The Short-Run Policy Trade-Off

220 likes | 420 Vues

The Short-Run Policy Trade-Off. Outline Mystery of the missing equation The Phillips curve as solution to the mystery of the missing equation Phillips curve as a “policy menu.” Aggregate supply and the Phillips Curve The short-run Phillips curve The long-run Phillips curve

The Short-Run Policy Trade-Off

E N D

Presentation Transcript

The Short-Run Policy Trade-Off • Outline • Mystery of the missing equation • The Phillips curve as solution to the mystery of the missing equation • Phillips curve as a “policy menu.” • Aggregate supply and the Phillips Curve • The short-run Phillips curve • The long-run Phillips curve • Policy implications of the NAIRU

Mystery of the missing equation • A frequent knock on Keynesian business cycle theory was its (alleged) failure to incorporate the price level as an endogenous variable—that is, there is no equation that links price level movements to changes in real GDP, employment, the balance of trade, etcetera. • A path-breaking article by New Zealander A.W. Phillips in 1958 presented a solution to the mystery

Phillips empirical study indicated an inverse relationship between unemployment and the rate of increase of money wages The Phillips contribution1 Data points for the U.K. (annual) Rate of change of money wages 0 Unemployment rate 1A.W. Phillips. “The Relation Between Unemployment and the Rate of Change of Money Wages in the U.K., 1861-1957,” Economica, Nov. 1958

The Samuelson-Solow Contribution1 Professors Samuelson and Solow carried the Phillips’ work a step further by suggesting an inverse relationship between inflation and unemployment. The data for the U.S. appearedto back this up. 1P. Samuelson and R. Solow. “Analytical Aspects of Anti-Inflation Policy,” American Economic Review, May 1960.

www.bls.gov Phillips curve

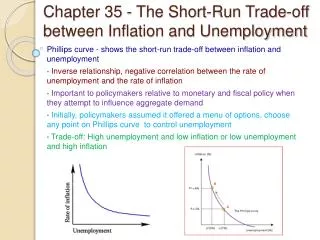

Stable trade-off between inflation and unemployment? The (inverted J) shape of the Phillips curve apparently gives policy makers an exploitable trade-off between inflation and unemployment. Moreover, the champions of the Phillips curve believed that the policy trade-off was “stable”—that is, the terms of the trade-off would hold up over time

The (MIT) Keynesian view went like this: Find the “politically acceptable” trade-offand use “active” aggregate demand management to achieve it. Inflation rate Policy target Phillips curve 0 Unemployment rate

Professor Friedman delivered a blistering attack on the Phillips curve at the American Economic Association meeting in 1967 The Friedman critique of the Phillips curve1 • 3 central points: • The Phillips curve “harbors a fundamental defect, namely, that the supply of labor is a function of the nominal wage.”This violates a basic axiom of microeconomic theory. • “There is no long run trade-off between inflation and unemployment.”Suggests there may be a short-run trade-off. • The long run Phillips curveis vertical at the NAIRU or natural rate of unemployment. 1Milton Friedman. “The Role of Monetary Policy,”AER, 58(1), March 1968, 1-17.

What is the NAIRU? ?? • NAIRU is an acronym for the “non-accelerating inflation rate of unemployment.” • The NAIRU, or alternatively, the “natural rate” of unemployment, is that level of unemployment corresponding to equilibrium in the Classical labor market. • The NAIRU is also defined as the rate of unemployment consistent with an unchanging (but not necessarily zero) inflation rate. • Corresponding to the natural rate of unemployment is the “natural” level of real GDP.

Definitions • UA is the actual rate of unemployment • UT is the target rate of unemployment • UN is the NAIRU or natural rate of unemployment • A is the actual rate of inflation • E is the expected rate of inflation • LRPC is the long run Phillips curve • SRPC is the short-run Phillips curve

What is the difference between the short-run and the long-run? In the long-run, agents correctly forecast inflation, that is:

“Adaptive” Expectations A key issue is how do agents form expectations about future inflation. Here we have a simple rule. Expected inflation in period t is equal to actual inflation in the period t – 1. That is: Which is to say that agents react to changes in the price level with a one-period lag.

The long-run Phillips curve is vertical at the NAIRU LRPC E = A Inflation rate E > A E < A 0 Unemployment rate UN

Short-run Phillips curves intersect the long-run Phillips curve at the expected rate of inflation LRPC E = A 12 Inflation rate SRPC2 :E =12% 3 SRPC1: E = 3% 0 Unemployment rate UN

Modeling stagflation LP E = A SP3 SP4 Monetary deceleration produces stagflation 8.1 S Inflation rate SP2 4.6 SP1 2.0 0 Unemployment rate UT UN

Monetarism took off in the 1970s • The monetarists, led by Professor Milton Friedman, experienced rising influence as inflation became public enemy number 1 in the 1970s. • Economists such as Edmund Phelps, Robert Lucas, and Thomas Seargent, subsequently added important modifications to the monetarist theory.

1960-69 1980-83

Summary • Money is non-neutral in the short-run—that is, unanticipated changes in the supply of money can affect output and employment, as well as prices, in the short run. • In the long-run, money is neutral. • Deviations of the economy from its “natural” growth path are explained mainly by erratic or unforeseen changes in the money supply of money. • Monetarists favor policy rules.