Issues in Vertical Integration

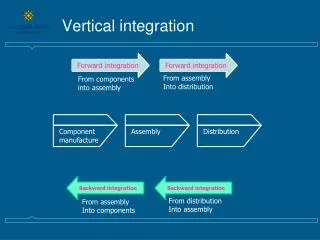

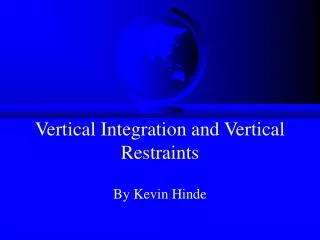

Issues in Vertical Integration. Vertical Non-Integration. Supplier 1. Supplier 2. Supplier 3. Upstream. The Firm. Distributor 1. Distributor 2. Distributor 3. Downstream. Consumers. Vertical Integration. Supplier 1. Supplier 2. Supplier 3. Upstream. The Firm. Distributor 1.

Issues in Vertical Integration

E N D

Presentation Transcript

Vertical Non-Integration Supplier 1 Supplier 2 Supplier 3 Upstream The Firm Distributor 1 Distributor 2 Distributor 3 Downstream Consumers

Vertical Integration Supplier 1 Supplier 2 Supplier 3 Upstream The Firm Distributor 1 Distributor 2 Distributor 3 Downstream Consumers

Problems Facing the Non–Integrated Firm • Double marginalization • Hold-up & other bargaining problems • Threat of vertical foreclosure • Downstream free-riding

Market-Power Pricing: A Review $/unit MC CS p* DWL profit Demand Quantity Q* MR

Double Marginalization • Consider two independent firms, upstream and downstream, that each have market power (i.e., perceive themselves as facing downward sloping firm-specific demand). • Each firm then prices at a mark up over marginal cost. • Recall that pricing above MC yields deadweight losses • Now these are being incurred twice!

Double Marginalization • If upstream and downstream merge, then upstream ceases to try to capture surplus from downstream. • Upstream prices (transfers) at MC. • One deadweight loss eliminated. • Like picking money up off the table!

A Digression: Transfer Pricing • Within a firm, goods should always be transferred at marginal cost (otherwise firm imposes a deadweight loss on itself). • Note marginal cost needs to be calculated using opportunity cost.

Example • Upstream division incurs constant production marginal cost of $1 per unit. • Upstream division also sells outside the firm at a price of $4 per unit. • If upstream division operating at capacity, then transfer price = $4, since that’s the opportunity cost of internal transfer. Decision is who not whether! • If not at capacity, then transfer price = $1, the production MC. Decision is whether not who!

Competitive Markets & Double Marginalization • If the upstream supplier is in a competitive mkt. (alternatively, in the Bertrand trap), then it prices at MC. • Consequently, no deadweight loss. • Impossible to get good for less. • Double-marginalization (i.e., transfer-pricing) justifications for merging do not apply.

Comp. Mkts. & Double Marg. • If downstream is competitive, then it’s pricing at MC. • It’s, therefore, not creating one of the two deadweight losses. • Hence, there’s nothing to pick up off the table vis-à-vis double marginalization— again not a motive to merge.

Hold-ups & Bargaining Issues • Firms often need to make transaction-specific investments. • E.g., a mold built to stamp out GM fenders can’t be used for Ford fenders. • This creates the danger of hold-up (opportunism). • After one firm (e.g., Fisher Body) makes investment, investment is sunk and subsequent bargaining w/ other firm (e.g., GM) could lead to returns that are too low.

Example • Upstream invests $12 million on transaction-specific investment. • MC for upstream for parts is $10. • A million units to be traded. • Downstream’s value is $30/part. • Surplus from post-investment trade = $20/unit. • Suppose bargaining splits surplus evenly, then upstream gets paid $20/unit; so gross profit is $10 million. • But this is less than investment cost!

Contractual Solutions • Obviously, should fix price in advance at $22 or more per part! • But in many cases this will create agency problems. • If quality, delivery time, etc., matter, what incentive does upstream now have to do good job given guaranteed price? • But w/o guaranteed price, upstream subject to hold-up.

Example: Disney & Pixar • Disney wants Pixar to make computer-animated film, Toy Story, which Disney will market. • Given Disney’s expertise in mkt’ing animated films, relationship makes sense. • What contract to write?

Disney & Pixar (cont.) • If Disney fixes price in advance, then Pixar’s incentives are blunted. • If parties wait to negotiate price after Pixar produces film, then Pixar’s incentives better, but now problem of hold-up. • Possible solution: option contract.

Option Contract • Contract fixes price if trade, but gives Disney right to refuse to trade. • If Pixar doesn’t make sufficiently good film, then Disney lets its option to buy expire. • If Pixar does make sufficiently good film, then Disney will want to exercise.

Renegotiation • A problem with any contract is that it can be renegotiated. • Hence, if outcome arises in which exercising contract as written would leave surplus on table, then parties will renegotiate. • However, the anticipation of renegotiation can distort ex ante incentives.

Renegotiation • This can undo the option-contract solution • What ultimately matters is which of two effects dominates • hold-up effect • threat-point effect

Threat-point Effect • Our assumption of wholly specific investment is often unrealistic—good could have a lower, general value (e.g., Warner Bros. could mkt. Toy Story). • Does gen’l value increase more at margin w/ investment than specific value? • If so, threat-point effect dominates and efficiency can be achieved. • If not, hold-up effect dominates and inefficient outcome.

Other Solutions to Hold-up • Keep markets thick: • harder to be held up if you have alternative suppliers or distributors to use. • additional benefits of diversification (e.g., not hosed if supplier’s factory burns down). • Develop reputation for cooperation rather than opportunism. • works if PDV of cooperate > PDV of opportunism today and non-cooperation tomorrow.

Reputation payoff cooperate opportunistic time 0 1 2 ...

Merge to Avoid Hold-up • Merger serves to limit danger of hold-up • Merger, however, doesn’t miraculously cure agency problems. • still need to provide incentives to upstream & downstream managers • dangers in how this is done (e.g., could be mistake to turn upstream into profit center—usually better to make cost center).

Vertical Foreclosure • Market power in one stream can be extended to another through vertical foreclosure. U1 U2 D1 D2 D3

Vertical Foreclosure U1 U2 D1 D2 D3 D2 and D3 at cost disadvantage, since U2 has market power. U2 may not do as well as U1 because of double marginalization.

Vertical Foreclosure • Also deters entry • locking up suppliers • locking up buyers • Not surprisingly, vertical mergers also receive antitrust scrutiny.

Downstream Free-riding • Suppose downstream is retail level. • Two retailers: • one provides customer information on product, customer service, etc. • other just sells product w/o doing any of that. • Problem: • the 2nd has cost advantage and can charge lower price • customers get info., service, etc. from 1st, but buy from 2nd.

Free-riding • 1st retailer can’t compete unless drops services. • But this could hurt manufacturer in terms of decreasing overall demand for product. • Solution: • force all retailers to charge same price (resale price maintenance) • Problem: RPM is generally illegal

Free-riding • Consequence: May have to merge into retailing to preserve service, etc. • Consequence: Franchising (some problems) • Consequence: Provide alternative motives for retailers to keep margins up. • participation in joint advertising campaigns • treatment (e.g., how fast restocked, etc.) • ability to carry product at all (e.g., drop those not providing service)

Problems Facing Integrated Firm • Detraction from core competencies. • Difficulty of selective intervention. • Incompatible cultures. • Product market is a very good incentive device—hard to duplicate internally. • Financial markets are very good incentive devices—hard to duplicate internally. • Captive market can inhibit innovation.