Download

1 / 25

250 likes | 384 Vues

From Perfect Competition to Total Monopoly A Spectrum. Who sets the price?. The market does. Price setting is a complex issue and is a function of the type of competition prevailing in the market. There is a spectrum of types of competition:. Perfect Competition.

E N D

From Perfect Competition to Total Monopoly A Spectrum

Who sets the price? The market does Price setting is a complex issue and is a function of the type of competition prevailing in the market. There is a spectrum of types of competition: Perfect Competition Monopolistic Competition Oligopoly Monopoly

Those in perfect competition have NO control over the price Perfect Competition In perfect competition there are many sellers, each supplying a small part of the industry’s output. None has a dominant position. Another feature of perfect competition is that products of an industry with a market structure of perfect competition must be standardized, that is they would produce identical or indistinguishably similar products. There are not many industries that are under perfect competition, examples might be agriculture

Those in monopolistic competition have some control over the price Monopolistic Competition In a monopolistically competitive industry, there are also many sellers. Like in the case of perfect competition, here also no one firm or seller can dominate and each services a small segment of the market demand. In a monopolistic competitive environment firms make similar and largely substitutable but not identical products, that is they would produce distinguishably similar products. Many industries are under monopolistic competition, examples might be retail trade or clothing manufacturing.

Those in an oligopoly have some control over the price Oligopoly In an oligopoly, there are a few sellers. Like in the case of perfect competition, here also no one firm or seller can singly dominate and each services a segment of the market demand. Oligopolies produce similar or differentiated products Oligopolies are the most dominant form of market structure, examples range from OPEC to computer hardware or software manufacturing, or private education

Those in a monopoly have considerable control over the price Monopoly In a monopoly, the industry consists of a single seller who dominates the market Monopolies produce one product by definition There are not very many absolute monopolies. There may be at times monopolies or structures approaching one in a given precisely defined market segment or location. For example public utilities, or the cable company in your region.

Market Price Under Perfect Competition In perfect competition, market price is set purely by market demand and supply. The price is set at the equilibrium point (or region). This is where the supply curve and the demand curve will intersect. Demand curve of the industry: The demand curve of the entire industry is a typical downward sloping demand curve.

Market Price Under Perfect Competition Demand curve of an individual seller: In contrast, the demand curve of an individual seller is nearly horizontal. WHY? Because there is near perfect product substitutability. The slope of the curve will be proportional to the “influence” a seller has on the market which in the case of perfect competition is not much at all.

Market Price Under Perfect Competition Price fluctuations are purely a function of supply and demand curve shifts Demand curve shifts when there is a change in: Supply curve shifts when there is a change in: • Income • Consumer taste • Product quality • Production Technology • Input prices • Environment (e.g. weather)

Output Decision Under Perfect Competition The seller may not set the price but they can decide how much to supply. Note that any one firm can decide how little or how much to sell and their decision will not impact the market price but will impact their own revenue Maximizing profit We know that MR=MC for profit (Π) to be optimized. As such Note: the seller cannot set the price but can set the marginal cost or the quantity Therefore:

Output Decision Under Perfect Competition This is not the end of the story – however: For the condition leading to MC=P to suggest a maximum, the following fact must be satisfied: or As such: Since MR=P and does not change with Q, so for maximization we also must have: or

This means that under perfect competition, even if a firm is doing its best, it may not earn a profit At P0 the firm will produce X ATC MC At P2 the firm will produce Y. This will not produce profit but the loss is less if they produce than if they shut down Price per unit P0 At P3 the firm might as well cease production because the firm loses a fixed cost whether they produce or not, so they might as well not produce P2 AVC P3 P1 At P1 the firm must cease production because neither variable or fixed cost is being recovered adequately Q Z Y X Shutdown point

Example: Fisheries Co. has a total cost function as follows: If the market dictated price is P=$16 per ton, should they stay in business? Therefore: So they should continue to produce

