Paying Off Simple Interest Installment Loans: A Guide

20 likes | 156 Vues

Understanding how to pay off simple interest installment loans can help borrowers save on interest charges. The Truth in Lending Law states that if you pay off a loan early, the lender must provide the method for doing so. Typically, you need to pay the previous balance plus the current month's interest. For instance, if Doug and Donna Collins have a loan of $1,800 at 12% for 6 months, to pay off in the 4th month, the calculation involves using the previous balance ($913.70) and the current month's interest ($9.14), resulting in a final payment of $922.84.

Paying Off Simple Interest Installment Loans: A Guide

E N D

Presentation Transcript

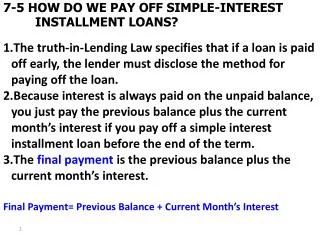

7-5 HOW DO WE PAY OFF SIMPLE-INTEREST INSTALLMENT LOANS? • The truth-in-Lending Law specifies that if a loan is paid off early, the lender must disclose the method for paying off the loan. • Because interest is always paid on the unpaid balance, you just pay the previous balance plus the current month’s interest if you pay off a simple interest installment loan before the end of the term. • The final payment is the previous balance plus the current month’s interest. Final Payment= Previous Balance + Current Month’s Interest

LET’s PRACTICE The first three months of the repayment schedule for Doug and Donna Collins’s loan of $1800 at 12% for 6 months is shown. What is the final payment if they pay the loan off with payment number 4? Find the previous balance. It is $913.70 Find the interest for the 4th month.(Principal x Rate x Time) $913.70 x 12% x 1/12 = $9.14 interest Find the final payment.(Previous Balance + Current Month’s Interest) $913.70 + $9.14 = $922.84 final payment