it an • “accession to wealth,” • “clearly realized,” • “over which the taxpayer has complete dominion”? • If it is income, when are these criteria met? • If it is income, in what amount? Donald J. Weidner

The Realization Requirement • Chirelstein: “because the realization requirement exists, the income tax is a tax on transactionsinstead of being a tax on income in the economic sense.” • There are four possible answers to the question of when a tenant-constructed building is income to the landlord. It can be taxed as either • prepaid rent • prorated rent • postpaid rent or • no rent at all Donald J. Weidner

Possibility # 1: Prepaid Rent • Possibility #1: The Landlord receives Prepaid Rent in the year in which the building is constructed. • How much rent? • The present value of the right to get the building at the end of the lease term. Assume the building is expected to be worth $200,000 at the end of 20 years. • reduce that $200,000 payment at the end of year 20 to its present value. • Using an 8% discount rate, the present value is about $50,000. • If you report the present value of the future payment in income at the beginning of the lease, you could consider the transaction closed at this point, with nothing further to report when the lease ends. • That is, report $50,000 income now, no further income later. Donald J. Weidner

Possibility # 1: Prepaid Rent (cont’d) • As soon as the landlord reports the building in income, the landlord receives a $50,000 basis in it. • Sometimes referred to as a “tax cost basis” • Landlord’s basis in the building at the termination of the lease at the end of year 20 would be $50,000, the amount previously included in income. • Landlord’s depreciation deductions for the last five years of the building’s useful life (after the lease expires), on a straight-line method, would be: $50,000/5 = $10,000 per year. • Note: To implement this prepaid rent approach, there must be a prediction of the value the building will have at the end of 20 years. Donald J. Weidner

Possibility # 2: Prorated Rent 2. Possibility #2: The Landlord receives rent that is prorated over the life of the lease. • How much rent? • The anticipated value of the building at the end of the lease term, $200,000. • When? • Include some of the building’s value in income for each year of the lease. Ex., $10,000 for each of 20 years. $10,000 X 20 = $200,000. • Landlord’s basis in the building on termination of the lease would be $200,000—the amount previously included in income (a “tax cost basis”). • Landlord’s depreciation for the remaining 5 years of useful life after the lease expires: $200,000/5 = $40,000 per year (using a straight-line method of computing depreciation). • The Prorated Rent approach requires, as did the Prepaid Rent approach, a prediction of the value of the building at the end of the 20 year lease term. Donald J. Weidner

Possibility # 3: Postpaid Rent 3. Possibility #3: The Landlord receives Postpaid Rent. • When is the income realized? • At the end of the 20 year lease, when the Landlord’s reversion in the building becomes possessory. • How much rent? • The fair market value of the building when the lease terminates. • If the building’s actual value turns out to equal the anticipated value, that amount is $200,000 in this hypothetical. • Landlord’s basis in the building would be $200,000, the amount included in income. • Again, a “tax cost basis” • Landlord’s depreciation deduction for each of the remaining 5 years of the building’s useful life: $200,000/5 = $40,000 per year. Donald J. Weidner

Postpaid Rent (cont’d) • The Postpaid Rent alternative has the advantage in that it does not require an initial estimate of the value at the end of 20 years. • But it still requires an appraisal of the property at the end of the lease. • The Postpaid Rent alternative is the approach the first IRS regulations took: that the expiration of the lease was the landlord’s realization event. • When the landlord’s reversion in the building became possessory. • The courts initially rejected this approach. Donald J. Weidner

Pre-Helvering v. Bruun • Cases prior to Bruun held that there was no taxable realization to the lessor either • when the leasehold improvements were installed by the tenant or • when the improvements vested in the lessor at the expiration of the lease. • The idea was that the building could not be severed and disposed of separately from the land, and thus was not “portable and detachable” unless it was torn down and scrapped. • Another way of stating the notion is that “profit” must be severed from “capital” to be taxed. • The realization requirement turns what might have been a tax on economic enhancement in wealth into a tax on transactions. Donald J. Weidner

