Download

1 / 34

350 likes | 624 Vues

This chapter explores short-term financing options such as trade credit, commercial paper, and bank loans for efficient working capital management. Learn about aggressive and conservative financing policies and the impact of maturity matching. Discover the risks and advantages of short-term debt compared to long-term debt, and understand the importance of effective annual rates (EARs) in evaluating different loan options.

E N D

CHAPTER 23Short-Term Financing • Working capital financing policies • Accounts payable (trade credit) • Commercial paper • Short-term bank loans • Secured short-term credit

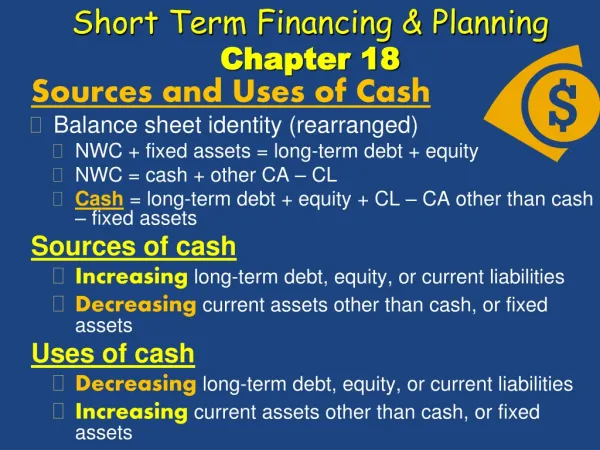

Working Capital Financing Policies • Maturity Matching: Matches the maturity of the assets with the maturity of the financing. • Aggressive: Uses short-term (temporary) capital to finance some permanent assets. • Conservative: Uses long-term (permanent) capital to finance some temporary assets.

Maturity Matching Financing Policy $ Temp. C.A. S-T Loans L-T Fin: Stock, Bonds, Spon. C.L. Perm C.A. Fixed Assets Years What are “permanent” assets?

Aggressive Financing Policy $ Temp. C.A. S-T Loans L-T Fin: Stock, Bonds, Spon. C.L. Perm C.A. Fixed Assets Years More aggressive the lower the dashed line.

Conservative Financing Policy $ Marketable Securities Zero S-T debt L-T Fin: Stock, Bonds, Spon. C.L. Perm C.A. Fixed Assets Years

The choice of working capital policy is a classic risk/return tradeoff. • The aggressive policy promises the highest return but carries the greatest risk. • The conservative policy has the least risk but also the lowest expected return. • The moderate (maturity matching) policy falls between the two extremes.

What is short-term credit?What are the major sources? • Short-term credit: Debt requiring repayment within one year. • Major sources: • Accruals • Accounts payable (trade credit) • Commercial paper • Bank loans

Short-term debt is riskier than long-term debt for the borrower. • Short-term rates may rise. • May have trouble rolling debt over. • Advantages of short-term debt. • Typically lower cost. • Can get funds relatively quickly with low transactions costs. • Can repay without penalty.

Is there a cost to accruals?Do firms have much control over amount of accruals? • Accruals are free in the sense that no explicit interest is charged. • However, firms have little control over accrual levels, which are influenced more by industry custom, economic factors, and tax laws than by managerial actions.

What is trade credit? • Trade credit is credit furnished by a firm’s suppliers. • Trade credit is often the largest source of short-term credit for small firms. • Trade credit is spontaneous and relatively easy to get, but the cost can be high.

B&B buys $3,030,303 gross, or $3,000,000 net, on terms of 1/10, net 30. However, the firm pays on Day 40.How much free and costly trade credit are they getting?What is the cost of the costly trade credit?

Gross/Net Breakdown • Company buys goods worth $3,000,000. That’s the cash price. • They must pay $30,303 more over the year if they forego the discount. • Think of the extra $30,303 as a financing cost similar to the interest on a loan. • Must compare that cost with the cost of alternative credit.

Net daily purchases = $3,000,000/360 = $8,333. Payables level if discount is taken: Payables = $8,333 (10) = $83,333. Payables level if don’t take discount: Payables = $8,333 (40) = $333,333. Credit Breakdown: Total trade credit = $333,333 Free trade credit = 83,333 Costly trade credit = $250,000

$30 , 303 k 0 . 1212 12 . 12%. Nom $250 , 000 Nominal Cost of Costly Trade Credit Firm loses 0.01($3,030,303) = $30,303 of discounts to obtain $250,000 in extra trade credit, so But the $30,303 in lost discounts is paid all during the year, not just at year-end, so the EAR is higher.

Nominal Cost Formula, 1/10, net 40 Discount % 1 - Discount % 360 Days taken - Discount period kNom = x = x = 0.0101 x 12 = 0.1212 = 12.12%. 1 99 360 30 Pays 1.01% 12 times per year.

