Download

1 / 20

200 likes | 345 Vues

Delve into bond price-yield dynamics and interest sensitivity measures like Duration and Convexity. Learn to calculate, interpret, and apply these key metrics to optimize bond portfolio management. Master immunization techniques and overcome its limitations for effective risk management.

E N D

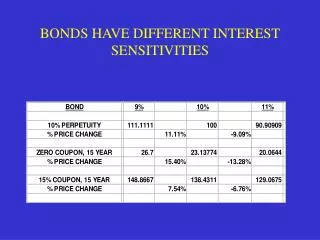

MEASURES OF INTEREST SENSITIVITY • Price Value of a Basis Point (PVBP) Change in bond price given a one basis point change in yield • Yield Value of a 32nd (YV32) Change in yield given a price change of 1/32 • Duration Macaulay: Price elasticity w.r.t. (1+y/2) Modified: % price change given yield change

PROPERTIES OF DURATION • DURATION: • Decreases with coupon rate • Decreases with yield • Usually increases maturity (but watch out for long-term deep discount bonds)

MODIFIED DURATION • Used more in practice because of easier interpretation • Calculate as shown, using closed form solution for DMAC or use built-in Excel function

CALCULATING DURATION • A. Program Closed-Form Solution into a spreadsheet • B. Use Excel functions DURATION and MDURATION (in Analysis ToolPak) • C. Approximate: DMOD (P- - P+)/[2(P0)(y)]

APPLICATION: HEDGING • For our portfolio, given a change in yield, P/P - DMOD(p) y • To hedge the portfolio against yield changes, set DMOD(p) = 0 • This implies: WA = - WB [DMOD(A)/ DMOD(B)]

APPROXIMATING BOND PRICE CHANGES • But what if P/P - DMOD(p) y isn’t a very good approximation? • A better approximation comes from carrying the Taylor’s Series one more term:

WHAT DOES CONVEXITY MEASURE? • Note that convexity is a second derivative measure • It tells us about the degree of curvature in the price-yield relationship

APPROXIMATING CONVEXITY A closed form solution exists, but convexity can be approximated quite accurately by measuring the change in the change in price, given a change in yield (including between coupon dates)

CONVEXITY PROPERTIES • As yield increases, convexity decreases • For a given yield and maturity, as coupon rate increases, convexity decreases • e.g., zeros have greatest convexity among bonds of given yield and maturity • For a given yield and modified duration, as coupon rate increases, convexity increases • e.g., zeros have least convexity among bonds of given yield and DMOD

IMMUNIZATION CAVEATS • The immunization technique protects us only against a small, one-time shift in rates • need to rebalance after yield shifts occur • For portfolios, immunization only works for parallel yield curve shifts • in fact, the yield curve often flattens or steepens • Why not just use zeros to immunize?