Download

1 / 32

341 likes | 825 Vues

Measuring the economy and the circular flow. Topics. National income accounts Expenditure approach to GDP Income approach to GDP Circular Flow of income and expenditure Leakages and injections Inflation and consumer price index. National Income Accounts. Gross domestic product -- GDP

E N D

Topics • National income accounts • Expenditure approach to GDP • Income approach to GDP • Circular Flow of income and expenditure • Leakages and injections • Inflation and consumer price index

National Income Accounts • Gross domestic product -- GDP • Measures the market value of all final goods and services produced during a year by resources located in domestic economy, regardless of who owns those resources • Gross national product -- GNP • Measures the market value of all goods and services produced by resources supplied by domestic residents and firms, regardless of the location of the resources • National income accounts • One person’s spending is another person’s income • Aggregate output is recorded on one side of the ledger and income created by that spending on the other side

GDP 1. GDP can be measured either by total spending on production or by total income received from that production: Expenditure approach • Adds up spending on all final goods and services produced in the nation during the year Income approach • Adds up all payments for resources used to produce output in the nation during the year 2. Includes only final goods and services • Goods that are sold to the final, or ultimate, user • Ignores most of the secondhand value of used goods because these goods were counted in GDP the year they were produced

GDP 3. Intermediate goods and services are those purchased for additional processing and resale • Excluded to avoid the problem of double counting which is counting an item’s value more than once 4. Main components in the GDP a. Consumption b. Investment c. Inventories d. Government purchases f. Net Export

GDP – Expenditure Approach: • Consumption - Personal consumption expenditures: consist of purchases of final goods and services by households during the year • Investment - Gross private domestic investment: consists of spending on new capital goods and additions to inventories • Spending on current production that is not used for current consumption ( such as physical capital [new buildings and machinery purchased by firms to produce goods and services],purchases of new residential construction and inventories) • Inventories: stocks of goods in process and stocks of finished goods. Help firms deal with unexpected changes in the supply of their resources or in demand for their products (Net changes in inventories)

Government purchases - Government consumption and gross investment: spending by all levels of government for goods and services • Excludes transfer payments because they are an outright grant from the government to the recipient • Net Exports: arise from interaction between the domestic economy and the rest of the world • Equals the value of U.S. exports of goods and services minus the value of U.S. imports of goods and services • Includes merchandise trade and and services – invisibles

GDP: Expenditure Approach • Expenditure (spending) approach: divide aggregate expenditure into its four components: • Consumption • Investment • Government Purchases • Net Exports (exports [X] minus imports [M]) C + I + G + (X – M) = Aggregate expenditure = GDP

GDP: Income Approach • Adds up all income payments for resources used to produce output in the nation during the year :compensation of employees (wages and salaries) net interest rental income corporate profits proprietors’ income • Aggregate expenditure = GDP = Aggregate income • Avoid double counting by including only the market value of goods or by calculating the value added

Computation of Value Added for a New Desk The value added by each firm equals the firm’s selling price minus the amount paid for inputs from other firms. The value added at each stage represents income to individual resource suppliers at that state Cost of Sale Intermediate Value Stage of Value Goods AddedProduction (1) (2) (3) Logger $ 20 $ 20 Miller 50 $ 20 30 Manufacturer 120 50 70 Retailer 200 120 80 Market Value of Final Good $200 The sum of the value added at all stages equals the market value of the final good and the value added for all final goods and services equals GDP based on the income approach

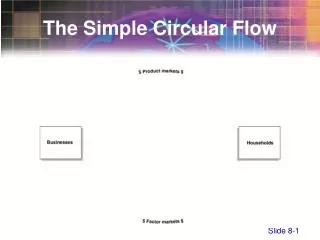

Income, Expenditure and the Value of Production • To see that for the economy as a whole, income=expenditure=production we need to study the circular flow of income and expenditure • Economy consists of 4 sectors: Households Firms Governments The rest of the world

Example: Malaysia National Accounts (millions of Ringgit) Source: International Monetary Fund (IMF): International Financial Statistics Yearbook (2004)

Households and Firms • a. Households sell and firms buy the services of labor, capital, land and entrepreneurship in the resource markets. For these resources services, firms pay income (Y) to households such as wage, interest, rent, profit • b. Firms sell and households buy consumer goods & services in the goods markets. The payment households make for these goods is called consumption expenditure ( C ) • c. Firms also buy and sell new capital equipment in the goods market (e.g. IBM sells PCs to General Motors). The purchase of new plants, equipment and buildings and additions to inventories are investment (I) • d. Firms finance their investment by borrowing from households’ saving in the financial markets • Thus income is payment for the services of resource and expenditure is a payment for goods or services