Effective Annual Rate, 1/10, net 40 Periodic rate = 0.01/0.99 = 1.01%. Periods/year = 360/(40 - 10) = 12. EAR = (1 + Periodic rate)n - 1.0 = (1.0101)12 - 1.0 = 12.82%.

Commercial Paper (CP) • CP are short term notes issued by large, strong companies. B&B could not issue CP; the company is too small. • CP trades in the market at rates just above the T-bill rate. • CP is bought by banks and other companies, then held as marketable securities for liquidity purposes.

A bank is willing to lend B&B $100,000 for 1 year at an 8 percent nominal rate. What is the EAR under the following five loans? 1. Simple annual interest, 1 year. 2. Simple interest, paid monthly. 3. Discount interest. 4. Discount interest with 10 percent compensating balance. 5. Installment loan, add-on, 12 months.

Why must we use Effective Annual Rates (EARs) to evaluate the loans? • In our examples, the nominal (quoted) rate is 8% in all cases. • We want to compare loan cost rates and choose the alternative with the lowest cost. • Because the loans have different terms, we must make the comparison on the basis of EARs.

Simple Annual Interest, 1-Year Loan “Simple interest” means not discount or add-on. Interest = 0.08($100,000) = $8,000. $8 , 000 . k EAR 0 . 08 8 . 0% Nom $100 , 000 On a simple interest loan of one year, kNom = EAR.

Simple Interest, Paid Monthly Monthly interest = (0.08/12)($100,000) = $666.67. 0 1 12 ... 100,000 -666.67 -667.67 -100,000.00 12 100000 -666.67 -100000 N I/YR PV PMT FV 0.66667 (More…)

kNom = (Monthly rate)(12) = 0.66667%(12) = 8.00%. 12 0 . 08 EAR 1 1 8 . 30%. 12 or: 8 NOM%, 12 P/YR, EFF% = 8.30%. Note: If interest were paid quarterly, then: 4 0 . 08 EAR 1 1 8 . 24%. 4 Daily, EAR = 8.33%.

N I/YR PV PMT FV 8% Discount Interest, 1 Year Interest deductible = 0.08($100,000) = $8,000. Usable funds = $100,000 - $8,000 = $92,000. 0 1 i = ? 92,000 -100,000 1 92 0 -100 8.6957% = EAR

Discount Interest (Continued) Amount needed 1 - Nominal rate (decimal) Amt. borrowed = = = $108,696. $100,000 0.92

Amount needed 1 - Nominal rate - CB Face amount of loan = = = $121,951. $100,000 1 - 0.08 - 0.1 Need $100,000. Offered loan with terms of 8% discount interest, 10% compensating balance. (More...)

Interest = 0.08 ($121,951) = $9,756. $9 , 756 EAR 9 . 756%. $100 , 000 EAR correct only if amount is borrowed for 1 year. (More...)

8% Discount Interest with 10% Compensating Balance (Continued) 0 1 i = ? 121,951 Loan -121,951 + 12,195 -109,756 -9,756 Prepaid interest -12,195 CB 100,000 Usable funds 1 100000 0 -109756 N I/YR PV PMT FV 9.756% = EAR This procedure can handle variations.

1-Year Installment Loan, 8% “Add-On” Interest = 0.08($100,000) = $8,000. Face amount = $100,000 + $8,000 = $108,000. Monthly payment = $108,000/12 = $9,000. = $100,000/2 = $50,000. Approximate cost = $8,000/$50,000 = 16.0%. Average loan outstanding (More...)

Installment Loan To find the EAR, recognize that the firm has received $100,000 and must make monthly payments of $9,000. This constitutes an ordinary annuity as shown below: Months 0 1 2 12 ... i=? 100,000 -9,000 -9,000 -9,000

N I/YR PV PMT FV 12 100000 -9000 0 1.2043% = rate per month kNom = APR = (1.2043%)(12) = 14.45%. EAR = (1.012043)12 - 1 = 15.45%. 14.45 NOM enters nominal rate 12 P/YR enters 12 pmts/yr EFF% = 15.4489 = 15.45%. 1 P/YR to reset calculator.

What is a secured loan? • In a secured loan, the borrower pledges assets as collateral for the loan. • For short-term loans, the most commonly pledged assets are receivables and inventories. • Securities are great collateral, but generally firms needing short-term loans generally do not have securities.

What are the differences betweenpledgingandfactoringreceivables? • If receivables are pledged, the lender has recourse against both the original buyer of the goods and the borrower. • When receivables are factored, they are generally sold, and the buyer (lender) has no recourse to the borrower.

What are three forms of inventory financing? • Blanket lien. • Trust receipt. • Warehouse receipt. • The form used depends on the type of inventory and situation at hand.

Legal stuff is vital. • Security agreement: Standard form under Uniform Commercial Code. Describes when lender can claim collateral. • UCC Form-1: Filed with Secretary of State to establish claim. Future lenders do search, won’t lend if prior UCC-1 is on file.