Download

1 / 20

200 likes | 328 Vues

Comments on “Flexible Inflation Targeting & Financial Stability: Is It Enough to Stabilise Inflation and Output?”. Andrew Filardo Bank for International Settlements. The Architecture of Financial System Stability: From Market Micro Structure to Monetary Policy 24-26 May 2006, Capri, Italy.

E N D

Comments on “Flexible Inflation Targeting & Financial Stability: Is It Enough to Stabilise Inflation and Output?” Andrew Filardo Bank for International Settlements The Architecture of Financial System Stability: From Market Micro Structure to Monetary Policy 24-26 May 2006, Capri, Italy 1

Related Policy Issues • Asset prices and monetary policy • Monetary stability and financial stability • Very important policy issues that demand greater research efforts – not just a Norwegian problem 2

Related Policy Issues Emerging market economies 3

The Pros Making progress • Explicit consideration of financial stability and monetary stability considerations for central banks • Larger set of equations – more realistic policy model! • “Calibrated” model of the Norwegian economy 4

The Cons Making progress??? • What should policymakers make of these results? • My remaining comments raise doubts about whether policymakers can rely with confidence on the “themes” coming from this analysis 5

Modeling Approach • Monetary policy loss function • Macro-financial set of 8 equations: • output, inflation, housing, shares, FX, Unemp, wages, credit • Monetary policy – augmented Taylor rules 6

If it were only that easy! Deep modeling issues: CB loss function • “Second generation” loss function – is it enough? • First generation - var(r)? Second generation V(f) Not clear that this is exactly what we mean by financial stability Not exactly sure what is going on with f in the model 7

If it were only that easy! Deep modeling issues: CB loss function • What do we mean by financial stability for CBs? • Low probability meltdowns • Japan-like situation where system short-circuits • The nonlinear interactions are surely the key ones • What is the ultimate source of externality or market failure? What justifies government intervention? And, is the central bank the obvious “stabiliser of first resort”? 8

If it were only that easy! Deep modeling issues: “Calibrated” models • Macro-financial model – is it that easy? • Asset prices – misspecification or bubbles? • Should CBs respond? Should CBs prick? Can CBs encourage/discourage bubbles by holding R too low for too long? [Filardo 2004, 2005] 9

If it were only that easy! Deep modeling issues: “Calibrated” models • Macro-financial model – is it that easy? • Asset prices – misspecification or bubbles? • Should CBs respond? Should CBs prick? Can CBs encourage/discourage bubbles by holding R too low for too long? [Filardo 2004, 2005] • Credit growth – monetary or real phenomenon? • Intrinsic shocks & linear stochastic control are key!!! • Cannot simply estimate a set of regression equations to draw robust policy implications!!! 10

If it were only that easy! Deep modeling issues: Ad hoc MP rules • Ad hoc monetary policy – is it sufficient? • Yes, if start with a realistic policy rule. Then, can ask: “Can the central bank do better?” • No, ifcomparing two non-optimal rules. They do not reveal much 11

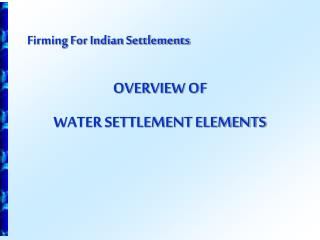

Results for Optimal Policy Optimal Monetary Policy Frontiers ? Variance of inflation Variance of output

If it were only that easy! Deep modeling issues: Ad hoc MP rules • Ad hoc monetary policy – is it sufficient? • Yes, if start with a realistic policy rule. Then, can ask: “Can the central bank do better” • No, ifcomparing two non-optimal rules. They do not reveal much • Other possible issues - • Where is the role for monetary aggregates? thresholds? • Considerations of deflation and ZLB should be added 13

Bottom Line • I like the paper • It makes some progress in thinking about key policy issues … • … but I am not sure that such modeling efforts are ready for prime time … yet! 14

Where Do We Go From Here? Need to backwards before moving forwards! • “Optimal” monetary policy • How do we add financial stability concerns in the “welfare” function of the central bank? • Shock identification and modeling – intrinsic and non-linear aspects • Policy responses – game theoretic aspects • amongst domestic policymakers (eg RBNZ) • multilateral considerations • Decision making under uncertainty – interim solution 15

Thank you! 16

Results for Optimal Policy Optimal Monetary Policy Frontiers Variance of inflation Variance of output

Results for Optimal Policy Optimal Monetary Policy Frontiers Variance of inflation Superior policy Variance of output

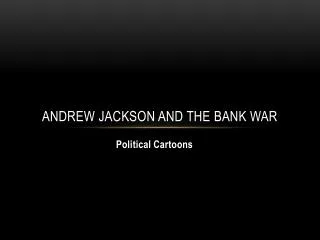

Modeling a Bubble Time-Varying Transition Probability Model Sample Path of a Bubble 15 10 5 0 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 -5 -10 -15 -20 Time periods Not a CAPM model!

Results for Optimal Policy Optimal Monetary Policy Frontiers Variance of inflation Variance of output