Download

1 / 3

30 likes | 128 Vues

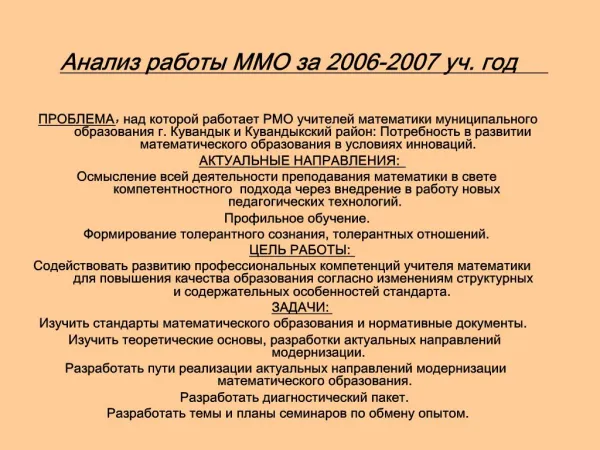

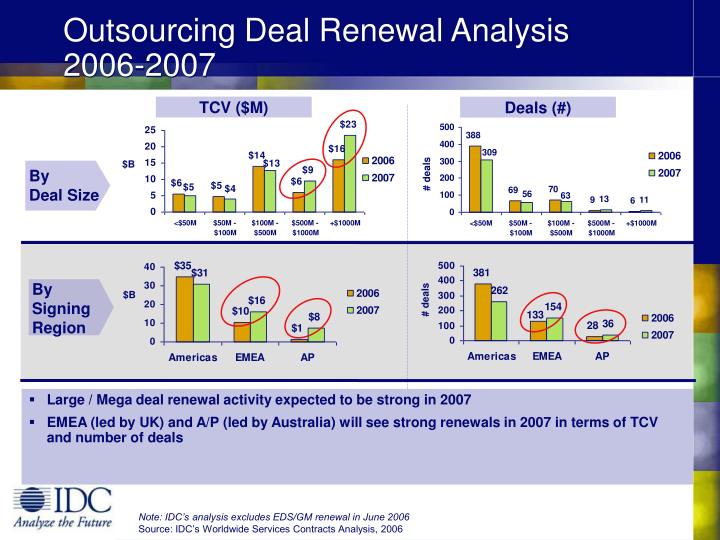

Outsourcing Deal Renewal Analysis 2006-2007. TCV ($M). Deals (#). $B. By Deal Size. # deals. $B. By Signing Region. # deals. Large / Mega deal renewal activity expected to be strong in 2007

E N D

Outsourcing Deal Renewal Analysis2006-2007 TCV ($M) Deals (#) $B By Deal Size # deals $B By Signing Region # deals • Large / Mega deal renewal activity expected to be strong in 2007 • EMEA (led by UK) and A/P (led by Australia) will see strong renewals in 2007 in terms of TCV and number of deals Note: IDC’s analysis excludes EDS/GM renewal in June 2006 Source: IDC’s Worldwide Services Contracts Analysis, 2006

Outsourcing Deal Renewal Analysis 2006-2007 (cont’) TCV ($M) Deals (#) $B By Segment # deals $B By Industry # deals • Renewals led by ISO deals. Vendors will need to develop breadth of offerings to pursue full ISO or a portion of deal. • Majority of renewals (82% in 2006, and 73% in 2007) will be moving into 2nd Gen outsourcing. • 2006 renewals led by: (1) manufacturing (2) financial services (3) government • 2007 renewals led by: (1) financial services (2) manufacturing (3) communications Note: IDC’s analysis excludes EDS/GM renewal in June 2006 Source: IDC’s Worldwide Services Contracts Analysis, 2006

Outsourcing Renewals by Vendor 2006 & 2007 Most at Stake - 4 Vendors account for $77bn in renewals N = 78 N = 16 • Impact N = 35 • Target incumbents in weakened state (e.g., EDS, CSC) • Partner with companies in complementary markets (e.g., AT&T) N = 51 TCV = $106B (N = 995 Deals) Note: IDC’s analysis includes EDS/GM renewal in June 2006 Source: IDC’s Worldwide Services Contracts Analysis, 2006