2. Governments • Government buy goods & services – government purchases from firms (G) • Government use taxes (T) to pay for their purchases • When government purchases exceed net taxes – budget deficit – to finance it the government borrow from financial markets 3. Rest of the world • Firms export goods & services to the rest of the world and import goods & services from rest of the world • Net Exports (NX) = Exports (X) – Imports ( if X > M, net exports positive and vice versa)

The Circular Flow of Income and Expenditure Households’ saving Households taxes Government Income Consumption expenditure G borrowing G Goods markets Financial markets Resource markets Net exports Investment expenditure Foreign borrowing Income C Rest of the world G Net exports Firms Firms’ borrowing

Leakages Equal Injections • Leakage – any diversion of income from the spending stream; includes saving, taxes and imports • Injection – any spending other than households: investment, government purchases, exports and transfer payments • This first accounting identity leads to • Y + NT = C + I + G + (X – M) • Since income equals consumption plus saving, we can substitute C + S for Y in this equation • C + S + NT = C + I + G + (X – M) • After subtracting C from both sides and adding M to both sides, the equation reduces to • S + NT + M = I + G + X • Thus, the leakages (S, NT, and M) must equal the injections (I, G, and X) into the circular flow

Planned versus Actual Investment • Planned Investment • The amount firms plan to invest before they know how much output they sell • Actual Investment • Includes both planned investment and any unplanned changes in inventories • Unplanned increases in inventories cause firms to decrease their production next time around • Only when there are no unplanned changes in inventories will GDP be at an equilibrium level planned investment equals actual investment

Limitations of National Income Accounting 1. Some production is not included in GDP • GDP includes only those products that are sold in markets • Ignores “do-it-yourself” household production an economy in which householders are largely self-sufficient will understate GDP • Ignores the underground economy • All market activity that goes unreported because it’s illegal or those involved want to evade taxes

2. GDP Ignores Depreciation • In the process of producing GDP, some capital wears out or becomes obsolete • A truer picture of the net production that actually occurs during a year is found by subtracting this depreciation from GDP • Depreciation measures the value of the capital stock that is used up or becomes obsolete in the production process

3. GDP Does Not Reflect All Costs • Some production and consumption degrades the quality of our environment- pollution of lakes and rivers, mass clearing of forests, depletion of exhaustible resources • These negative externalities are largely ignored in GDP accounting

Real versus Nominal GDP • i. Nominal GDP : Gross domestic product measures the value of output in current prices Since the economy’s average price level changes over time, current-dollar comparisons across years can be misleading. Specifically, nominal GDP can increase over time because • Output increases • Prices increase • Both of these occur • ii. Real GDP refers to GDP adjusted for changes in prices the production of goods and services valued at constant prices.

The GDP Deflator or GDP Price Index Measures the current level of prices relative to the level of prices in the base year. Reflects the prices of goods & services but not the quantities produced GDP Deflator or GDP Price Index = Nominal GDP X 100 Real GDP

The Consumer Price Index (CPI) • Is a measure of the overall cost of the goods and services bought by a typical consumer. • A base year is used as a point of reference to compare the prices in other years prices in other years are expressed relative to the base-year price • Price index constructed by dividing each year’s price by the price in the base year and multiplying by 100

Example: Calculating the Consumer Price Index and the Inflation Rate

Problems with the CPI • The goal of CPI is to measure changes in the cost of living – however it is not a perfect measure of the cost of living • There are 4 main sources of bias in the CPI: i. substitution bias ii. Introduction of new goods (new goods bias) iii. Unmeasured quality change (quality change bias) iv. Outlet substitution bias

Substitution bias Changes in relative prices lead consumers to change the items they buy. E.g. changes in the price of sources of protein. If price of fish rises and the price of chicken remains unchanged, people buy more chicken and less fish. Because the CPI ignores the substitution it says the price of protein has increased when actually it is constant (same amount of protein)

New goods bias New goods keep replacing old goods E.g. PCs and typewriters – if we want to compare the price level in 1998 with that in 1978 – compare the price of PCs now and that of a typewriter in 1978 Because PCs are more expensive than typewriters, the arrivals of new goods puts an upward bias into CPI and its inflation rate

Quality change bias Many goods are highly improved from year to year – CDs, cars, computers, etc. Part of the rise in the prices of these items is a payment for improved quality and is not inflation But CPI counts the price rise as inflation and so overstates inflation

Outlet substitution bias When confronted with higher prices, people use discount stores more frequently and convenience stores less frequently This is called outlet substitution. The CPI do not monitor outlet substitutions.