T defaulted Helvering v. Bruun309 U.S. 461 (1940) LL Leased lot & building for 99 years T 1915 T may, on giving bond to secure 2 years’ rent, remove or tear down any bldg. On termination of the lease, T to surrender all land, buildings, and improvements T Removed existing buildings and constructed a new bldg with a UL of 50 years. [85 years left on the lease] 1929 [nonpayment of rent & taxes] LL 1933 LL regained possession of land and building } FMV building constructed by T is $64,000 LL’s “unamortized cost” of old bldg. is 13,000 “Net FMV” [net “gain” $51,000 as at 7/1/33, says IRS] stipulation Donald J. Weidner

Bruun and Its Aftermath: From Possiblility # 3 to Possibility # 4 • Bruun agreed with the IRS and held that there was income to the landlord when the tenant defaulted and the landlord’s reversion became possessory (Possibility #3). • One might ask what would happen if, upon the tenant’s default, the value of the land had decreased. • Would the landlord have been allowed a deduction? • Congress reversed Bruun by enacting sections 109 and 1019 • thus adopting Possibility # 4. Donald J. Weidner

Possibility #4: No Rent 4. Possibility # 4: The Landlord has No Rent At All from the Building Constructed by the Tenant. • The building is treated as unrealized appreciation that is not taxed as “rent” at any time. • With nothing included in income, the landlord’s basis in the building at the expiration of the lease is zero. • Because the landlord’s basis in the building is zero, the landlord gets no depreciation deductions during the remaining useful life of the building. Donald J. Weidner

Sections 61, 109 and 1019 in A Nutshell • Sec. 61 regulations provide that, if a tenant pays any of the landlord’s expenses, the payments are additional rental income to the landlord. • Further, if a tenant places an improvement on the real estate that is a substitute for rent, the improvement is additional rental income to the Landlord. • The test for whether it is rent is the intent of the parties. Donald J. Weidner

Sections 61, 109 and 1019 (cont’d) • Sec. 109 states that, on termination of a lease, the landlord does not have income on account of the value of an improvement erected by a tenant (See Text p. 784, Supp. P. 144). • The regulations provide: • “However, where the facts disclose that such buildings or improvements represent in whole or in part a liquidation in kind of lease rentals, the exclusion shall not apply to the extent that such buildings or improvements represent such liquidation.” • This regulation has never been vigorously enforced. Donald J. Weidner

Sections 61, 109 and 1019 (cont’d) • Sec. 1019 is a basis rule that is consistent with the Section 109 exclusion of what could otherwise be seen as income. • Section 109 states that there is no income and Section 1019 states that, as a consequence, there is no basis increase (no tax cost incurred, hence no “tax cost basis”). (Supp. P. 144). Donald J. Weidner

World Publishing Co. v. Commissioner(Supplement p. 145) Net lease for 50 years OFO T 1928 Tenant to pay annual rental averaging $28,500 Tenant required to construct a 6 story or more building of cost of at least $250,000 Building to become part of the realty on construction. Tenant agrees to subordinate to a mortgage up to a stated percentage of ground value. 1950 Sold all its interest Taxpayer: WORLD PUBLISHING NFO $700,000, subject to the lease to T, which had 28 more years to run ACCEPTED: The FMV of the land alone was $400,000. QUESTION: What did TX, the New Fee Owner, buy for the extra $300,000? STIPULATED: When the NFO, World Publishing Co., purchased whatever it purchased, the remaining useful life of the building “was not greater than the unexpired term of the lease.” That is, the remaining useful life of the building was equal to, or shorter than, the remaining term of the lease. Donald J. Weidner

World Publishing (cont’d) • Is there anything facially confusing about NFO’s claim for “Depreciation and Amortization?” • Recall, a depreciation deduction is only available if the property is • used in a trade or business, or • held for the production of income. • IRS position is: NFO has merely a reversionary interest, which may not be depreciated. • The person claiming a depreciation deduction must have something akin to a substantial present possessory interest. • The IRS argued this in Bolger Donald J. Weidner

World Publishing (cont’d) • Blackmun rejected the argument that NFO did not have a sufficient possessory interest. • Consider the analogy of a building constructed by a landlord and then leased: • “Where an owner of land erects a building on it and then leases it, he is still entitled to recover the cost of the improvement by depreciation deductions.” • Even though the present possessory interest in the building is in the tenant. • Thus, the normal landowner/building owner is not required to have a present possessory interest in a building to depreciate the landdowner/ building owner’s investment in it. • The facts of the particular tenant constructed improvement matter: • Here, taxpayer “clearly owned the building in more than a bare-legal-title sense.” Donald J. Weidner