Monopoly Monopolists have considerable power but not absolute reign. Their success is still subject to: • Whether the customer wants their product. The customer may have no choice from whom to buy, but always has the choice to not buy at all. • Whether the customer would buy something else. Please note that whilst in perfect competition the product is standardized and perfectly or nearly so substitutable, the converse is not true in a monopoly. In a monopoly, the seller is the only seller of X in the market but there may be someone else selling Y which whilst is not X can stand in for it. • Need to control costs. Even if there is great demand, supply has to be adequately efficient. • Government or social regulation

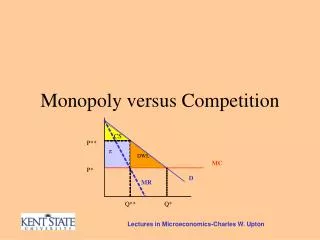

Output and Price Decision Under Monopoly An unregulated monopolist can choose price and output quantity in such a way that MC=MR. Doing so will give a maximum profit point. Unlike the case of perfect competition where the price was forced to P=MC=MR, in this case MR is not a constant as neither price nor quantity need to remain fixed. But we do know that in all cases: Where η is price elasticity of demand. Rearranging, we have:

However we know that as η < 0, will always be negative As such MR must always be less than price P. Or price must always be greater than marginal revenue. Also, it is natural and economic behavior that managers seek to operate when MR >0. But if MR>0, then from we have that η < -1 otherwise will be larger than P and MR will be forced negative. A monopolist WILL NOT produce in the inelastic range of its demand curve if it is maximizing profit.

Similarly as MR=MC for profit maximization, then: since η < 0 then or: which means that the price must exceed marginal cost. ATC AVC PM Demand MR QM

Example: Franchise war Franchiser makes its money from collecting a percentage of each store’s sales (or total revenue). Franchisee makes its money from profit. Franchiser wishes to maximize total revenue. It does so by forcing the franchisee to sell more burgers even when not profitable. i.e when MR≠MC and by opening more stores Franchisee wishes to maximize profit: that is operate at MR=MC for the store.

Maximizing profit for the store will require: Price Demand MR MC Maximizing total revenue will require: Pee Per Quantity Qee Qer

Cost Plus Pricing Monopolists often price their products by simply adding a fixed amount to their cost. This method is called Cost Plus pricing The fixed amount added is often called profit margin or markup. What should be your markup? The markup is often not arbitrary and is instead usually a percentage of cost and is added to the estimated average cost. or

Some firms set a target rate of return which in turn determines the markup. Under such conditions, the price is set equal to: We can also analyze C: Where: C is production cost L is unit labor cost M is unit materials cost Kis the unit marketing cost AFC is the average fixed cost Where: P is price C is production cost A is total gross operating assets πis the desired total profit on those assets

Does Cost Plus Pricing Maximize Profit? Not Necessarily but it could Recall that: Rearranging: On the other hand: Combine and rearrange:

Case Study: Capture Inc. is the sole supplier of commodity X in several regions. X sells for $27 a ton in the Northeast region Costas Megalodrachmas is the owner of the monopoly operation. In a recent statement he said; “people in the Midwest are very price-conscious and our managers there know what to charge”. • Are the demand curves in the two regions mentioned the same? If so why, If not how do they differ? • CM also said that; “our labor costs are higher in the NE and is almost double that of the MW”. Is the marginal cost for X the same in the NE and the MW? • Why is the price higher in the NE? • If marginal cost is 20% higher in the NE, and the price elasticity of demand is -3 in the NE and -4 in the MW, what would be the price in the MW?

Are the demand curves in the two regions mentioned the same? If so why, If not how do they differ? Demand curves are different. The demand curve is more price elastic in the MW. A 1% price change will reduce demand by a larger percentage. B. Is the marginal cost for X the same in the NE and the MW? No. The marginal cost is lower in the MW. C. Why is the price higher in the NE? We know that As MC is higher and η is less elastic in the NE, the profit maximizing price is higher in the NE

D. If marginal cost is 20% higher in the NE, and the price elasticity of demand is -3 in the NE and -4 in the MW, what would be the price in the MW?