Download

1 / 20

200 likes | 287 Vues

Explore the U-3 and U-6 unemployment rates, and delve into the four prominent theories explaining the yield curve's shape in the financial market. Learn about Operation Twist, default risk, bond ratings, and call and put options.

E N D

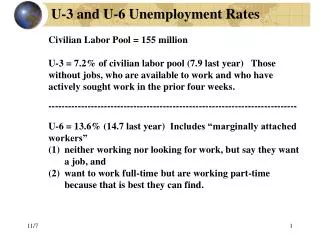

U-3 and U-6 Unemployment Rates Civilian Labor Pool = 155 million U-3 = 7.2% of civilian labor pool (7.9 last year) Those without jobs, who are available to work and who have actively sought work in the prior four weeks. ---------------------------------------------------------------------------- U-6 = 13.6% (14.7 last year) Includes “marginally attached workers” neither working nor looking for work, but say they want a job, and want to work full-time but are working part-time because that is best they can find.

Four Theories Four prominent theories used to explain the shape of the yield curve. Expectation theory Liquidity premium theory Market segmentation theory Preferred habitat theory

(1) Expectation Theory Says… • Shape of yield curve determined by expectations about future rates. Changes in expectations cause changes in the yield curve. • Assumes investors are indifferent between a long-term security and a series of short-term securities.

Term Structure Formula • Long-term interest rates are the geometric average of current and future period rates. where: R observed market rate f forward rate nmaturity of bond prescript time at which period starts (0 is “now”) subscript length of period

Implied 1-Year Forward Rate Formula Implied forward rate for the n-th period coming up • Example of how to apply: • Want implied yield of a 1-year security that starts 6 years from now. • Look up yields on 6-year security and 7-year security. • Use formula above with n= 7.

Example 3: Calculating Forward Rates Assume following Treasury security quotes: Find the 1-year implied forward rates during nth period (where n = 2,3,4,5)

Example 4: Using Formula Using find the 1-year implied forward rate during 3rd year 1-year Treasury bill 1.9% 2-year Treasury note 2.4% 3-year Treasury note 2.7%

(2) Liquidity Premium Theory Says… • Long-term securities have greater price risk, and generally less marketability. • Liquidity premiums contribute to an upward tendency of a yield curve.

(3) Market Segmentation Theory Says… • Market participants may have strong preferences for particular maturities, and buy and sell securities consistent with these preferences. • Can theoretically lead to discontinuities in yield curve.

(4) Preferred Habitat Theory Says… • Preferred Habitat Theory (an extension of Market Segmentation Theory) allows market participants to trade outside of their preferred maturities if adequately compensated. • Preferred Habitat Theory allows for humps in the yield curve.

Operation Twist “Operation Twist” is the nickname for the Fed’s 2011-12 initiative of buying longer-term Treasuries and simultaneously selling some of the shorter-dated issues it already held in order to bring down long-term interest rates.

Why Not Only Short-Term Debt? Q. Why not finance long-term needs by continually refinancing short-term debt? A. Firms do more of this than they should. There will always be periods when can not roll over. Then need a bailout (like Fed had to do in 2008-09).

Which Theory is Right? • Each has its point. • Day-to-day changes in the term structure are most consistent with the Preferred Habitat Theory. • Many economists also feel that expectations and liquidity premiums are important in determining the yield curve.

Default Risk • Investors require a default risk premium. • DRP = i – irf> 0 • Investors satisfied when feel that DRP offsets expected default loss. • Default risk premiums tend to increase in periods of recession (when people scared) and decrease in periods of economic expansion (when people overconfident). • “flight-to-quality” • Bond ratings are only for default risk.

Bond Ratings Fitch, too

NRSROs • Nationally Recognized Statistical Rating Organizations • NRSROs are credit-rating agencies authorized by the SEC and banking regulators. Currently 10 (best known Moody’s, Standard & Poor’s, Fitch). • BBB- (Baa3) and above are investment-grade, below are speculative-grade or “junk.” • Issuers pay to have their bonds rated. Banks, insurance companies, pension funds, many mutual funds can only hold investment-grade bonds. • As conditions change, rating agencies change their ratings. Bad when an issue’s rating drops below cutoff.

Default Rates Bond default history when initially rated: AAA 0.52% AA 1.31 A 2.32 BBB 6.64 BB 19.52 B 35.76 CCC 54.38 History with recent mortgage securities entirely different. The agencies also rate commercial paper (discussed elsewhere).

Call Options • A call option permits the issuer (borrower) to call (refund) the obligation before maturity. • Borrowers will “call” if interest rates decline. • Investors in callable securities bear the risk of losing their high-yielding security. • investors demand a call interest premium. • CIP = ic – inc > 0

Put Options • A put option permits the investor (lender) to terminate the contract at a designated price before maturity. • Investors are likely to “put” their bond back to the borrower during periods of high interest rates. • The difference in interest rates between putable and nonputable contracts is called the put interest discount. • PID = ip – inp < 0

Conversion Options • A conversion option permits the investor to convert a security contract into another security • The conversion yield discountis the difference between the yields on convertibles relative to nonconvertibles. • CYD = icon – incon < 0

![[u] [u:] [ou]](https://cdn4.slideserve.com/8524074/slide1-dt.jpg)